Microsoft Stock: A Comprehensive Analysis of Growth Prospects and Valuation Concerns

If you want a deep dive into Microsoft stock, watch the full video about the Magnificent 7 Stocks:

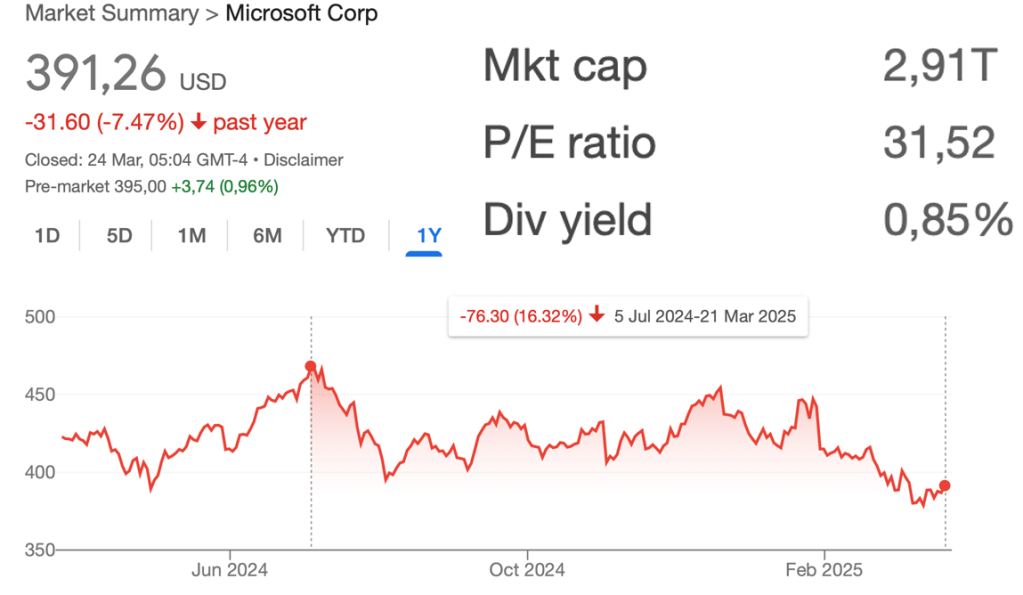

As one of the world’s most valuable companies and a cornerstone of the technology sector, Microsoft Corporation (NASDAQ: MSFT) presents investors with an intriguing case study in balancing exceptional business performance against demanding market expectations. The company’s recent 16% pullback from its all-time highs has sparked renewed debate among analysts and investors about whether this represents a buying opportunity or the beginning of a more significant valuation recalibration.

The Microsoft Growth Engine: Strengths and Recent Performance

Microsoft’s business transformation under CEO Satya Nadella has been nothing short of remarkable. Over the past decade, the company has successfully shifted from being primarily dependent on its legacy Windows operating system to becoming a diversified tech powerhouse with three dominant business segments: Productivity and Business Processes (including Office and LinkedIn), Intelligent Cloud (Azure), and More Personal Computing (Windows, Xbox, and devices).

This strategic pivot has yielded impressive results. Over the last five years, Microsoft’s stock has delivered a 100% return, significantly outperforming both the broader market and many of its tech peers. The company’s financial performance has been equally strong, with consistent revenue growth averaging 12% annually and net income expanding at a 10% clip. These growth rates are particularly impressive given Microsoft’s massive scale, with annual revenues now exceeding $200 billion.

The AI Imperative: Microsoft’s Big Bet

Microsoft’s current strategy centers on artificial intelligence, with the company making massive investments to position itself as the leading enterprise AI platform. The company’s early and prescient investment in OpenAI, the creator of ChatGPT, has given it a significant first-mover advantage in the generative AI space. Microsoft is rapidly integrating AI capabilities across its product suite, from GitHub Copilot for developers to Microsoft 365 Copilot for business users.

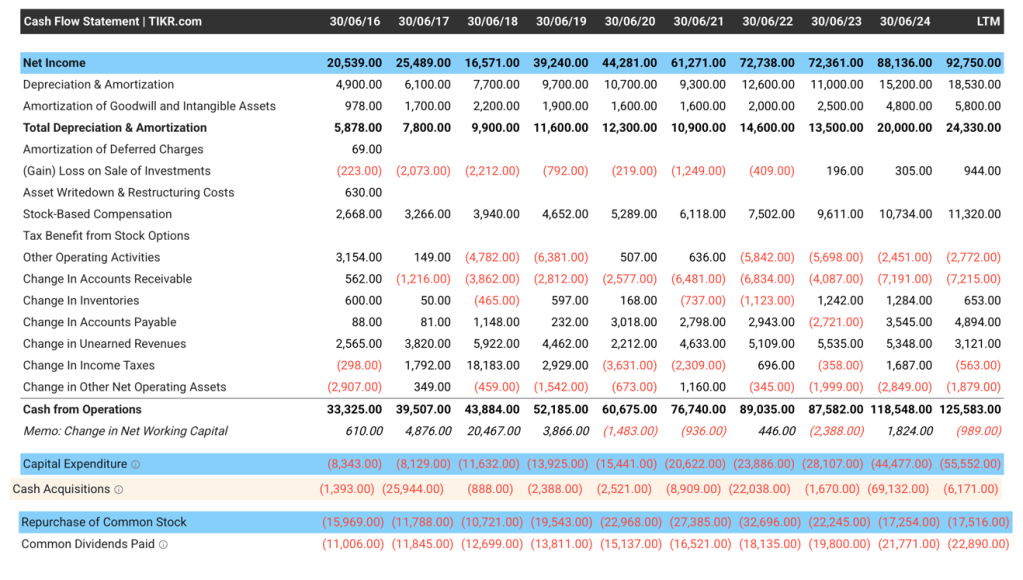

However, this AI leadership comes at a substantial cost. Microsoft’s capital expenditures have ballooned from $15 billion annually just a few years ago to a projected $55 billion in the current fiscal year. This dramatic increase reflects the enormous infrastructure requirements of AI computing, particularly the need for data centers packed with expensive, high-performance GPUs. While these investments may pay off handsomely in the long run, they are putting significant pressure on Microsoft’s free cash flow in the near term.

Financial Health and Capital Allocation

Microsoft maintains a fortress balance sheet, with approximately $80 billion in cash and equivalents. However, the company’s capital allocation priorities have shifted noticeably in recent years. The $70 billion acquisition of Activision Blizzard, completed in late 2023, represented Microsoft’s largest deal ever and signaled its ambitions in the gaming and metaverse spaces. Simultaneously, the company has reduced its share repurchase program from about $30 billion annually to closer to $20 billion as it redirects cash toward growth initiatives.

The company’s dividend, while growing steadily, remains modest with a yield of just 0.7%. This reflects Microsoft’s preference for reinvesting in growth opportunities rather than catering to income-focused investors. The dividend has grown at an 8-10% annual rate in recent years, a pace that seems sustainable given the company’s cash flow generation.

Valuation Concerns: Is the Stock Overpriced?

Microsoft’s valuation multiples have expanded significantly in recent years, reflecting both its strong execution and the market’s enthusiasm for its AI potential. The stock currently trades at approximately 35 times forward earnings and 30 times free cash flow – premium multiples that assume continued strong growth.

A detailed discounted cash flow analysis suggests that Microsoft’s intrinsic value is highly dependent on growth assumptions. Under a base case scenario assuming 8-10% annual earnings growth and a terminal multiple of 20x, the stock appears overvalued by about 30%. Even in a more optimistic scenario with 10-12% growth and a 25x terminal multiple, the upside appears limited at current prices.

The stock’s earnings yield of about 2.5% compares unfavorably with the 4.2% yield available on risk-free 10-year Treasury notes, highlighting the premium investors are paying for growth potential. This valuation gap could become problematic if interest rates remain elevated or if Microsoft’s growth fails to meet expectations.

Competitive Landscape and Risks

While Microsoft enjoys strong competitive positions across its businesses, the company faces several significant challenges:

- Cloud Computing Competition: Amazon Web Services remains the leader in public cloud infrastructure, while Google Cloud is growing rapidly and making significant AI investments of its own.

- AI Monetization: It remains unclear how quickly enterprises will adopt and pay for AI capabilities, and whether these will be additive to or simply replace existing software spending.

- Regulatory Scrutiny: Microsoft’s size and influence have drawn increasing attention from regulators worldwide, particularly following the Activision acquisition.

- Execution Risk: Integrating massive AI capabilities across Microsoft’s vast product portfolio while maintaining quality and security is an enormous operational challenge.

Investment Outlook and Recommendation

Microsoft represents one of the highest-quality businesses in the technology sector, with unmatched enterprise relationships, recurring revenue streams, and a proven ability to adapt to technological shifts. The company’s early leadership in enterprise AI positions it well for the next phase of digital transformation.

However, at current valuation levels, much of this potential appears already priced into the stock. Investors are paying a premium for growth that, while likely to materialize over time, may not exceed the market’s already lofty expectations. The combination of elevated multiples, rising capital intensity, and macroeconomic uncertainty suggests that patience may be rewarded.

For long-term investors already holding Microsoft shares, maintaining positions makes sense given the company’s exceptional quality and growth prospects. However, new investors may want to wait for a more attractive entry point, potentially in the $350-$380 range, which would represent a 20-25% discount to current levels and provide a more comfortable margin of safety.

The coming quarters will be critical in assessing whether Microsoft’s AI investments are generating the expected returns. Key metrics to watch include Azure growth rates, adoption of AI-powered products like Copilot, and capital expenditure efficiency. Until these metrics demonstrate clear acceleration, the risk/reward profile appears balanced at best.

Conclusion: Quality Comes at a Price

Microsoft stands as a testament to how a mature technology company can reinvent itself and continue to drive innovation. Its strategic positioning in cloud computing and artificial intelligence is unmatched among legacy tech firms, and its financial resources provide ample flexibility to navigate an uncertain economic environment.

That said, even the best companies can become overpriced. At current levels, Microsoft’s stock appears to discount nearly perfect execution of its AI strategy, leaving little room for disappointment. While the company’s long-term prospects remain bright, investors would be wise to be selective about their entry points. In the volatile world of tech investing, patience and discipline often prove more valuable than enthusiasm and FOMO.

As we watch Microsoft navigate this critical transition period, the fundamental question remains: Can the company grow into its valuation, or will the stock need to come down to meet reality? Only time will tell, but for now, a cautious approach seems prudent.

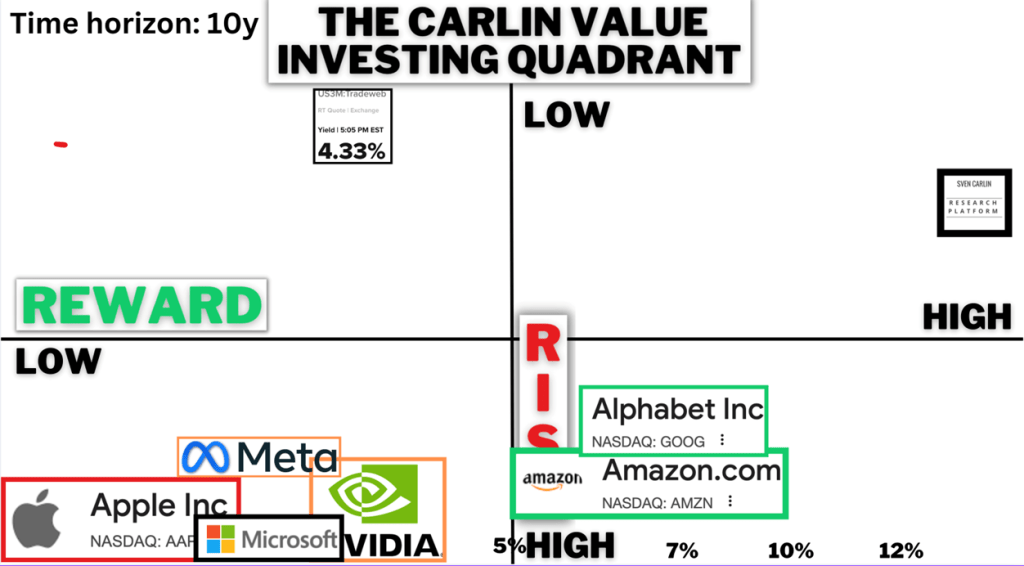

Value Investing Risk & Reward Quadrant (check all the stock analyses)