Fastned Stock Analysis – Another EV Related Bet

I remember seeing the first Fastned charging points over the country a few years ago already. I was always looking and thinking how empty those were. However, that was a few years ago as I moved out from the Netherlands in 2019, so let’s see how Fastned has been evolving and whether there is an investment opportunity there or it remains a pure bet where many things have to fall into place for current investors to make any kind of long-term return.

This Fastned stock analysis (AMS: FAST) is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential with a margin of safety, so as would Buffett say; I start with the As. At the end I need to find only a handful and I’ll do great over my investing life.

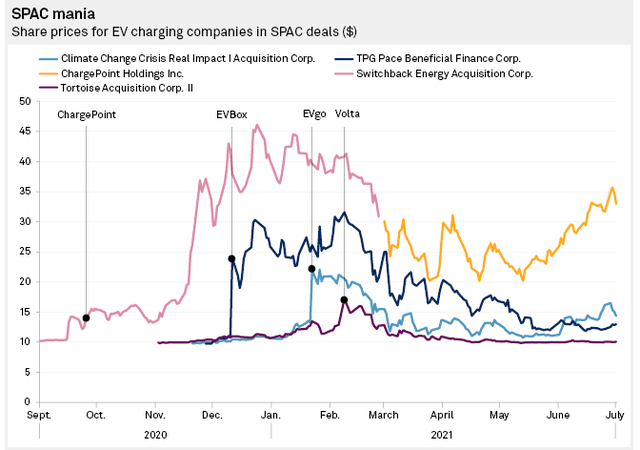

Fastned stock price overview – AMS: FAST

Fastned went public in 2019 at 10 EUR per share. It has been trading flat up to the EV charging craze that has hit the market.

The SPAC mania did subdue a bit as EV charging companies are far from showing any kind of profitability or sustainable competitive advantages, but in a world with an abundance of free money, there are more and more bets to be made. This will end ugly for most investors – there – I have warned you!

Let’s see if there is value with Fastned stock.

Fastned stock analysis – Business Overview

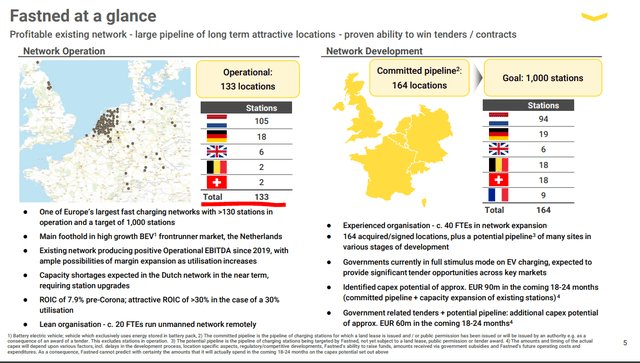

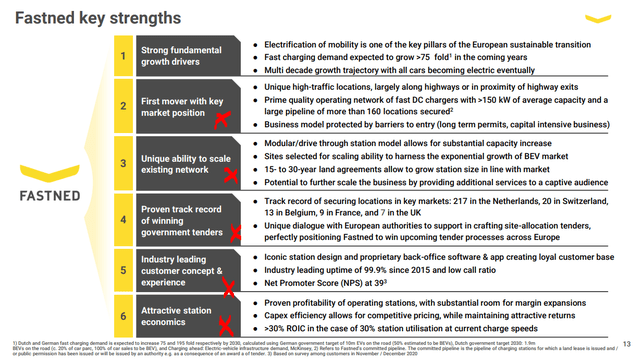

Fastned has 133 locations and another 164 in the pipeline where their goals is to reach 1,000 stations.

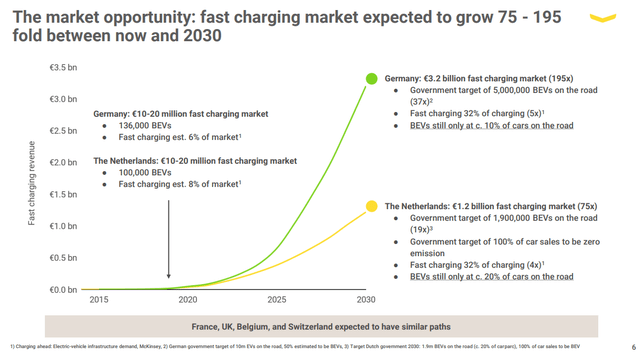

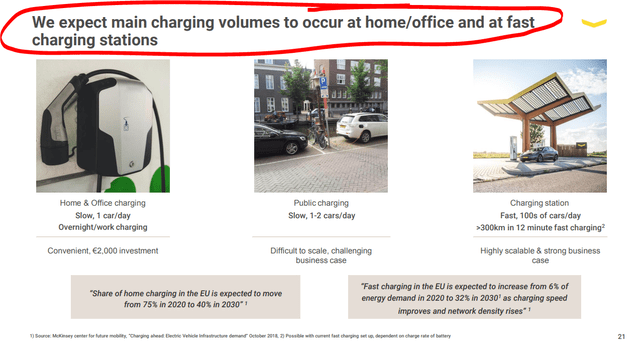

The business model is based on a boom in EV sales and charging requirements.

Let’s immediately dismantle the business model.

2) There is no moat in the business, anyone can set up charging stations and especially utilities. 3) Anyone can do it 4) just means you paid most, but competition can be fierce, plus there might be free charging points with solar to attract cusomers to IKEA, like the $1 breakfast

5) customer experience? For charging???

6) The price and economics depend on the competition which you are on the mercy of.

Time will tell what will be, maybe we will have a winner but it is also possible nobody will ever make money in the sector. So, millions are invested on an expectation.

I reiterate myself, anything can happen, but we value investors don’t look for bets.

Fastned stock analysis – financials

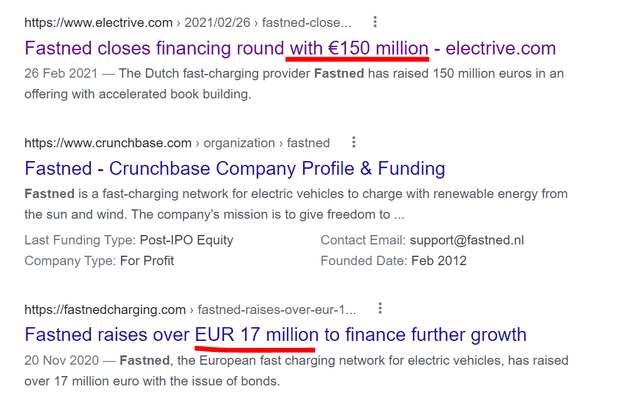

When a company is losing money and needs even more money to invest and grow, you can be sure only of dilution.

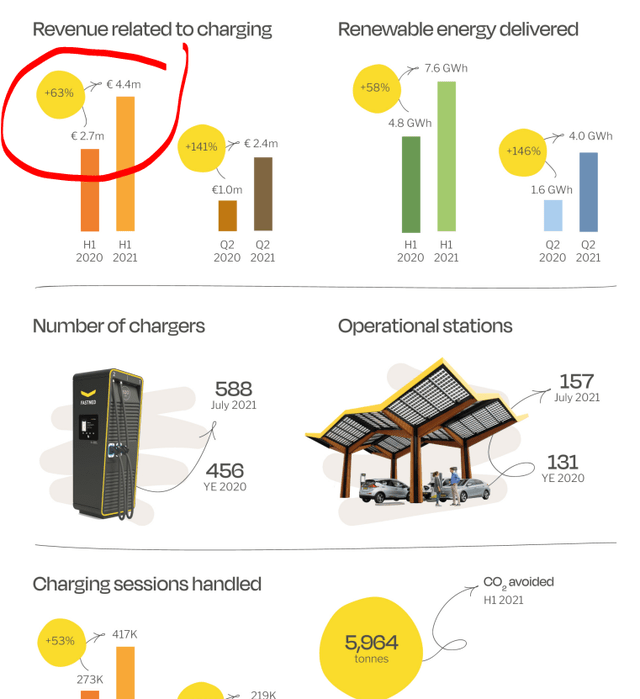

Plus, they might be reaching revenues of 10 million for 2021. This is a price to sales ratio of 100 on the current market cap of 1 billion EUR.

They lost 15 million EUR to sell 4.4 million! No need to dig deeper here. They also have 80 million of loans and the key important factor here is the ability the company will have to constantly attract new money (depends also on the stock price and exuberance related).

I personally prefer companies that make money.