Investing in Sugar – Südzucker AG Stock Analysis

Investing in commodities is tricky and many call me crazy for doing that. However, I don’t invest by buying an ETF, I invest by carefully analyzing long term trends and take advantage of short term irrationalities. By short term I mean up to 3 years, by long term I mean a decade.

This article will explain:

- How to approach investing in commodities by using sugar as an example (Sugar cycle analysis)

- How to take advantage of cyclicality and what the market doesn’t yet see (will you still eat sugar tomorrow? I hope not, but you probably will)

- Analyze a commodity stock Südzucker AG (SZU) (OTCKP: SUEZF) from a long term perspective

Contents

Investing in Sugar – Südzucker AG Stock Analysis

Commodity investing strategy – take advantage of long term cycles

Sugar price cycle

Sugar production costs

Sugar price forecasts

Sugar investing strategy

Südzucker AG (SZU) (OTCKP: SUEZF) Stock Analysis

Investment thesis

Commodity investing strategy – take advantage of long term cycles

Let me show you first the core of this investing strategy. The below figure plots SZU’s stock price and the price of sugar over the past 20 years.

Source: Macrotrends and author’s adjustments

The correlation is not perfect but if you would ask a 7-year-old kid, he would say it is. And such a long-term investing perspective is the starting point when investing in commodities. The key is than to look at all the possible margins of safety, who will go bankrupt in the sector, who is the lowest cost producer, and all the other cyclical factors affecting the sector. It is also important to have a clear strategy because nobody knows where the bottom is. On top of it all, some stocks might be considered sugar stocks, move in correlation to sugar prices, but have the minority of their revenue derived from sugar.

The point is that the market is cyclical and will always be cyclical. Those are natural forces that affect commodity markets and if you take a decade long approach to investing in commodities, you will achieve great returns by taking advantage of those long term market forces that eventually prevail. However, it is crucial that you do nothing for most of the time, something impossible to do for most investors. Let’s see what is going on with sugar.

Sugar price cycle

When production is higher than consumption with any commodity, things are not good for the respective commodity’s price.

Source: Sudzucker

Sugar is in oversupply and will remain so for at least a year or maybe two. This leads to low sugar prices as farmers dump what they have and there is no way around it. However, low prices, perhaps some bad weather might lower future production and then we will probably see higher prices again, like it was the case in 2015/16.

Source: Macrotrends

In the last 5 years, sugar prices have been extremely volatile. We are now at 50% of what the price was in 2016. This is explained by demand and supply. However, from a risk reward perspective you approximately know what is going to happen next. Low prices, lead farmers to plant something else and you get high prices next. Like it was the case in 2016.

A production decrease is expected but not enough to offset rising inventories.

Source: Sudzucker

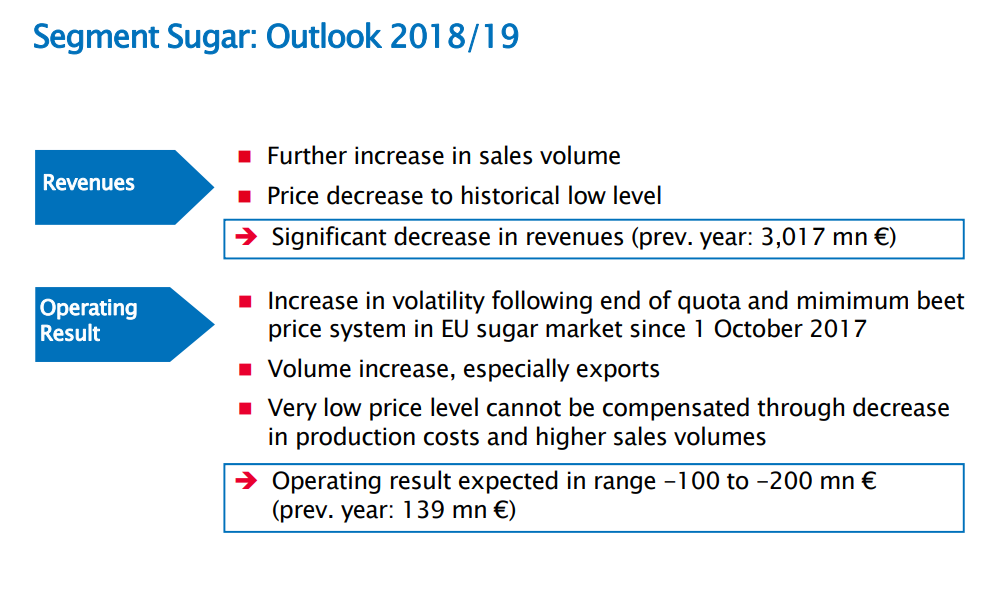

Of course, the above are just expectations where a drought might mix things up. However, the company SZU expects to see negative income from sugar operations next year.

Source: Sudzucker

As a long term investor, I price in the above and then already think beyond 2018/2019. What will be the case then? At some point in time, sugar producers will have to produce less to stay alive. SZU expects at least two difficult transition years so that is something to take into consideration because financial markets have a hard time thinking long term.

The easiest way to explain a cycle is to look at the cost. In the long term, the price of a commodity will fluctuate around the average cost that satisfies the demand. So, what are the average cost prices for sugar production around the world and is the long-term supply demand trend stable?

Demand for sugar is expected to grow steadily over the next decades, unfortunately for human health, but that is another topic.

Source: Sudzucker

Sugar production costs

According to Nordzucker: “At the current price level, there is hardly a sugar company in Europe which can still produce at a break-even,” Which means European production costs are above $12 cents per pound for the most efficient producers. The beet union is going nuts and warns how all producers are selling below cost. They require protection from cheaper production in Mercosur (another thing my taxes will pay but that is another story).

The EU levied production quotas in order to become an exporter of sugar which increased production and now you have overproduction.

Brazilian costs are around 10 to 14 cents per pound depending on the producer and Thailand is also there.

Sugar price forecasts

JSG Commodities forecasts prices to hit a low of 8 cents per pound. The European Association of Sugar manufacturers is also not positive and demands government action.

Other sugar producers foresee sugar prices continuing to be under pressure in the short term, still reflecting strong production from other countries, such as India and Thailand, resulting in an expected overall crop surplus. The magnitude of this surplus will depend on the size and the mix of the huge crop, which should have more ethanol production and significant impact on productivity due to the drier weather.

Sugar production is volatile and that is something to keep in mind.

Source: Bloomberg

Another good monsoon and there will be more pain for sugar. Drought and you will see prices spike.

Costs in India vary around Rs. 36.50 per kilo of sugar that is 16.59 per pound or 23 cents per pound. Given the bumper crops the costs must be lower but without the subsidies, hardly competing with Brazil.

All indicates that we are below balance prices. I don’t think people will suddenly stop to eat sugar so demand will remain stable at least. This leads to the next step which is to look at whether there are investing opportunities and the development of a strategy.

Sugar investing strategy

So, we know that sugar is in a downturn which is not sustainable over the long term. However, we also know that the negative earnings are only about to hit companies as most expect two years for the skies to clear.

This means that only the fittest will survive, there will be losses next year which will make things look ugly from an investing perspective where few like to invest in companies with negative earnings. But we have to find those companies that will have high positive earnings over the next decade which could lead to high dividends and higher stock prices when sugar prices turn up in the next cycle. Let’s see if SZU has what it takes.

Südzucker AG (SZU) (OTCKP: SUEZF) Stock Analysis

SZU is a holding company with diversified production.

Source: Sudzucker

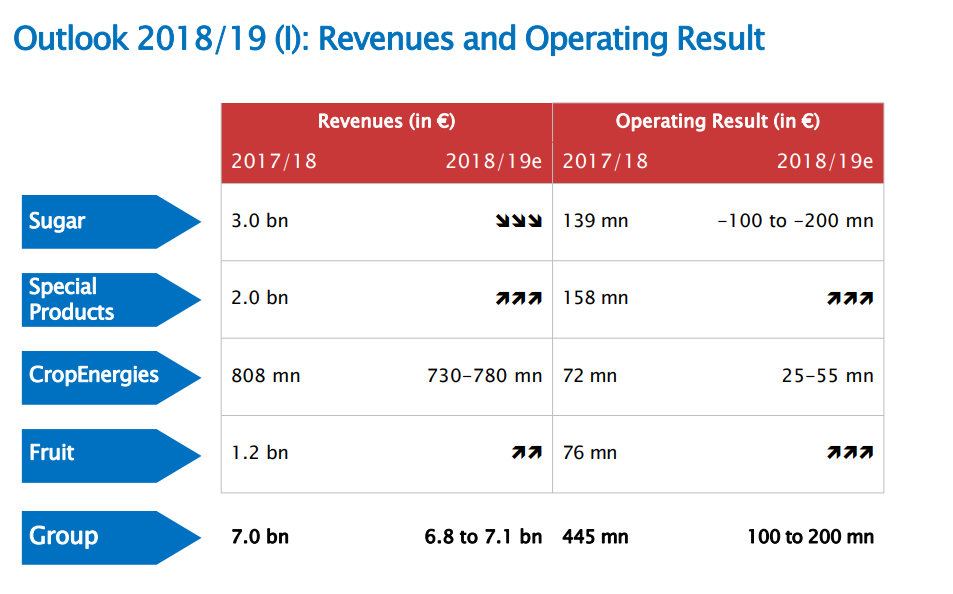

Sugar revenues are expected to decline more than 10% and the operating result turn from positive to negative. Special products and fruit will grow by more than 10% but it will not be enough to compensate for the decline in sugar revenues.

Source: Morningstar

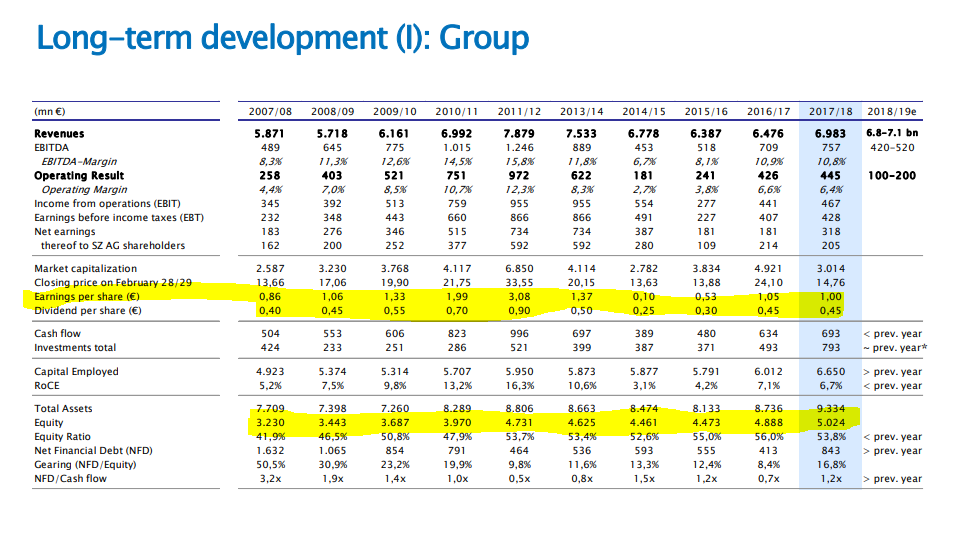

A two year slump and lower operating results by 75% will affect earnings and most importantly cash flows. If cash flows drop to 2015 levels, the dividend might still be sustained for one year as a EUR 0.5 dividend requires only 102 million in cash.

My concern is that in case of higher sugar prices, SZU’s net income doesn’t change much and will probably come to 500 million in operating income and 250 million in cash available for dividends which would be around 1.2 EUR per share. That would however be a 10% dividend yield that would propel the price to a yield of at least 5% in Europe. Think of a stock price above EUR 20 in such a case.

This means that the stock will probably go to 20 and above in the next few years as the cycle turns. It was trading above EUR 25 just a year ago and above EUR 30 in 2013.

The company has a stable balance sheet where only 43% of the assets are financed by debt.

Source: Sudzucker

Debt issues shouldn’t really be a concern given the long-term maturity.

Source: Sudzucker

The market cap is much higher when the dividend is growing or higher which shows how short term oriented the market is.

The investments next year will be high which will probably increase debt. However, the investments are mostly into starch.

They also have a pizza business with EUR 1 billion in revenue.

Could it be that the only reason this stock is this low is because it might go lower and the dividend might be cut?

Investment thesis

I know SZU is going to be at EUR 20 somewhere in the next 5 years, for sure in a decade. I need a 15% return which means the purchase price comes at EUR 10.98! Still one EUR to go down. However, it might go even lower which means you buy more at 9 and then at 7. Sell at 11 and sell the first position at 20 and collect dividend in the meantime. That would be a relative investment strategy but I am an absolute investor looking for business earnings, not just market returns. Never depend on markets for your returns, it doesn’t work well in the long term even if it did miracles in the last 35 years.

A look at earnings shows that the average earnings over the past decade were EUR 1.2 giving a current CAPE (cyclically adjusted price earnings ratio of 10). This implies a 10% long term return which is nice. Given that my required return is 15% per year, my entry point would be EUR 8. Given that few like European stocks at the moment, if sugar prices stay down for another year and we see pain and negative earnings in the sector with some dividend cuts, it is possible to see this at 8. Then it would be a great margin of safety investment no matter what happens. If DB goes bust and we see turmoil in Italy it might really happen.

When and if it gets closer to 8, I’ll take another look, dig deeper into the European beet industry and look at SZU’s subsidiaries. Given the German ownership I don’t think private equity funds will want to mess with this one and split it in pieces.

To conclude, this is a really good company at currently a relatively low price. I am waiting for an absolutely low price with a margin of safety. As I look at hundreds of companies per year, I am happy with finding a few that trade at such absolute low prices with large margins of safety. Given the amount of research I do, I find a few of them per year which are my buys. Check my research platform for more information about what and how I do.

SZU goes on my watch list and I’ll wait for an opportunity that might come in the next decade, as I cover the company I’ll understand it better and take advantage of possible opportunities.

STOCK MARKET RESEARCH PLATFORM LINK (TEST IT OUT – 30 day money back guarantee no questions asked)