Nutrien Stock Analysis – 3 Keys & 3 Investing Scenarios (Cheap)

Nutrien Stock Analysis

Here is the Nutrien Stock Analysis video, article continues below:

Nutrien stock (NYSE:NTR, TSX:NTR) a company created in 2018 after the merger of Potash Corporation and Agrium. Potash Corporation was always regarded as a really good business due to its low-cost production and Agrium as a good retailer thanks to its scale and leading retail position across North America. This made the business always too expensive for me from an investing perspective. However, at the moment, Nutrien’s stock is trading at decade lows and therefore it deserves a another good look.

In this Nutrien stock analysis I’ll focus on the most important things when it comes to investing in Nutrien: potash, cash flows and the stock price in relation to possible future cash flows. I have created 3 investing scenarios that give a good risk and reward perspective for investing in Nutrien stock.

Nutrien Stock Analysis Key – Potash Market

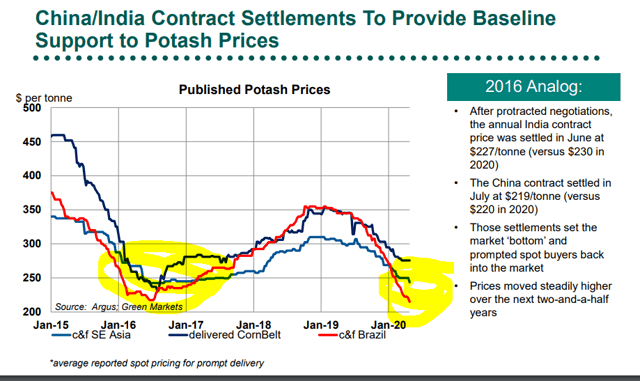

Potash is a cyclical commodity. When prices are high, lots of new investments usually lead to oversupply for a certain time and vice versa, when prices are low, there is limited investment that often leads on supply gaps.

We are currently in an oversupplied market with plenty of potential supply within the market. Just Nutrien can increase production by 6 Mtpa from existing mines without high costs. Until demand grows enough to cover for the current oversupply, potash prices can remain depressed.

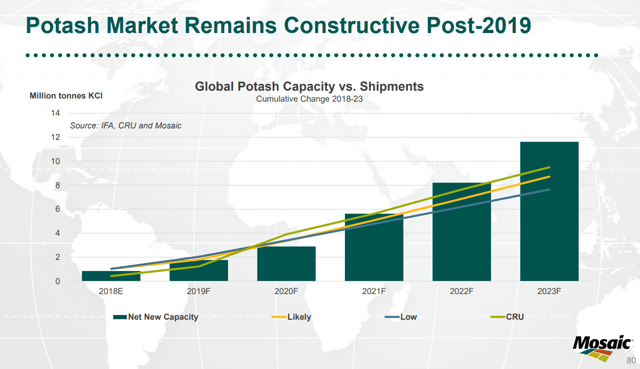

Given the net new capacity potentially coming into the market shown in the chart above, it is likely potash prices will remain subdued for years to come and that is also why investment banks downgraded Nutrien stock on ‘lower for longer’ potash prices.

So, it is unlikely that we will see a boom in potash prices and a subsequent boom in Nutrien’s stock price in the coming years like it was the case in 2008 or in 2011 when potash prices reached $800 per ton.

Nutrien stock – potash fundamentals

But, investing is not about catching an uptrend in a commodity. Investing, and especially value investing, is finding investments where the risk of things getting worse is low, which leaves the upside to unknown possible positives and long-term structural trends. With Nutrien, it is unlikely things will get worse because the company is a low-cost producer of potash, it has a good retail business and it is likely demand for food will grow in the future.

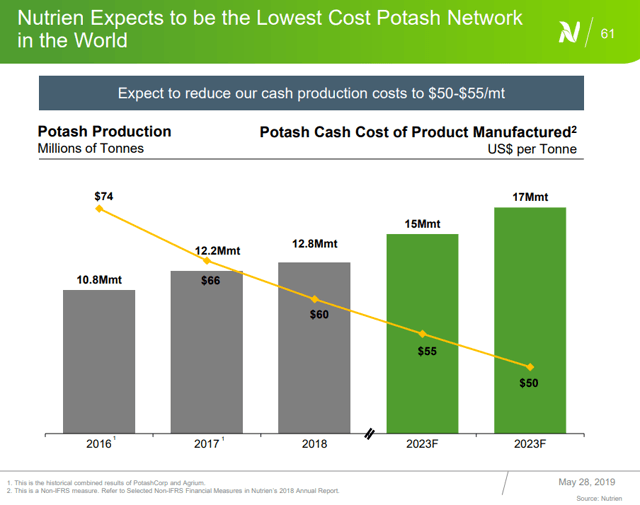

You might think that with cash production costs at $50, potash prices at $250 are still very high and there is much more room to fall. Well, cash costs are only one part of the equation.

If we look at one of the largest possible potash projects coming into the market, BHP’s Jansen project, the total cost to build the mine is expected to be around $5.7 billion to produce 4 million tons per year. If you wish to just get your investment back in 10 years, then you need a price of potash of $142.5 per ton over 10 years just to cover for the initial investment ($5.7 billion divided by 40Mtpa (10 years of production) = $142.5/t). Add approximate cash mining costs of $60, taxes and other costs, and you quickly get a minimum of $200 per ton just to break-even on mining potash.

This is important because it is unlikely for potash prices to fall below $200 – $250 per ton and stay there for longer which allows us to calculate Nutrien’s cash flows with a margin of safety.

Nutrien Stock Analysis – Cash Flows

Over the last two years, with potash prices between $250 and $350, Nutrien achieved free cash flows of $2 billion per year and, given the last guidance, it is likely they will do the same in 2020.

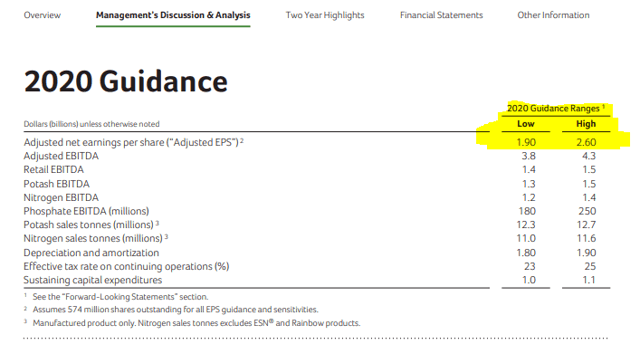

2020 guidance is for $3.8 billion in EBITDA. If we deduct $0.6 billion for interest payments, $0.2 for tax alongside $1.8 billion of depreciation, earnings should be at $1.1 billion. Thus, we come to around $2 in EPS.

On cash flows, if I add the $1.8 billion in depreciation back and deduct the $1 billion in CAPEX, I get to almost $2 billion in cash flows. That is $3.5 in cash flow per share. If they pay out 50% of that, it is enough to sustain the dividend of $1.8 per share that currently gives a yield of 4.71%. They will likely do more buybacks and invest part of the free cash flow into growth and investors should expect additional future returns.

All in all, $2 billion of free cash flows per year on a market capitalization of $21 billion leads to high single digit investment returns. An attractive proposition in the current environment.

Given Nutrien’s retail business that should make money no matter fertilizer prices, the $650 million yearly synergies thanks to the merger and the extremely low cost production that leads to high margins, it is unlikely for the dividend to be cut and it is unlikely that Nutrien’s cash flows ever fall into negative territory. Therefore, Nutrien looks like a low risk long-term investment at the moment. But, let’s put things into a market perspective too.

Nutrien stock price forecast and investment perspective

I have created 3 investing scenarios for Nutrien’s stock depending on their short to medium cash flows which is usually what the market focuses on.

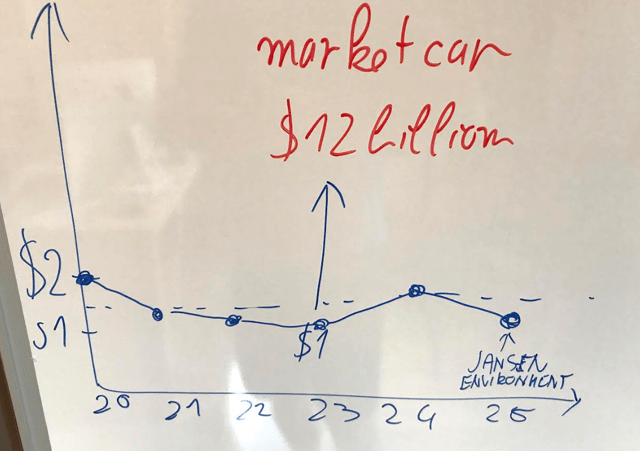

Nutrien stock price forecast – negative scenario

In the negative scenario, one where let’s say BHP decides to go onward with their Jansen project and put it into production by 2025, it is likely potash prices will remain closer to $200 rather than $300. In that case, and alongside some other business weaknesses, we could see Nutrien’s cash flows fall to $1 billion that would be just enough to sustain Nutrien’s dividend.

X-axis year, y-axis FCF

If that happens, given the current valuation, we could assume the market would apply a 10 to 12 free cash flow ratio to the stock and we could see Nutrien at a market cap of $12 billion. This is also the biggest risk when it comes to investing in Nutrien stock and one you should keep in mind before investing. I am not saying it will happen, just that it can happen. In any case, even with the negative developments in the market, it looks like Nutrien’s dividend would not be in danger.

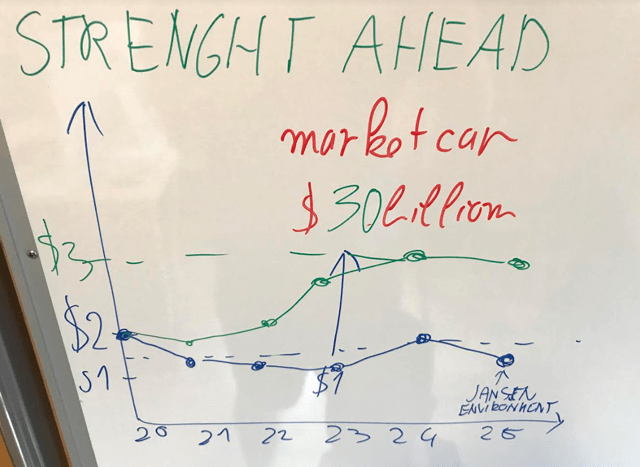

Nutrien stock price forecast – base case scenario

In the most likely scenario, cash flows might be subdued for a year or two, but thanks to global population growth and growing demand for food alongside Nutrien’s operational growth activities, cash flows should steadily rise and reach $3 billion in the future. This would likely push Nutrien’s dividends and the stock price higher.

In the above scenario, I would not be surprised to see Nutrien’s market cap above $30 billion in a few years. This, alongside the dividend, would give investors double digit returns from investing in Nutrien stock now.

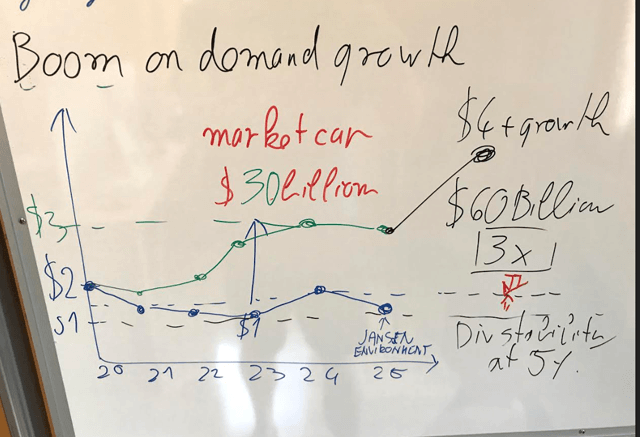

Nutrien Stock Price Analysis – Best case scenario

Within the boom scenario, one where Nutrien is capable to bring its idled production online and sell potash at high prices, cash flows could easily surpass $4 billion and more, that alongside some market exuberance due to likely higher buybacks and dividends, could easily lead to a market cap of $60 billion and above.

All in all, the investing scenario is positive for Nutrien, the business is a good business with low cost production and conservative management which is not a bad thing in the current environment. See how it fits your portfolio.

If you with to read my full 50 page report/notes on Nutrien, you can find it here for free as part of my Research Platform.

If you wish to read more stock analyses like these, please check the Stock Analysis part of my blog.

To receive these in your inbox, please subscribe to my newsletter. Thank you!