Reinet Investments: A Value Trap or a Hidden Gem?

If you want to watch an in-depth video discussing Aker BP, you can watch it here:

Holding companies have long fascinated value investors due to their tendency to trade at steep discounts to their underlying net asset value (NAV). These discounts can present compelling opportunities—but they can also mask structural flaws, poor capital allocation, or simply a lack of market interest. One such company that embodies both the promise and the pitfalls of this investment style is Reinet Investments S.C.A., a Luxembourg-based holding firm that was once part of the Richemont Group.

At first glance, Reinet appears to be a textbook case of undervaluation. The company’s reported NAV stands at approximately €6.9 billion, translating to around €46 per share. Yet, its stock trades near €22—a staggering 52% discount to its stated intrinsic value. Historically, Reinet’s NAV has grown at a respectable 9% annually over the past 15 years, suggesting that its underlying assets are not stagnant but rather appreciating steadily.

The Anatomy of Reinet’s Portfolio

The company’s investment portfolio is anchored by two major components:

- The Pension Insurance Corporation Group (PIC) – A UK-based pension fund manager overseeing roughly £50 billion in assets, PIC is Reinet’s crown jewel. However, unlike publicly traded insurers, PIC does not provide detailed financial disclosures, making it difficult for investors to assess its true profitability or risks.

- Liquidated British American Tobacco (BAT) Stake – Reinet recently sold its position in BAT, generating €1.5 billion in cash. This infusion of liquidity could be a catalyst—if deployed wisely.

Beyond these core holdings, Reinet maintains a smattering of smaller investments, including private equity stakes and other financial ventures, collectively valued at around €1 billion. The problem, as with many holding companies, is that these assets are often illiquid, opaque, or subject to management’s discretion—leaving shareholders in the dark about their real worth.

Why Such a Deep Discount?

The market’s skepticism toward Reinet is not unfounded. Several structural issues contribute to the persistent gap between its market price and NAV:

1. The Black Box Problem

Holding companies like Reinet are notorious for their lack of transparency. Unlike standalone businesses that issue detailed quarterly reports, holding firms often provide only broad summaries of their investments. PIC, for instance, does not publish the kind of granular financial data that would allow analysts to model its cash flows or risks accurately. Without this visibility, investors must take management’s word on valuation—a precarious position.

2. The Capital Allocation Dilemma

Now that Reinet has €1.5 billion in cash from the BAT sale, the critical question is: What will management do with it? The company has stated that the proceeds will fund “ongoing investment activity,” but history suggests that such vague mandates can lead to questionable decisions.

Consider the case of Prosus (PRX), another holding company that traded at a steep NAV discount. Prosus famously invested €4 billion in Just Eat Takeaway, a deal that ultimately destroyed value. If Reinet follows a similar path—deploying capital into overpriced or speculative ventures—the discount could widen further rather than narrow.

3. Management Incentives: Are They Aligned?

Executive compensation is another red flag. Reports indicate that Reinet’s CEO has received €10 million+ in remuneration, raising concerns about whether leadership is truly focused on maximizing shareholder value or simply growing assets (and fees). In an ideal scenario, a holding company trading at a deep discount should be aggressively buying back shares or distributing dividends—not expanding into unrelated ventures.

Comparisons to Other Holding Companies

Reinet is not alone in its struggles. Many holding firms trade below NAV due to:

- Complex corporate structures that obscure true value.

- Minority stakes in illiquid assets, limiting control over exits or dividends.

- Market distrust in management’s ability to unlock value.

Prosus, for example, has long traded at a discount due to its massive but unwieldy stake in Tencent. Similarly, Sofina and Exor have faced skepticism over their investment strategies. Yet, in some cases, these discounts have narrowed dramatically when management took decisive action—such as spinning off assets or initiating buybacks.

Is Reinet a Buy? The Verdict

The 52% discount to NAV is undeniably tempting. If PIC is as valuable as management claims, and if the BAT proceeds are reinvested wisely, Reinet could prove to be a multi-bagger for patient investors. However, the risks are substantial:

- Valuation Uncertainty: Without clearer disclosures on PIC’s financials, the NAV could be overstated.

- Capital Misallocation: If management squanders the BAT windfall on dubious acquisitions, the discount could persist or worsen.

- Structural Headwinds: Holding companies often remain undervalued for years due to investor apathy or distrust.

Conclusion: A Cautious Approach

For deep-value investors, Reinet represents a high-risk, high-reward proposition. The sheer size of the discount provides a margin of safety, but due to the lack of transparency, this makes this stock a very risky investment idea

Before investing, shareholders should demand:

- Greater transparency on PIC’s financials.

- A clear plan for the BAT proceeds (buybacks, dividends, or high-return investments).

- Alignment of executive compensation with shareholder returns.

Until then, Reinet remains a potential value trap—one that could either reward patience or serve as a cautionary tale.

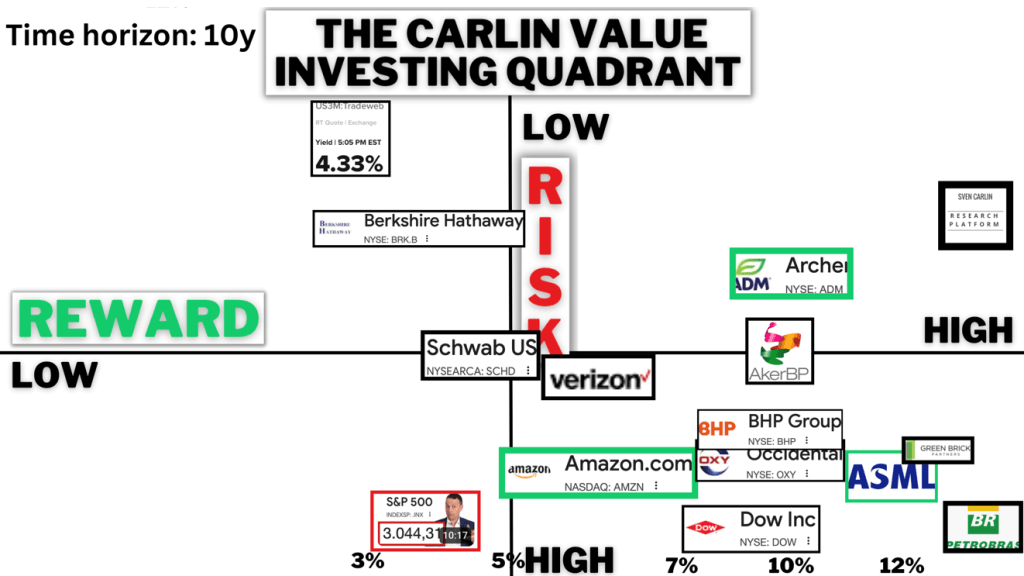

Value Investing Risk & Reward Quadrant (check all the stock analyses)

v