Meta Platforms: A Comprehensive Analysis of a Tech Titan at a Crossroads

If you want a deep dive into Meta stock, watch the full video about the Magnificent 7 Stocks:

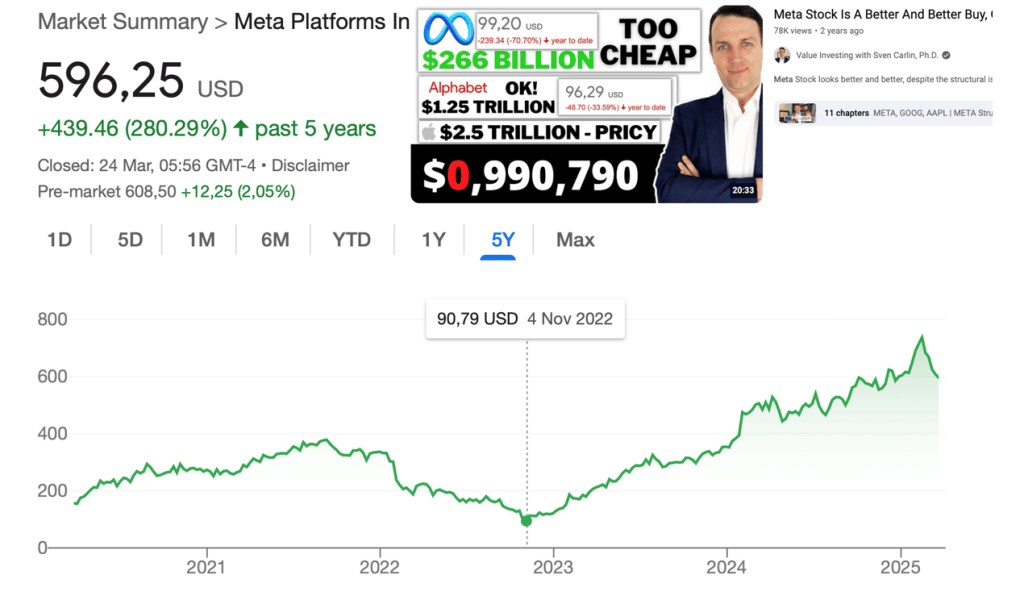

Meta Platforms (NASDAQ: META) stands as one of the most compelling case studies in modern technology investing, embodying both the extraordinary potential and inherent risks of dominant digital platforms. The company’s journey from its 2022 nadir – when shares traded below $100 amid widespread skepticism – to its recent highs above $700 represents more than just a market recovery; it reflects a fundamental transformation in how investors perceive the social media giant’s long-term value proposition.

The Remarkable Financial Turnaround

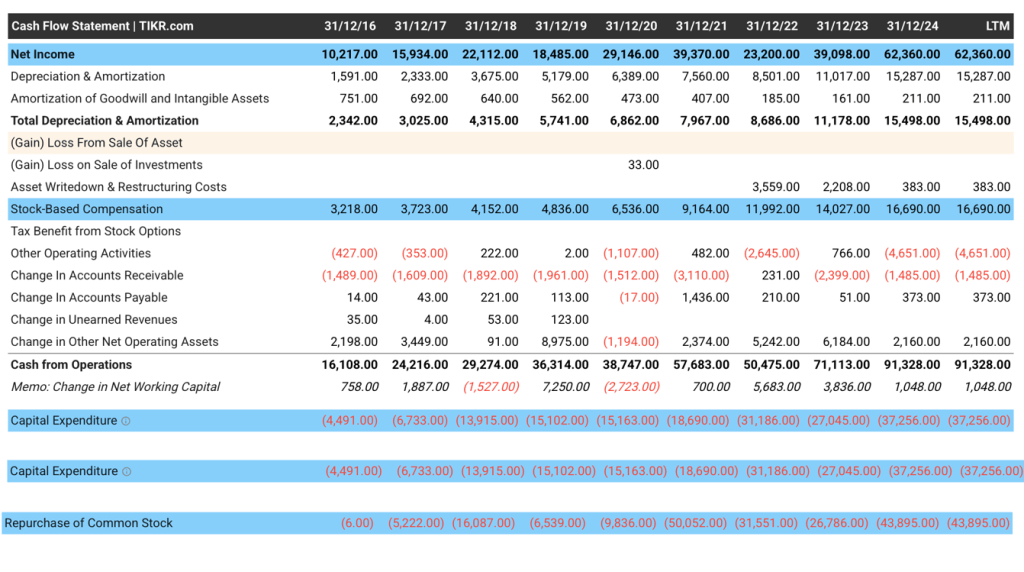

Few companies have engineered as dramatic a financial rehabilitation as Meta achieved between 2022 and 2024. What makes this transformation particularly noteworthy is that it occurred against a backdrop of significant technological disruption (the rise of AI) and macroeconomic uncertainty. The numbers tell a striking story:

Revenue growth reaccelerated from near-stagnation to double-digit percentages, while net income more than tripled from approximately $20 billion to over $60 billion. This profit explosion resulted from a combination of factors: improved advertising technology leveraging AI, stringent cost discipline that saw headcount reductions of more than 20%, and a strategic shift toward higher-margin revenue streams.

Perhaps most impressively, Meta achieved this while simultaneously making massive investments in artificial intelligence infrastructure and continuing to fund its Reality Labs division’s metaverse ambitions. The company’s operating margins, which had compressed to the mid-20% range during its spending peak, rebounded to exceed 40%, demonstrating that Zuckerberg’s “Year of Efficiency” was more than just a temporary cost-cutting exercise.

The AI Pivot: From Metaverse to Machine Learning

Meta’s strategic focus has undergone a subtle but significant evolution. While the company maintains its long-term bet on the metaverse through its Reality Labs division, the overwhelming emphasis has shifted to artificial intelligence. This recalibration reflects both technological realities and market demands:

The development of Meta’s AI assistant represents an attempt to create what could become the primary interface for billions of users across its platforms. Unlike standalone chatbots, Meta’s AI benefits from deep integration with WhatsApp, Messenger, and Instagram – giving it immediate access to an enormous user base.

Behind the scenes, Meta is making substantial investments in custom silicon through its Meta Training and Inference Accelerator (MTIA) chips. These proprietary processors aim to reduce reliance on expensive Nvidia GPUs while optimizing for Meta’s specific AI workloads. The company’s open-source AI strategy, exemplified by its Llama large language models, simultaneously advances the field while strengthening Meta’s position as an AI leader.

Advertising Engine: Still the Core Profit Driver

Despite all the futuristic ambitions, Meta’s financial health remains firmly rooted in its digital advertising business. The company has demonstrated remarkable adaptability in this core segment:

Through sophisticated use of AI, Meta has improved ad targeting and measurement capabilities, enabling better returns for advertisers. This has supported both increased ad loads (particularly in Reels) and higher pricing. The Instagram platform continues to evolve, with commerce features and short-form video helping maintain user engagement against TikTok’s competition.

WhatsApp, long considered an under-monetized asset, is beginning to contribute meaningfully through click-to-message ads and business messaging services. This represents a potentially massive untapped revenue stream as the platform’s nearly 3 billion users gradually become more commercialized.

Valuation Considerations: Growth Versus Margin of Safety

Meta’s valuation presents investors with a complex calculus. At current levels near $700 per share, the stock trades at approximately:

- 25x forward earnings

- 20x free cash flow

- 7x revenue

These multiples appear reasonable relative to Meta’s growth profile and competitive position, but leave little room for error. A discounted cash flow analysis suggests the stock is pricing in sustained high-single-digit revenue growth and stable margins – achievable but not guaranteed projections.

The company’s massive share repurchase program (over $40 billion annually) provides meaningful support to earnings per share growth, but also raises questions about capital allocation priorities at these valuation levels. With net cash exceeding $60 billion, Meta maintains ample flexibility, but investors might prefer more disciplined deployment of this war chest.

Risk Factors: Navigating an Uncertain Future

Several material risks could derail Meta’s growth trajectory:

Regulatory pressures continue to mount globally, particularly in the European Union where the Digital Markets Act imposes significant operational constraints. In the U.S., potential legislation targeting algorithmic content delivery or data privacy could force costly business model changes.

Technological disruption looms as AI-powered search and assistant products (from competitors like Google and OpenAI) could potentially bypass traditional social media interfaces. Meta’s ability to maintain its position as a “must-buy” for advertisers in this evolving landscape remains unproven.

Cultural and generational shifts pose another challenge, as younger users increasingly favor TikTok-style content consumption patterns. While Instagram Reels has successfully countered some of this threat, maintaining platform relevance requires constant innovation.

Investment Outlook: Quality at a Price

Meta represents one of the highest-quality businesses in the technology sector, with:

- Unparalleled scale (3.5 billion+ monthly users across its apps)

- Best-in-class profitability

- A management team that has demonstrated adaptability

- Strong balance sheet and cash generation

However, at current valuations, much of this quality appears already priced in. The stock offers limited margin of safety should growth slow or should AI investments fail to generate adequate returns. While long-term investors may continue holding core positions, new money might wait for one of the periodic pullbacks that have characterized Meta’s volatile trading history.

The ideal entry point would be in the $500-550 range, which would represent:

- A 20%+ free cash flow yield

- 18-20x forward earnings

- Better risk/reward balance for long-term holders

Conclusion

Meta’s extraordinary turnaround from $100 to $700 serves as a powerful reminder of the market’s tendency to overreact in both directions. While the company has solidified its position as a digital advertising powerhouse and made impressive strides in AI, current valuations appear to reflect these achievements fairly.

Investors would be wise to maintain disciplined valuation standards, remembering that even the highest-quality businesses become risky investments when purchased at elevated multiples. Meta will likely remain a dominant force in digital communication and advertising for years to come, but the optimal time to increase exposure may come during the next market pessimism rather than at current optimistic levels.

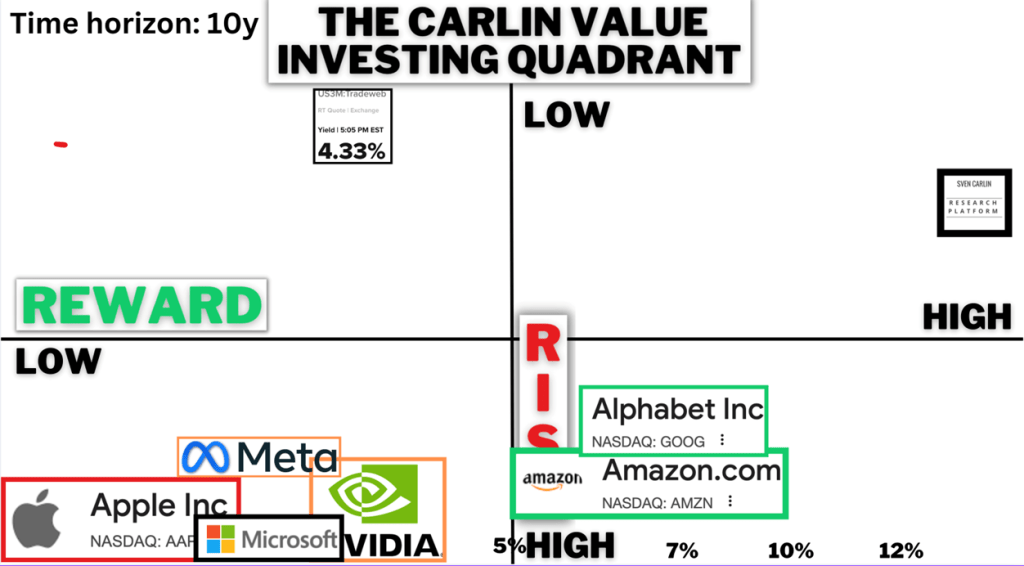

Value Investing Risk & Reward Quadrant (check all the stock analyses)