September Value Investing Quadrant: A Deep Dive into Risk and Reward

Check the full Value Quadrant video here:

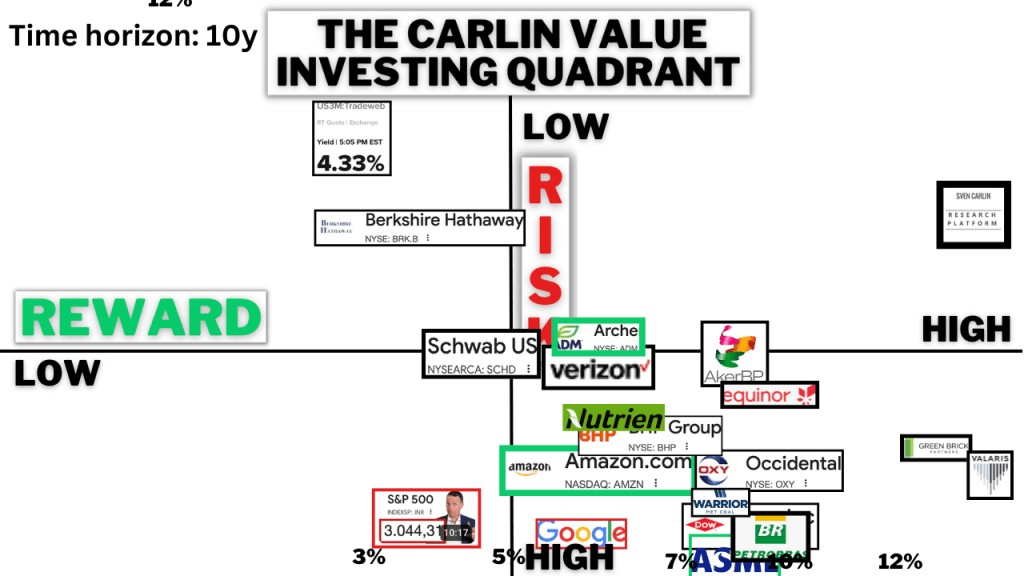

The essence of value investing lies in carefully weighing risk against reward. In today’s market, where the S&P 500 trades at historically high valuations, investors are forced to look beyond the broad index in search of individual businesses that still offer favorable odds. At a P/E of nearly 29, the S&P implies only a 3–4% annual return over the next decade or two, leaving little margin of safety. This backdrop sets the stage for a detailed look at where true value may still be found — and where risk threatens to overwhelm potential gains.

The Market Backdrop: S&P 500

The S&P 500’s lofty valuation is the first warning sign. Historically, investors have enjoyed 8–10% returns from the index, but at current multiples, forward returns are likely to be half that. Today’s buyers are paying dearly for each dollar of earnings, leaving little room for disappointment. If economic growth falters, or if earnings merely flatten, investors could face not just reduced returns but significant drawdowns. For disciplined value investors, the index is therefore less an opportunity and more a risk indicator — a signal to hunt for individual bargains rather than hiding in the broad market.

Consumer & Retail

Nike once embodied the perfect combination of brand power and global growth. Today, however, the story is more complicated. Its products remain iconic, yet the company’s valuation assumes a level of growth that is increasingly difficult to achieve. Competition is fierce, consumers are fickle, and global markets are saturated. Paying premium multiples for a brand that may already have peaked is a dangerous proposition.

Lululemon sits in a similar position. The brand has tapped into the athleisure trend with great success, and expansion opportunities remain, especially in international markets. Yet the stock is priced as though double-digit growth will continue indefinitely. Any slowdown in demand, whether from consumer fatigue or competitive pressures, could see shares re-rate sharply. Like Nike, Lululemon offers more risk than reward at today’s valuations.

Kraft Heinz tells another story altogether. The company has become the archetype of a struggling consumer staple. Once-powerful brands like Heinz ketchup and Kraft cheese no longer command the loyalty they once did, and revenue growth has stalled. While the dividend is attractive, its long-term sustainability is in doubt. Investors who treat Kraft Heinz like a bond may be disappointed if earnings fail to cover payouts in the future. For now, it offers stability, but little chance of meaningful wealth creation.

Dividend-Oriented Plays

Dividend-focused investments often appeal to those seeking stability and income, and the Schwab U.S. Dividend ETF is a reliable way to access that. With a basket of established dividend payers, the fund offers a yield that should deliver 5–7% annual returns over the long term. The problem, however, is valuation. Many of the ETF’s holdings are already expensive, meaning investors are paying up for safety and may not capture much upside.

Verizon, by contrast, provides a single-stock example of a high-yield, income-driven investment. Its 6% dividend yield is generous and supported by recurring cash flows from its telecom network. But the company carries a heavy debt burden, making it acutely sensitive to higher interest rates. Growth prospects are limited in a mature market, and while the dividend may continue, investors should not expect much in the way of capital appreciation. Verizon is essentially a bond in equity form: reliable income, limited upside, and vulnerability to shifts in credit markets.

Compounders & Blue-Chip Anchors

Berkshire Hathaway continues to stand out as a safe harbor. Its portfolio of wholly owned businesses and equity holdings generates consistent earnings, while Warren Buffett’s capital allocation philosophy ensures prudence and discipline. Yet at today’s price, Berkshire is not cheap. The days of 10% annual compounding may be behind it; more likely, investors will see returns of 4–5% going forward. Still, the low risk makes it a dependable cornerstone for long-term portfolios.

Alphabet, or Google, is in a more precarious position. The company still dominates digital advertising and continues to grow strongly in cloud computing and YouTube. Its cash flows are enormous, and its balance sheet is robust. But lurking in the background is a fundamental risk: the rise of artificial intelligence. If AI disrupts search, Google’s core revenue engine could be threatened. Regulators also remain keenly focused on the company’s dominance. At its current valuation, Alphabet is cheaper than many of its big-tech peers, but the uncertainty around its business model makes the risk higher than it appears at first glance.

ASML, the Dutch semiconductor equipment maker, is another world-class business trading at a premium. Its machines are essential for advanced chip production, giving it a wide moat and an almost monopolistic position in extreme ultraviolet lithography. Demand will grow as the world needs ever more powerful chips. But the semiconductor industry is notoriously cyclical, and ASML’s valuation reflects high expectations. Investors buying today may earn 7% annually over a decade, but should be prepared for sharp swings along the way.

Growth Giants

Amazon has always been a company willing to sacrifice short-term profit for long-term growth, and that remains true today. Its e-commerce business continues to expand, AWS dominates cloud computing, and its advertising arm is growing rapidly. While expected returns of 7–10% annually are realistic, the path will be volatile. Periods of heavy reinvestment often weigh on margins and stock performance, making Amazon best suited for investors who buy on downturns and hold through cycles.

Alibaba offers a similar growth story in Asia, with e-commerce, cloud computing, and now AI forming its growth engines. Its valuation, however, is far more modest, reflecting deep investor skepticism. Chinese regulatory crackdowns and a slowing domestic economy have left many foreign investors wary. Still, if Alibaba can navigate these headwinds, the company could deliver close to 10% returns annually, offering more upside than Amazon but at higher political and macroeconomic risk.

Cyclicals & Commodities

Dow Inc. represents the high-risk end of the spectrum. As a chemical producer, it is deeply exposed to commodity cycles, and its history of dividend cuts and poorly timed buybacks does not inspire confidence. While there is the possibility of a 2–3x gain in the next upcycle, the risks are immense, making Dow a speculative bet.

Occidental Petroleum, on the other hand, is a more stable energy play. With Warren Buffett’s Berkshire Hathaway owning a large stake, management has focused on reducing debt and returning cash to shareholders. If oil prices remain steady, Occidental could offer 10% annual returns, with the potential to double in value. The key risk is oil price volatility, but Buffett’s vote of confidence provides some comfort.

Among European energy companies, Equinor, Eni, and BP stand out for their generous dividend policies. Even if oil prices were to fall, these companies could continue paying yields of 8–10%, thanks to their low-cost operations. For investors seeking stable income with moderate commodity exposure, they represent safer choices within the energy sector.

BHP Group, the global mining giant, provides another form of commodity exposure. With dominant iron ore assets and a solid balance sheet, BHP offers both yield and growth. Its dividends are around 4%, and long-term returns may approach 10%. The main risk is recession-driven demand destruction, but BHP’s asset quality makes it more resilient than most cyclicals.

Archer-Daniels-Midland, the agricultural processor, is a steady business that thrives on global food demand. Earlier in the year, it traded at attractive valuations, but after a significant rally, expected returns are closer to 6%. It remains a safe company, but not the bargain it once was.

Warrior Met Coal exemplifies the high-risk, high-reward profile of commodity producers. The company has benefited from higher coal prices and new project developments, lifting its stock significantly. But coal is deeply cyclical, and political as well as environmental pressures make it a fragile long-term investment.

Valaris, the offshore drilling contractor, offers a different kind of energy upside. Trading at a 10% free cash flow yield, the company could triple in value if the offshore cycle continues to recover. But this is an extremely cyclical business, and any downturn in oil demand could erase gains just as quickly. For investors with patience and strong stomachs, Valaris represents a classic deep-value turnaround.

Niche & Overlooked

Amidst the larger names, Amsterdam Commodities (Acomo) is a hidden gem. Specializing in sourcing food ingredients, spices, tea, and nuts, the company has quietly built a century-long record of steady growth. Its strategy of integrating acquisitions has allowed it to compound earnings at around 8% annually. With a dividend yield of 5% and a valuation at just six times earnings, Acomo presents one of the most compelling opportunities available today: a low-risk business with the potential to double in value while paying investors generously along the way.

Another niche opportunity comes from David Einhorn’s Greenlight Capital Re and related real estate ventures. By focusing on land and property investments, Einhorn has managed to compound value at 12–13% annually. This offers both inflation protection and long-term compounding, though the risks of real estate cycles cannot be ignored.

Final Thoughts

Taken together, the quadrant reveals a bifurcated market. On one side are the popular consumer and tech giants — Nike, Lululemon, Amazon, Google — many of which are priced for perfection and offer muted returns at elevated risk. On the other are overlooked, cyclical, or niche businesses that, while riskier in the short term, provide far greater long-term reward.

Berkshire Hathaway and select European energy names represent safe anchors, offering steady compounding and dividends. High-risk plays like Dow, Warrior Met Coal, and Valaris offer lottery-ticket upside for those willing to endure volatility. But perhaps the clearest opportunity lies in the overlooked corner of Amsterdam Commodities: a small, defensive, growing business trading at a valuation that still leaves room for value investors to win.

In an era when the S&P itself looks stretched, the quadrant reminds us that patience, discipline, and careful stock selection are more vital than ever.

Value Investing Risk & Reward Quadrant (check all the stock analyses)

To follow the quadrant updates, join my free value investing course. There will be one email monthly discussing the various updates! That is it! VALUE INVESTING FOR LIFE COURSE!