Graftech Stock Price Analysis – High Uncertainty But Contracts Give It Low Risk

Why Did Mohnish Pabrai Buy Graftech Stock

- Graftech stock has the potential to be a ‘PE ratio of 1’ company. You are practically paying $700 million for $700 million in yearly free cash flows.

- The short-term outlook for steel is murky where the $2 billion in debt and total of $3 billion of contractual obligations represent a risk. Further, competition is intensifying in China.

- On the other hand, the company has $4.5 billion in revenues already contracted which mitigates the risk.

- If the company manages to survive short to medium term downturns, the upside is from 300% to 500%. A positive risk/reward investment.

Prefer watching? Here is the video analysis of Graftech Stock (article below)

Graftech stock overview

Graftech (EAF) is a provider of high-power graphite electrodes for the growing EAF’s (electric arc furnace) steel market. The company is an integrated producer as it owns Seadrift Coke L.P, that produces 75% of the petroleum needle coke EAF needs to produce graphite electrodes.

Source: Graftech

It is important to note that the company practically went bust in 2015, when Brookfield acquired it for $1.25 billion. Graphite electrode prices were around $2,600 per ton in 2016 while those are around $10,000 now. So, Brookfield bought in at the right time, reorganized the company, but mostly benefited from higher electrode prices.

Source: Graftech IPO S-1

The management moved quickly and switched from mostly selling on spot, to selling through long-term contracts in order to benefit from the temporarily high electrode prices.

Graftech stock value – margin of safety and PE ratio of 1

The management acted quickly to take advantage of the higher pricing environment and locked in 3 to 5 year take or pay contracts with almost 80% of their customers.

Source: Graftech Q2 Earnings Presentation

This means that over the next 4 years, we can expect the company to perform equally to this year thanks to those long-term contracts. Locked in revenue is at $4.5 billion.

Source: Graftech 10-Q

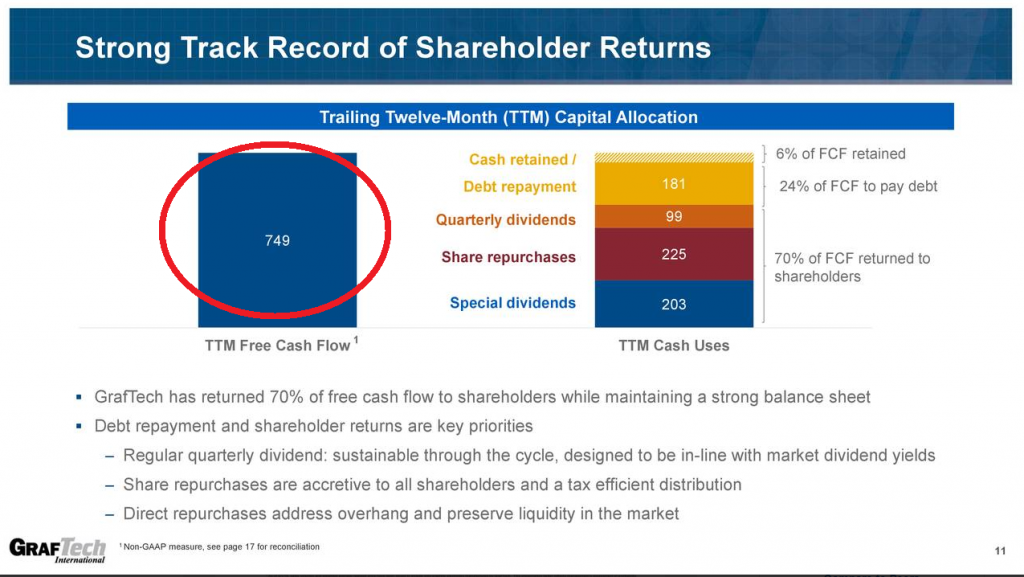

The take or pay contracts should lead to prolonged excellent performance as trailing twelve months free cash flows are $749 million.

Source: Graftech Q2 Earnings Presentation

Multiply $749 with 4, which is the minimum expected time these contracts will be in place, and you have a total of $3 billion in free cash flows if the coming 4 years look like 2018 or the first part of 2019. Graftech’s market capitalization is currently $3.7 billion, so you are practically getting whatever the company does on top of the contracts from now to eternity for $700 million. Which is what the company is making now per year. Thus, if after 2023, the company is still equally profitable as today, this is a typical Pabrai ‘PE ratio of 1’ company.

However, the contracts will lead to only $4.5 billion in revenue, that is enough to cover for 2, 2.5 years of business at these levels. Electrode prices are still high, so the company might get to new contracts. In the last conference call, the management said fall is the period when they negotiate contracts. We will see what will the customers decide, buy Graftech’s or wait for supply from China.

The locked in, contractual cash flows are what provides a relative margin of safety. However, only about 60% of the cash flows will be distributed to shareholders, mostly through buybacks. There is $2 billion in debt that the company intends to pay down by quarterly instalments of around $125 million.

Source: Graftech Q2 Results

As Brookfield is the owner of the company and also the owner of the $2 billion in debt, they might be creative in the ways they take the money out of Graftech. There was a $750 million dividend in the form of a promissory note to Brookfield where the company didn’t have the money to pay the dividend, but issued a note in order to pay it later. I know such things are normal when it comes to this type of ownership structures, but still something I would not like as a small shareholder. You are simply not, and will never be, equal. Apart from Brookfield’s intentions, that also sold stocks directly to Graftech for $19 in August 2018, the main question is how will the steel market evolve.

The main question with Graftech – EAF steelmaking

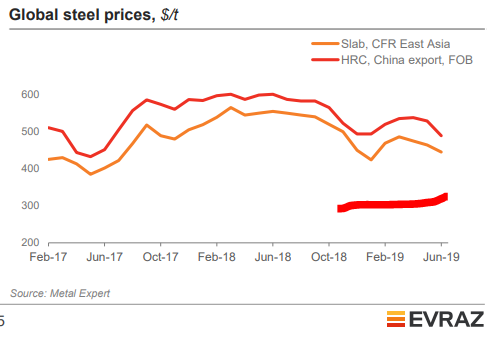

The main question is the long-term outlook for the company. As the main product is steel, electrode prices will depend on steel prices and demand for it, especially for EAF steelmaking. Steel prices have softened a bit over the last year, and if we have an economic slowdown in China, prices will fall more.

Source: Evraz Q2 Investor presentation

As investors usually predict 5 out of the coming 2 recessions, stock prices tank, sometimes for no fundamental reason at all. The same might be happening to EAF, fear of lower steel prices and lower demand for electrodes is what has pushed the stock down, even if the market remains strong.

However, if there is a decline in demand for steel, graphite electrode prices can easily tank as it was the case up to 2016, when prices fell to approximately $2,500 per MT.

Source: Graftech IPO S-1

On the other hand, if the EAF steel sector remains positive, there will be a nice future for Graftech. If China goes from 9% to 20% EAF steel production, demand for electrodes will remain high, no matter what happens in the environment.

Source: Graftech

Petroleum coke, necessary to make electrodes, is also used when making the graphite electrodes (anodes) in the EV industry. This increases prices of the prime input material and consequently also of electrodes. Graftech is hedged against such increases as the 100% owned subsidiary Seadrift Coke, produces the necessary material.

Source: Graftech

China will try to produce the necessary needle coke by using coal, but the quality might not be sufficient to jeopardize Graftech position. If all the projected needle coke plants come online as expected, prices might be much lower. This is typical for a cyclical industry.

Source: Steel Mint

The above are the short-term concerns. Combine such possible supply threats with Graftech’s debt, and things might get ugly. We know that Brookfield wants to get out, so that is another negative. They might be window-dressing this just to get out as soon as possible.

The question is whether the company will survive a negative period, be it a short one due to the high level of debt. That part is a bit too risky for me. To explain; electrode prices can easily fall, which means there will be no more room for take or pay contracts. Consequently, margins could fall significantly and profits too. That will be the time to buy because over the long-term, things look good.

Long-term outlook for Graftech international

If the world continues to develop as expected, the amount of steel that still needs to be produced is staggering. As the world continues to develop, you will need more and more steel. Growth might be slowing down, but 3% global growth today, requires much more steel than 6% global growth 20 year ago because the current consumption is more than double what it was.

Source: SIA

Graftech Stock Valuation

I think there is a big chance for Graftech to become a PE ratio of 1 company and I believe Pabrai is buying because of the margin of safety in the form of the short-term take or pay contracts and because of the exposure to future growth in Asia, especially India.

All you need is another commodity boom over the next 10 years and you quintuple your money. Therefore, from a risk reward perspective, I would say there is a 15% chance of a total loss over 5 years, a 15% chance for a 50% loss, a 40% chance for a double, 20% for a triple and 10% for a quintuple.

The actual risk reward value for the stock is $25, not a bad bet.

On a personal note, I prefer businesses where there is practically no downside and similar upside.