NVIDIA: A Deep Dive into the AI Juggernaut’s Valuation and Future Prospects

If you want a deep dive into Nvidia stock, watch the full video about the Magnificent 7 Stocks:

The rise of NVIDIA over the past few years has been nothing short of extraordinary. From being primarily known as a gaming GPU company to becoming the undisputed leader in artificial intelligence hardware, NVIDIA’s transformation has captivated investors and reshaped entire industries. The company’s stock has surged tenfold since 2020, fueled by an unprecedented boom in AI demand, data center expansion, and its dominance in high-performance computing. However, after such a meteoric rise, questions naturally arise: Is NVIDIA still a good investment at current levels? Or has the stock become overvalued, riding a wave of hype that may eventually recede?

The AI Revolution and NVIDIA’s Central Role

NVIDIA’s success is inextricably linked to the explosive growth of artificial intelligence. The company’s graphics processing units (GPUs) have become the backbone of AI training and inference, powering everything from large language models like ChatGPT to autonomous vehicles and advanced robotics. This dominance has translated into staggering financial performance. Revenue has skyrocketed from $16.7 billion in 2021 to over $60 billion in 2024, with data center sales—now the company’s largest segment—growing fivefold in just three years.

The driving force behind this growth is the insatiable demand for AI infrastructure. Hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud are investing hundreds of billions of dollars to expand their AI capabilities, and NVIDIA’s chips are at the heart of these efforts. The company’s latest generation of GPUs, such as the H100 and the upcoming Blackwell architecture, are in such high demand that supply struggles to keep pace. Analysts project that NVIDIA’s revenue could continue growing at a blistering pace, with estimates suggesting 50% growth in 2025, followed by 27% in 2026, before settling into a still-impressive 15% annual growth trajectory in the years beyond.

Valuation: The Elephant in the Room

Despite these impressive growth metrics, NVIDIA’s valuation remains a contentious topic among investors. The stock currently trades at a forward price-to-earnings (P/E) ratio of around 40 and a price-to-free cash flow (P/FCF) multiple of approximately 48. These figures are undeniably high by traditional standards, raising concerns about whether NVIDIA’s current share price already reflects its best-case future scenario.

To assess whether the stock is fairly valued, we can consider three potential scenarios:

- The Bull Case: AI Adoption Exceeds Expectations

If NVIDIA continues to grow its free cash flow at 25% annually over the next decade—a scenario that assumes AI adoption accelerates beyond current projections—the company’s market capitalization could theoretically reach $6.7 trillion within ten years. This would imply an annualized return of roughly 10%, which might justify today’s elevated valuation for long-term investors. - The Base Case: Steady but Slowing Growth

A more conservative outlook assumes NVIDIA’s growth gradually decelerates to 15% per year, with the P/E ratio normalizing to 20 over time. In this scenario, the stock would likely remain range-bound, offering modest returns unless earnings surprises push valuations higher. - The Bear Case: Cyclical Downturn or AI Disappointment

The semiconductor industry is notoriously cyclical, and NVIDIA is not immune to downturns. If AI adoption fails to meet lofty expectations—or if a broader economic slowdown leads hyperscalers to cut capital expenditures—NVIDIA’s earnings could stagnate. In such a scenario, the stock could see a dramatic repricing, potentially falling to a market cap of $400 billion or lower (a 60% decline from current levels).

Key Risks That Could Derail the NVIDIA Story

While NVIDIA’s technological lead and market position are formidable, several risks could disrupt its growth trajectory:

- AI Return on Investment (ROI) Uncertainty

Many enterprises are still experimenting with AI, and it remains unclear whether the technology will deliver the transformative productivity gains that justify its high costs. If businesses scale back spending due to underwhelming results, NVIDIA’s growth could slow abruptly. - Competition Intensifies

NVIDIA’s competitors are not standing still. AMD’s MI300X GPUs are gaining traction in AI workloads, while tech giants like Google and Amazon are developing their own custom AI chips to reduce reliance on NVIDIA. Additionally, China’s push for semiconductor self-sufficiency—though hampered by export controls—could eventually erode NVIDIA’s dominance in certain markets. - Semiconductor Cyclicality

The chip industry has always been prone to boom-and-bust cycles. NVIDIA itself has experienced brutal corrections in the past, including a 90% drop during the 2008 financial crisis and a 50% plunge in 2022. If AI demand cools, the company could face a painful downturn as inventory builds up and margins compress. - Valuation Compression

Even if NVIDIA continues to execute flawlessly, its stock could underperform simply because today’s high multiples leave little room for error. A shift in investor sentiment—perhaps triggered by rising interest rates or a broader market correction—could lead to significant multiple contraction.

Investment Strategy: Patience Over FOMO

Given these risks and uncertainties, how should investors approach NVIDIA today?

For long-term believers in AI, NVIDIA remains the best pure-play investment in the space. The company’s technological moat, software ecosystem (CUDA), and relentless innovation make it the clear leader in AI hardware. However, buying at all-time highs carries inherent risks, and investors should consider waiting for a more attractive entry point. Historically, semiconductor stocks experience sharp pullbacks, and NVIDIA could see a better buying opportunity if macroeconomic conditions worsen or if AI hype temporarily fades.

For value-conscious investors, patience is key. NVIDIA’s valuation remains stretched, and a more conservative approach would involve waiting for either:

- A meaningful pullback (e.g., a 30%+ decline from current levels)

- Clear evidence that AI monetization is exceeding expectations (e.g., sustained 50%+ revenue growth beyond 2025)

Conclusion: A Legend in the Making, But Not Without Risk

NVIDIA’s journey from a gaming GPU company to the engine of the AI revolution is one of the most remarkable business transformations in recent memory. The company’s future remains bright, with AI still in its early innings and demand for high-performance computing showing no signs of slowing.

However, great companies do not always make great investments at any price. NVIDIA’s current valuation demands near-perfect execution and assumes that AI adoption will continue accelerating indefinitely. While this may happen, the stock’s risk-reward profile appears balanced at best—and skewed to the downside if growth falters.

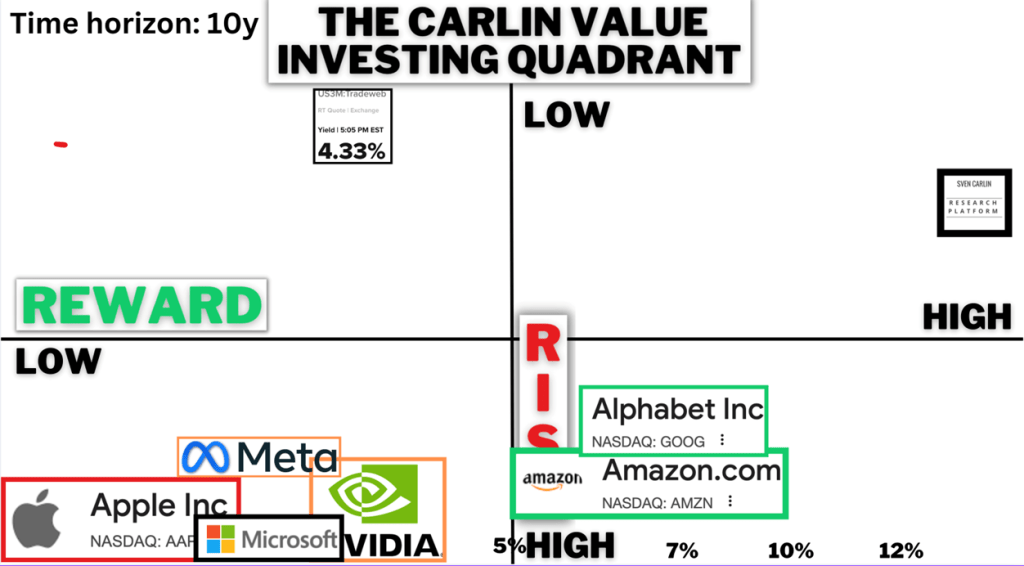

Value Investing Risk & Reward Quadrant (check all the stock analyses)