Should You Include Gold in Your Investment Portfolio? A Thoughtful Analysis from a Value Investing Perspective

If you want a deep dive on gold, you can watch the video here:

The price of gold has recently surged past $3,000 per ounce, igniting fervent discussions among investors about its future trajectory. Many are convinced that gold is on an unstoppable upward climb, with predictions calling for $5,000 in the near term and $10,000 or more in the long run. While these projections may seem compelling, the more pressing question for investors is whether gold truly deserves a place in a well-structured portfolio.

To answer this, we must examine gold’s historical performance, its role in modern finance, and the macroeconomic forces that could drive its price higher—or leave it stagnant for years. More importantly, we must assess whether gold aligns with the principles of value investing, which prioritizes long-term wealth preservation, risk management, and cash-generating assets.

Gold’s Historical Performance: A Story of Peaks and Valleys

Gold has long been regarded as a store of value, but its price history reveals a pattern of dramatic surges followed by prolonged stagnation.

In 1971, when the U.S. abandoned the gold standard, the metal was officially priced at $35 per ounce. Over the next decade, it skyrocketed to nearly $800 by 1980—an extraordinary rally fueled by inflation fears and geopolitical instability. However, this was followed by a 20-year bear market, with gold sinking back to $250 by the early 2000s.

The 2008 financial crisis reignited interest in gold as a safe haven, pushing prices to an all-time high of $1,900 in 2011. Yet, once again, the rally fizzled, and gold spent much of the next decade trading sideways. Only in recent years, amid unprecedented monetary expansion and soaring debt levels, has gold reclaimed its upward momentum, surpassing $3,000 in 2024.

The Inflation-Adjusted Reality

While gold’s nominal gains appear impressive, its inflation-adjusted returns tell a different story. After accounting for rising prices over the past half-century, gold’s real returns have been modest at best. Unlike productive assets such as stocks or real estate—which generate earnings, dividends, and rental income—gold simply sits there, relying solely on speculative demand for appreciation.

This raises a crucial question: If gold doesn’t compound wealth over time, is it truly an investment—or just a hedge against chaos?

The Bullish Case for Gold: Why $10,000 Is Plausible

Despite its historical volatility, there are compelling reasons to believe gold could reach $5,000 or even $10,000 in the coming years.

1. Runaway Government Debt and Deficits

Governments worldwide are spending beyond their means, with no political will to reverse course. The U.S. national debt has surpassed $34 trillion, and interest payments alone now exceed $1 trillion annually. This trajectory is unsustainable, and when crises hit, central banks print more money—devaluing currencies and boosting gold’s appeal.

2. The Return of Inflation

After decades of relatively stable prices, inflation has reemerged as a structural threat. Supply chain disruptions, energy shortages, and labor market shifts suggest that higher prices may persist, eroding the value of cash and bonds. Gold, as a finite resource, tends to hold its purchasing power over time.

3. Central Banks Are Hoarding Gold

In recent years, central banks—particularly in China, Russia, and India—have been aggressively accumulating gold, reducing the available supply. This institutional demand creates a price floor, making severe declines less likely.

4. Geopolitical Uncertainty

With rising tensions between major powers, trade wars, and military conflicts, investors are increasingly seeking non-political assets like gold that can’t be frozen or confiscated (at least not easily).

Given these factors, $5,000 gold seems achievable within this decade, and $10,000 is possible if monetary debasement accelerates.

The Risks and Drawbacks of Gold Ownership

While the bullish arguments are strong, gold is far from a risk-free investment.

1. It Doesn’t Generate Income

Unlike stocks (dividends), bonds (interest), or real estate (rent), gold produces no cash flow. You only profit if someone else is willing to pay more for it later—a dynamic that can lead to long periods of stagnation.

2. It’s Highly Sensitive to Sentiment

Gold thrives in times of fear and uncertainty, but when markets are calm, it often underperforms. Investors who bought at the 2011 peak waited over a decade just to break even.

3. Opportunity Cost Could Be High

Historically, stocks have outperformed gold over the long run. If you allocate too much to gold, you may miss out on compounding growth from productive businesses.

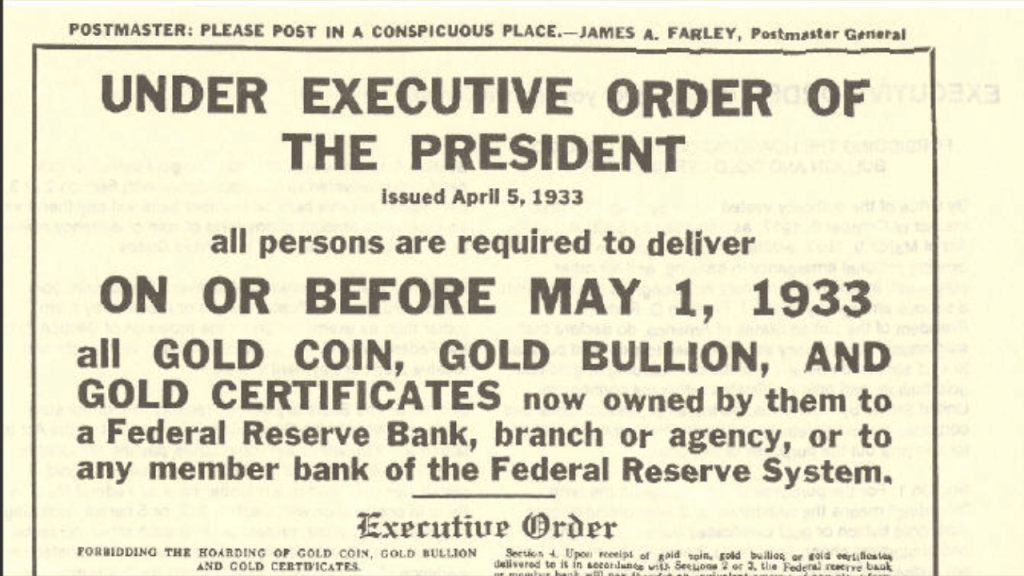

4. Regulatory Risks (Though Unlikely)

In 1933, the U.S. government banned private gold ownership, forcing citizens to sell at a fixed price. While a repeat seems improbable, extreme financial crises can lead to extreme policies.

How (and Whether) to Include Gold in Your Portfolio

Given these pros and cons, how should investors approach gold?

Option 1: A Small Hedge (5–10% Allocation)

Many “all-weather” portfolios include a small gold position (typically 5–10%) to reduce volatility. The idea is to rebalance periodically—selling some when gold surges and buying more when it’s out of favor.

Option 2: Avoid It Entirely (If You Have Better Alternatives)

If you’re confident in finding high-quality businesses or other inflation-resistant assets, gold may be unnecessary. Warren Buffett famously avoids gold because it “doesn’t do anything”—he prefers cash-flowing investments.

Option 3: Use Gold as Crisis Insurance

Some investors hold physical gold (coins, bars) strictly as disaster insurance, not expecting returns. In a true financial collapse, gold could become one of the few accepted stores of value.

Final Thoughts: Is Gold Right for You?

Gold’s future is bright in nominal terms, but its role in a portfolio depends on your goals, risk tolerance, and investment philosophy.

Gold may very well reach $5,000 or $10,000, but its value in your portfolio depends on whether you see it as an investment or insurance.

Value Investing Risk & Reward Quadrant (check all the stock analyses)