JDE Peets: A Comprehensive Analysis of the World’s Leading Coffee and Tea Company

Table of Contents

Check out the full video on YouTube, if you prefer reading however, keep scrolling.

JDE Peets, one of the largest coffee and tea company in the world, is currently trading at a price-to-earnings (P/E) ratio of 15 with a dividend yield of 4.28%. Despite its challenges since going public in 2020, recent developments suggest that the company may be undervalued, presenting potential upside for long-term investors. In this article, we’ll explore the fundamentals of JDE Peets, assess its financial health, and evaluate its intrinsic value to determine whether it’s a good investment opportunity.

JDE History

JDE Peets was formed in 2020 through the merger of Douwe Egberts, a well-established Dutch tea and coffee brand, and Peet’s Coffee, an American coffee company. Since going public, the stock has struggled to gain traction, but several key developments signal potential for growth. One major event was when JDE Peets’ majority shareholder increased their stake in the company by purchasing Mondelez’s 16% share for 25 euros per share, a significant premium over its current trading price of 16 euros. This transaction implies that the private value of the company could be as high as 25 euros per share, offering a clear margin of safety for potential investors.

Business Overview

JDE Peets owns a portfolio of iconic global brands, including Senseo, Pickwick Teas, and the flagship Douwe Egberts Coffee, as well as the popular Peet’s Coffee brand. The company has made strategic acquisitions such as Caribou Coffee and Maratha Coffee. Though these acquisitions were made at relatively high multiples, they have helped JDE Peets expand its market presence. Despite some challenges, the company continues to grow its footprint across the globe, with a particularly strong focus on emerging markets.

While JDE Peets competes with major players like Nestlé and Starbucks, its diversified portfolio and vertically integrated supply chain give it a solid foundation for continued growth. The company’s focus on high-quality products, combined with efficient operations, positions it to navigate the competitive coffee and tea landscape.

Leadership and Management

JDE Peets recently faced a leadership transition with the appointment of Rafael Oliveira as CEO. Oliveira, who previously served as Kraft’s international president, brings a wealth of experience and leadership to the company. This management change has been welcomed by investors, as it is seen as a step in the right direction after some uncertainty under previous leadership. The company’s holding structure, with a focus on long-term cash flows, also suggests that JDE Peets is well-positioned to execute on its growth strategy while maintaining stability.

Financial Performance

JDE Peets has experienced steady growth in organic sales, with a reported 3% increase in the last quarter. The company has shown good profitability and robust free cash flow, driven by price growth and an expanding presence in emerging markets. Gross profits have benefited from favorable pricing and mix shifts, and JDE Peets is also focusing on reducing its debt, which currently stands at nearly 5 billion euros. The company’s debt is manageable, with an average cost of debt at 1.1%, making it an attractive option for acquisitions and expansion.

However, JDE Peets has also faced challenges with rising debt levels due to recent acquisitions. While the company is targeting a 2.5x leverage ratio, it plans to pause share buybacks until its debt is reduced. The company’s strategy is to use free cash flow to stabilize its balance sheet while maintaining its dividend payout and pursuing growth opportunities.

Intrinsic Value and Valuation

To assess the intrinsic value of JDE Peets, we used a discounted cash flow (DCF) approach, considering earnings per share (EPS) of 1.1 euros, a 5% growth rate, and a 10% discount rate. Based on these assumptions, the intrinsic value comes out to approximately 15 euros per share. This is very close to the current trading price of 16 euros, indicating a modest margin of safety.

A 9-10% annual return is possible from this investment if the company maintains steady growth. Should macroeconomic conditions improve, particularly with favorable inflation or interest rate environments, the potential return could rise to 12% or more. However, there is always the risk of slower growth and a potential reduction in the P/E ratio, which could lead to a downside of up to 30% from the current price.

Intrinsic Value Calculation Template by Sven Carlin (free download on Value investing course)

Margin of Safety

The key factor driving the margin of safety is the recent purchase of Mondelez’s 16% stake for 25 euros per share, which is 70% higher than the current market price. This suggests that private investors may view the company’s value as significantly higher than its current public market price, providing a cushion in the event of a takeover or increased investor interest.

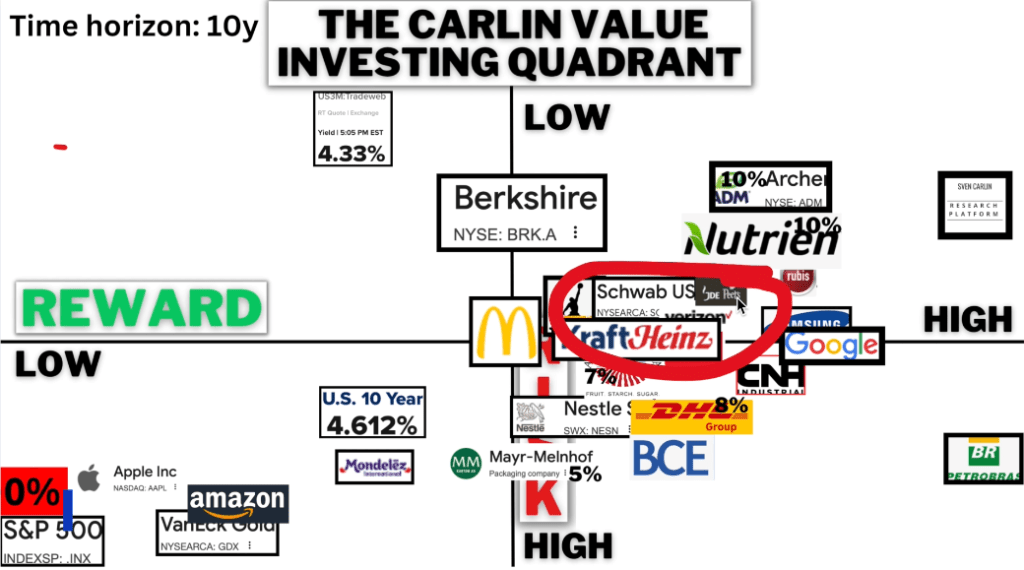

Value Investing Risk & Reward Quadrant (check all the stock analyses)

Dividend and Capital Allocation

JDE Peets has a stable dividend policy, with a payout ratio of approximately 65% of earnings. The company’s dividend yield of 4% offers an attractive income stream for investors while also positioning the company for long-term growth. Capital allocation priorities include paying down debt, pursuing acquisitions, and maintaining stable dividends. The company expects to generate 850 million euros in free cash flow, partly driven by the release of inventory.

Risks and Opportunities

While JDE Peets faces several risks, including competition from large global players like Starbucks and Nestlé, as well as volatility in commodity prices, there are significant growth opportunities. The global demand for coffee and tea continues to rise, particularly in emerging markets, which should help drive sales in the coming years. Additionally, the company’s vertically integrated supply chain, strong brand portfolio, and focus on profitability provide a solid foundation for growth.

Conclusion

JDE Peets presents a compelling investment opportunity for value investors. Despite recent challenges and market volatility, the company’s strong brand portfolio, solid financial performance, and low valuation relative to its private value offer attractive upside potential. With a 4% dividend yield, steady growth prospects, and a margin of safety from recent transactions, JDE Peets could be a good addition to a diversified portfolio.