Is Verizon Stock a Good Investment? Analyzing the Dividend, Debt, and Intrinsic Value

Verizon stock analysis, contents:

Here is the video version of the VZ stock analysis, if you prefer reading, scroll below:

Verizon Communications Inc. (NYSE: VZ) has been a topic of interest for many investors, particularly those focused on dividend-paying stocks. Over the past five years, Verizon’s stock price has declined by 36%, while its dividend has consistently increased. This divergence raises important questions: Why is the stock falling despite rising dividends? Is Verizon a good fit for your portfolio? Let’s dive into the details to understand the company’s financial health, intrinsic value, and future prospects.

Verizon’s Performance

Verizon’s stock has under-performed over the last five years, declining by 36% while the broader market has doubled. Despite this, the company has maintained and even grown its dividend, offering a current yield of approximately 7%. This high yield has helped offset some of the stock’s decline for income-focused investors. However, five years of flat performance in a booming market is far from ideal.

With a market capitalization of $160 billion, Verizon remains a significant player in the telecommunications industry. But its stock performance has been weighed down by several factors, including high debt levels, intense competition, and rising interest rates.

Key Challenges With Verizon

- Heavy Debt Load

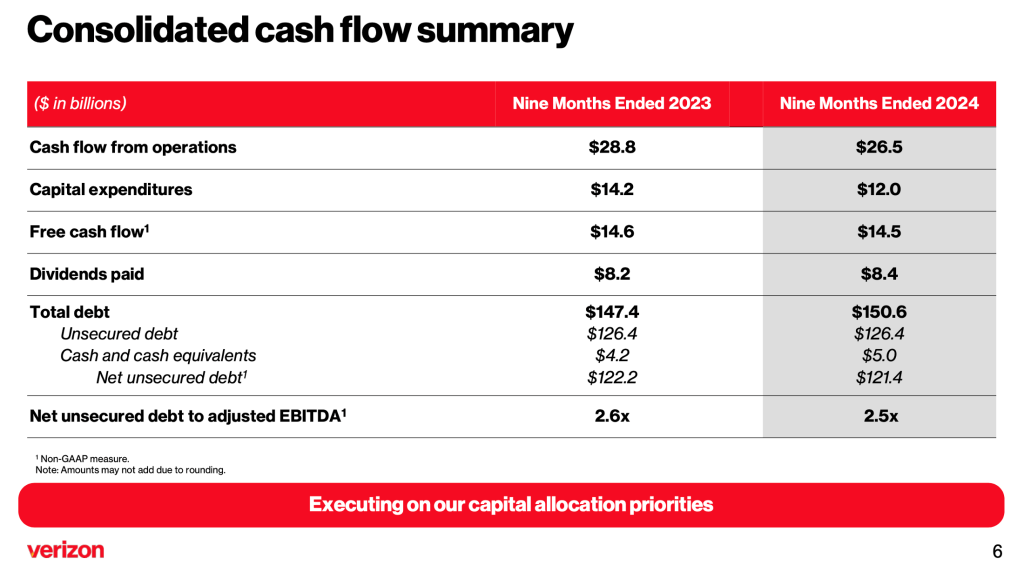

Verizon has invested heavily in its infrastructure, spending $200 billion over the past decade on 5G spectrum acquisitions, fiber expansion, and other initiatives. While these investments are necessary to remain competitive, they have also led to a substantial debt pile, now standing at $150 billion. The company’s recent $20 billion acquisition of Frontier Communications’ fiber assets adds to this burden. - Flat Revenue Growth

Verizon’s revenue growth has been stagnant, with total revenue remaining flat over recent years. While wireless service revenue has shown modest growth, it hasn’t been enough to offset declines in other areas. Cash flows from operations have also decreased by $2.3 billion, though capital expenditures have declined by a similar amount, keeping free cash flow stable. - Competition from T-Mobile

T-Mobile has been aggressively gaining market share, putting pressure on Verizon’s growth prospects. The telecommunications industry is highly competitive, with pricing wars and customer retention challenges impacting profitability.

Interest Rates and Verizon’s Stock Performance

Verizon’s stock is sensitive to interest rate movements. As a dividend-paying company with significant debt, rising interest rates have a dual impact:

- Higher Dividend Yield Expectations: When interest rates rise, investors demand higher yields from dividend stocks like Verizon. This has pushed Verizon’s dividend yield from 4.29% to 7% over the past few years, contributing to the stock’s decline.

- Increased Debt Costs: Verizon’s debt refinancing costs have risen sharply. For example, a $1 billion bond refinanced in 2025 at 0.85% will now cost 5%, significantly increasing interest expenses.

Conversely, if interest rates decline, Verizon’s stock could benefit. Lower rates would reduce debt costs and make the company’s dividend yield more attractive, potentially driving the stock price higher.

Intrinsic Value Analysis

Using a discounted cash flow (DCF) model, we can estimate Verizon’s intrinsic value based on its dividend growth and discount rate. Here’s a summary of the analysis:

- Current Dividend: $2.60 per share.

- Growth Assumption: If Verizon continues to grow its dividend at a modest rate, the stock is fairly valued at around $38, offering a 10% expected return.

- Best-Case Scenario: If interest rates decline and the required dividend yield drops to 5%, Verizon’s intrinsic value could rise to $50, offering a 12-13% return.

- Worst-Case Scenario: A dividend cut or stagnant growth could significantly reduce the intrinsic value. For example, if the dividend is cut to $1.50, the stock’s value could fall below $20.

(for more information on the intrinsic value template and Verizon intrinsic value calculation check here)

Risks to Consider

- Dividend Cut: The biggest risk for Verizon investors is a potential dividend cut. If the company struggles to manage its debt or faces lower-than-expected margins, a dividend reduction could severely impact the stock price.

- Interest Rate Volatility: Continued increases in interest rates could further pressure Verizon’s stock and dividend yield expectations.

- Competition: Intense competition, particularly from T-Mobile, could limit Verizon’s growth and profitability.

Is Verizon a Good Investment?

Despite its challenges, Verizon could be a compelling addition to a diversified dividend portfolio. The stock offers a high yield of 7%, and its infrastructure investments position it as a leader in 5G and fiber expansion. However, the risks associated with its debt load and interest rate sensitivity cannot be ignored.

For long-term investors, Verizon’s stock could provide steady income and potential capital appreciation if interest rates decline. However, those with a lower risk tolerance may want to approach with caution, given the potential for dividend cuts and further stock price declines.

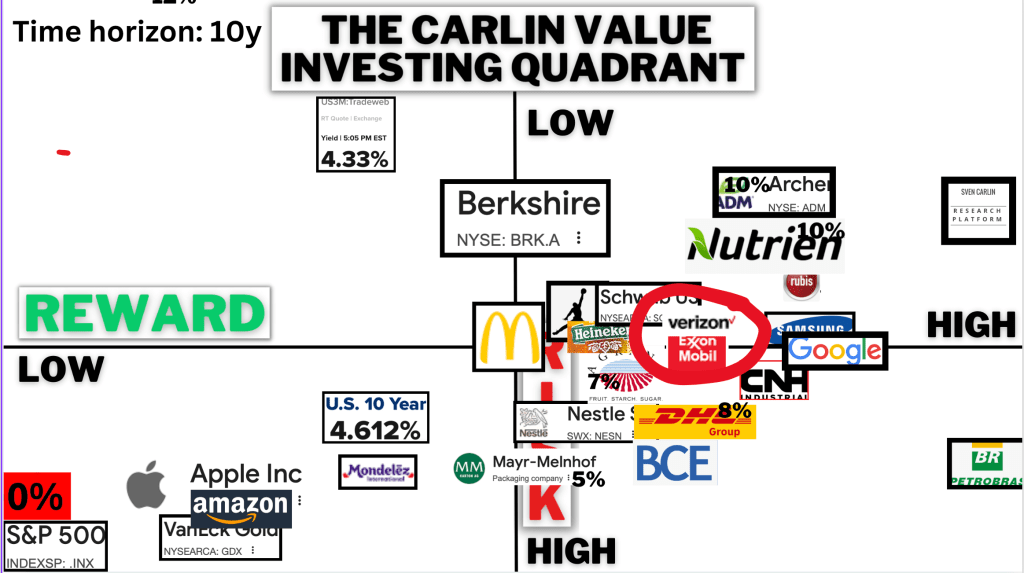

Verizon on the Value Investing Risk and Reward Quadrant

Compared to other investments, Verizon looks good thanks to the dividend yield but is also risky in line with the market’s risk.

(to learn more about the quadrant and check other analyses, check here: Value Investing Quadrant)

Conclusion

Verizon is a classic example of a high-dividend stock with significant risks. While its 7% yield is attractive, the company’s heavy debt, flat revenue growth, and sensitivity to interest rates make it a complex investment. For those willing to accept the risks, Verizon could be a valuable addition to a diversified portfolio, particularly in a declining interest rate environment. However, investors should closely monitor the company’s ability to manage its debt and maintain its dividend.

If you’re interested in exploring Verizon further, consider downloading our free intrinsic value calculator to run your own analysis.