Flex LNG Stock Analysis – The Big Bet On The LNG Boom

Flex LNG stock price analysis and earnings model

Do you want to invest alongside the Norwegian billionaire John Fredrisken? He is betting big on a revival in shipping and he has been in the industry for 5 decades now and made a lot of money in the process.

Prefer watching? Enjoy the video, article continues below.

The owner of Flex LNG (FLNG) is Geveran trading – indirectly controlled by trusts established by billionaire John Fredriksen for the benefit of his family. He also owns Golar LNG (GLNG), Seadrill (NYSE: SDRL) – offshore drilling, Marine Harwest ASA (OSE: MOWI) – salmon, Golden Ocean Group (GOGL) – dry bulk and Frontline (FRO) – tankers .

To quote him, this is what investing in tankers really is: “Fredriksen pockets $1 million a day in dividends from his 23 percent stake in the company. He says he finds oil drilling dull compared with tankers, where you can earn back a year’s losses in the space of a week. “I’ve been in tankers for 50 years, and I like it,” he says. “For me, it’s still fun.””

So, we have to keep in mind volatility before investing and also diversification. As you have seen above, he is always diversified. Let’s look at the LNG sector and then at the company.

The LNG shipping sector

We all know the story; natural gas is the fossil fuel of the future as more environmental and cheaper. The best way to distribute it across the world is by LNG. LNG production is consequently ramping up and this should lead to higher demand for ships.

Source: Flex Lng

Expectations are that there will be more and more LNG coming into the market creating a positive tailwind for the shipping sector. I always prefer to invest into sectors that offer positive tailwinds. If things don’t go as planned, you don’t lose much as there will always be positive periods that can save you. If things go as planned, you do very well.

Flex LNG company overview

The following video gives a good overview of what is going on in the LNG sector and about the company, I urge you to watch it, it is just 3 minutes long.

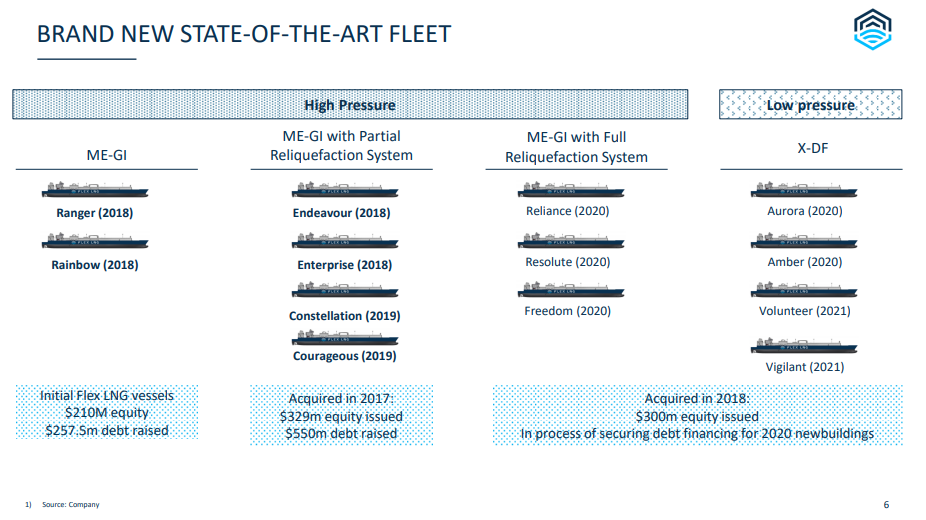

Flex LNG is LNG shipping company with a fleet of next generation LNG carriers with large cargo capacity. The fleet consists of thirteen modern LNG ships, five existing and eight under construction for delivery throughout 2019-2021. All LNG carriers are equipped with slow speed, two-stroke engines MEGI or X-DF propulsion which will provide Charterers with state-of-the-art tonnage offering significant advantages in form of reduced fuel consumption and lowered boil off rates.

Newer ships mean less fuel costs and give an advantage over older ships.

Source: FLEX LNG

For now, the company has 5 operating ships and 8 are being built.

Source: FLEX LNG

The plan is that the newer ships will get better shipping rates and be profitable for the long-term.

Source: FLEX LNG

When it comes to owning ships, it is all abut the shipping rates you can get. Shipping rates are always volatile, depending on season and on demand for ships.

Source: SP Global

In Q2 2019, FLNG achieved rates of just $46,266 per day, that is not great, but not bad even. It is a break-even level for the company. However, the above shows how rates are always volatile and we have to go for the average to make financial calculations.

Source: Flex LNG

Let’s look at the fundamentals before using the above rate data to make an earnings model.

Flex LNG stock fundamentals

We have 5 boats in operation and 8 being built. Building ships should mean cash flows are deeply negative, alongside lots of debt and financing necessary to build the new boats.

Source: Flex LNG

They still have $670 million to pay for their new boats, they have already paid $349 million, which is not little money. They recently did a sale and charter-back transaction with Hyundai Glovis where two vessels have been sold for $420 million with a net consideration of $300m to the company adjusted for a non-amortizing and non-interest bearing seller’s credit of $120m in total. This confirms the value of the ships and perhaps there will be more possibilities to do the same financing deals in the future, to improve the balance sheet.

Source: Flex LNG

Equity is high, it is in the form of money used to finance the ships that are being build, also created with equity financing where the owners added $300 million for 31% of the company in October 2018 at a valuation of $900 million. The current valuation is $520 million so you are getting the ships at a nice discount.

Source: Flex LNG

The cash flows are nothing stellar as rates are at breakeven levels so we shouldn’t even expect anything more at the moment.

The financing is relatively cheap which is good and the company will likely not have trouble to finance the completion of the boats. Interest rates are around 6% which is not much for shipping.

Flex LNG stock price analysis and earnings model

Recent US listing (NYSE: FLNG)

They recently listed on the NYSE under the ticker FLNG but this is not a new company, it has been listed in Norway for a while now. They were created as a smaller company that is focused on growth, to take advantage of the possible LNG boom.

As already mentioned, they also did a private placement for $300 million, that is significant on the current market cap of $600 million.

When it comes to earnings, it all depends on spot rates and whether they will lock long-term contracts when those spot prices are higher. They assume a cash breakeven level of $50,000 per day which means that if rates are higher, profits will also be higher.

Source: Flex LNG

I have no idea where will rates go in the future and when. In 2018 rates went above $200,000 for a short period of time, but that wasn’t sustainable.

Rates really depend on demand, how hot will the summer in Asia be (airco) and how cold will the winter be (heating).

We also have a fleet oversupply at the moment but growth in LNG demand should cover for that in the future. So, if prices are around $40,000 with oversupply, those will probably be much higher when the supply of vessels is not enough.

Source: Bloomberg

The trend remains positive with higher demand expected from China.

Further, one year charter rates are already at $85,000, which means the company could make around $12 million per vessel in cash flow. This would lead to free cash flows of above $150 million.

I somehow feel that if they break even at $50,000 with the newest ships and good financing, the competition can’t do better. Therefore, it is unlikely that prices remain below $50,000 for longer. At an average of $75k, each vessel would make $9 million in free cash flows. This would lead to free cash flows of $117 million on the 13 ships in operation. Not bad on a $600 million market cap. If prices spike in a year, and go above $200,000, FLNG could earn its current market cap in one year. The stock price would probably increase 10 times too in the process. This summarizes what investing in shipping means. But there are also risks.

FLEX LNG investing risks

For a summary of risks, all well explained in the Annual report.

The covenants on the debt explain the risk when it comes to investing in shipping. If those covenants are breached, ship values drop, the company has to put up more money and there simply isn’t any (if there was money, the covenants would not be breached).

Source: FLEX LNG Annual Report

This is the house of cards for most shipping companies. Keep in mind the risks but also the upside and read the story of the owner and his investing style in a nice Washington Post article.

On the other hand, in good times you make money, to quote: “Thanks to his practice of awarding fat dividends from his companies when profits were soaring, he had won the confidence of investors who might otherwise steer clear of the battered tanker industry. In May, he raised $210 million in equity for Frontline 2012”. (BTW, Frontline didn’t work out when oil prices collapsed).

Investment thesis on FLEX LNG

Spot rates will remain volatile depending on short term LNG shipping prices – depending on short term LNG demand and supply (mild or cold winter in Asia).

The company is a low-cost provider thanks to new ships with modern engines.

The key is to look at spot prices, if those really spike, this will be a big winner.

On the other hand, you never know what will the market look like and a longer period of lower spot rates, might turn this into an ugly story.

Therefore, if you fancy the risk reward, as it is positive, you might dip your toe, but keep in mind portfolio exposure. If LNG rates spike, you will do great. On the other hand, if it doesn’t go well, your maximum loss can be 100%. However, be careful that the 100% doesn’t become bigger and bigger if you add too much money to it.

The thesis here is that spot prices will spike in the future and that is when the company might switch to longer term contracts. This might lead or to vessel sales or dividends.

I will keep watching the stock and who knows…

The opinions expressed – imperfect and often subject to change – are not intended nor should be taken as advice or guidance. The Sven Carlin Stock Market Research Platform is not an investment advisor or financial advisor. The Sven Carlin Stock Market Research Platform provides research, it does not advise. The information enclosed in this article is deemed to be accurate and reliable, but is not guaranteed by the author.