Medtronic Stock Analysis – A Great Business but a Mediocre Investment

Medtronic Stock Analysis – MDT

Medtronic stock analysis is part of a series of analyses I made on growth stocks that compound over time. The best stock out of the list to invest in was Visa. You can check my Visa stock article and also the tool best used to analyze the risk and reward when it comes to growth stocks, the delta of the delta.

Medtronic plc. is a medical device company that generates the majority of its sales and profits from the U.S. healthcare system. However, the company is headquartered in the Republic of Ireland for tax purposes. An example of products are transcatheter aortic valves, advanced stapling tools, and neurovascular stent retrievers.

Healthcare is a hot sector with strong tailwinds, plus the company has acquired Kanghui Holdings with the target to distribute its products in China where it sells already for more than $1 billion.

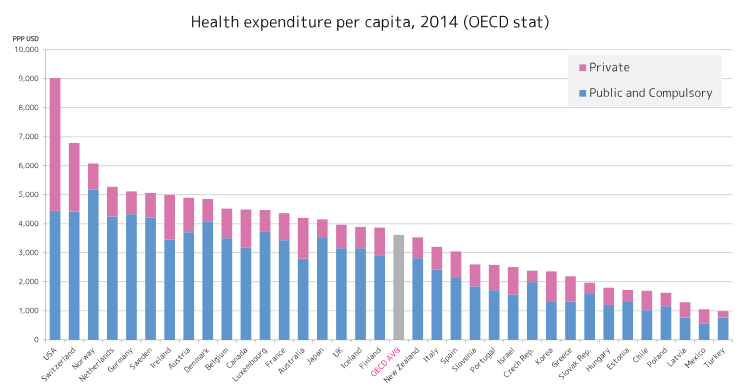

The key risk for Medtronic is an improvement in the efficiency of the US healthcare system. It is unlikely that it will happen, but Medtronic is banking on the fact that the US spends double of what comparable countries spend on healthcare.

Spending on healthcare per country

Source: OECD

Now, given the business models and psychological effect of spending on healthcare, it is likely that other countries reach what is spend in the US, but it is also possible that the US will be forced to cut on unnecessary spending.

Nevertheless, Medtronic looks very good. Revenue growth is steady while the growing free cashflows allow for higher dividends.

Medtronic stock financials

Source: Medtronic Morningstar

Given that the company operates in a very delicate sector and invests about 7% of its revenue into R&D, we can say it has a moat. The highly engineered medical devices are not a market one can easily enter. Plus, it is diversified across many fields.

Medtronic stock valuation

We can assume the company is going to continue to grow at a rate around 4%. Alongside the current PE ratio of 20 that gives a business yield of 5%, you can expect long-term returns to be in the high single digits. Given the quality of the business, the stability and defensiveness of it, a 7 to 9% yearly return should be a great deal compared to long-term risks. Therefore, it is very likely the stock will continue to compound for a long time.

Medtronic stock price remarkable past performance

Perhaps it will not compound at double digit rates as it did in the 1990s, but a steady growth like it was the case in the last two decades is what you can expect.

This was an example of a simple stock analysis, but that is what investing should be; simple. If you wish to learn more about investing, so that you can too quickly analyze businesses and know whether the business is something for your portfolio, feel free to check my FREE, I repeat, FREE, Comprehensive Stock Market Investing Course.