DSM Stock Analysis – A Valuation Question

I follow cycling and there is a DSM team, but I never cared nor knew about what DSM does, so perhaps they should save a few millions per year by not advertising in that environment. On top of that, their team didn’t do much this year – second last of the world tour teams. Anyway, let’s see what this is about, the stock is doing better than the cycling team for sure.

This DSM stock analysis is part of my full analysis of all the businesses listed on the Amsterdam Stock Exchange. You can find the full list here: Amsterdam Stock Exchange All Stocks List and Analysis.

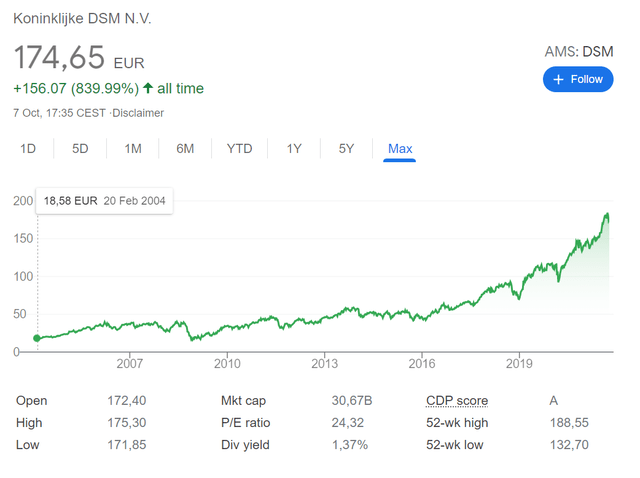

DSM Stock Price Overview

A stock that goes only up over a long time usually represents a good business, one that grows, compounds and is a good capital allocator with good returns on capital. Those that invested almost 20 years ago have been rewarded with a really good returns, almost a 10x.

The market cap is still not that high, at 30 billion EUR, so there is room for more growth. Let’s see if DSM stock can make another 10x from current levels and thus become a 100x over time – 100 baggers discussed here.

DSM Stock Analysis – Business Overview

DSM is a science company producing special ingredients for food like vitamins and other special materials like engineering plastics and resins.

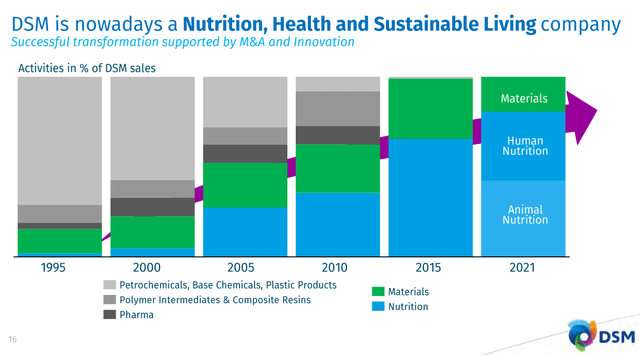

It is important to not that 10 years ago DSM was a pure chemical company producing low margin commodity products and evolved into a higher margin specialty ingredients and materials company.

DSM’s transition over time

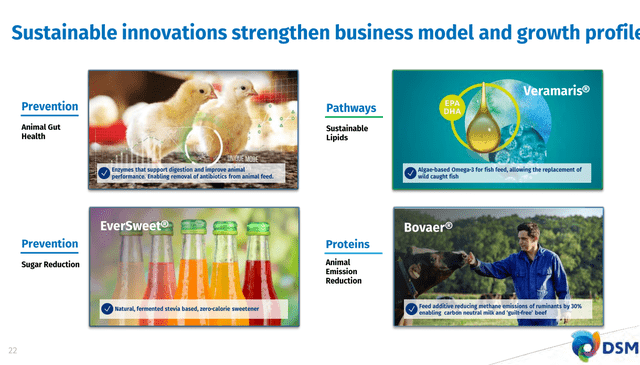

Nutrition is the core business of the company now.

DSM nutrition overview – Source: 2020 Results presentation

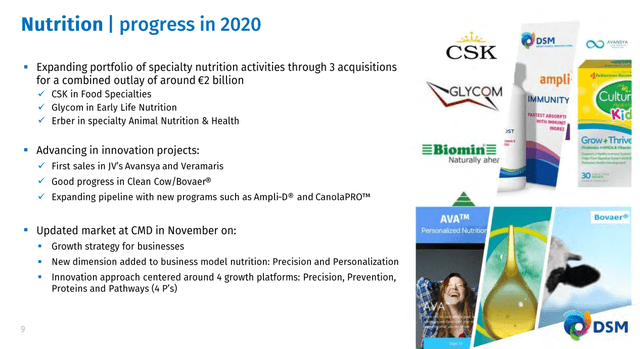

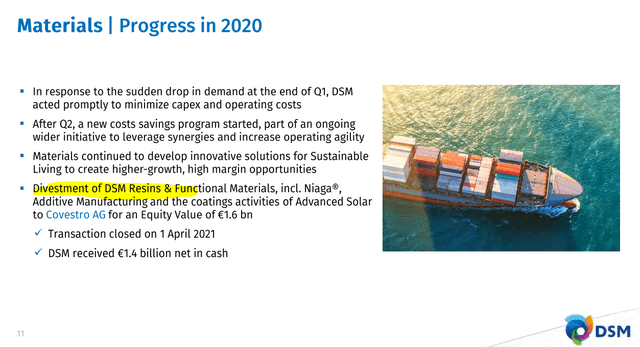

DSM has been doing a lot of acquisitions but also divestments. The market usually really likes when a company sells a low margin business to acquire higher margin, faster growth businesses. This is because growth and higher profit promises is what is easiest to sell to the market, cyclical commodities are regarded as ugly. DSM has been doing a stellar job over the past 10 years to move itself from an ugly commodity business to a stellar human innovative nutrition company.

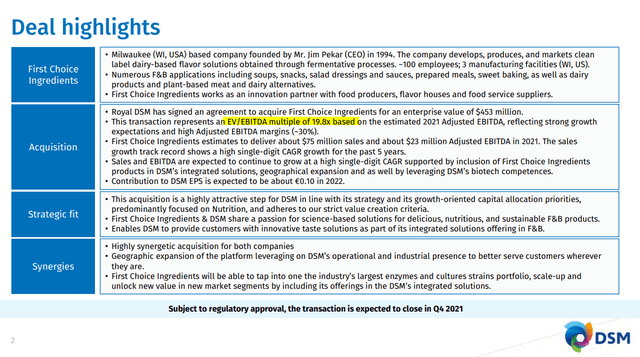

However, at some point, the strategy applied cannot be of equal value. The first acquisitions done in 2010 were at rock bottom prices, but now the recent First Choice acquisition has been made at 20 times EBITDA.

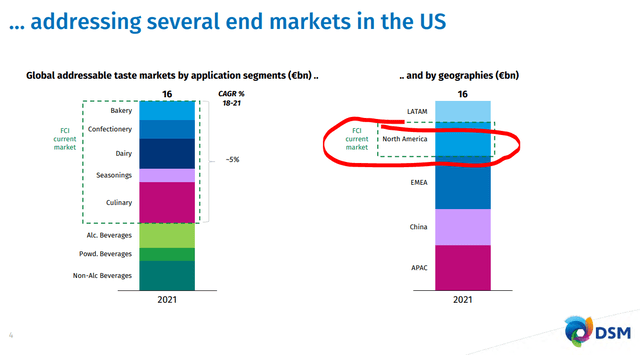

It might be expensive, but if they can scale their products globally through their network, it might be cheap for them.

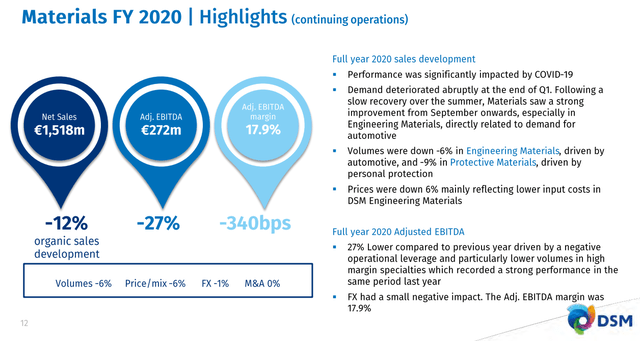

Materials is a smaller part of the business as the focus is on nutrition.

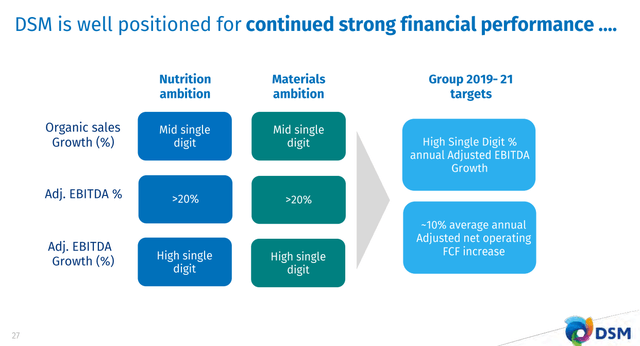

They plan to grow sales around 5% and grow EBITDA too as they sell the low margin businesses and focus on more specialty businesses. If they can further scale on the acquisitions, the future should be good for DSM. But a good future doesn’t mean it is already a good investments, if all depends on valuation.

DSM stock financials

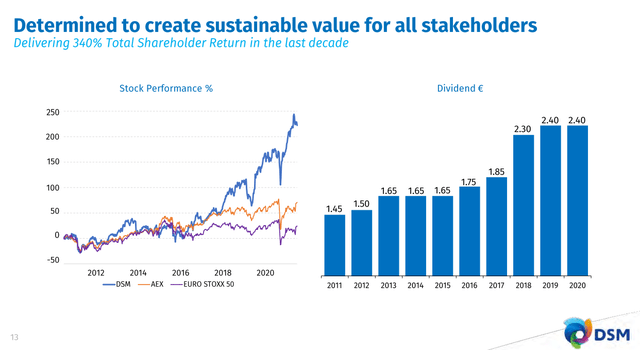

It all sounds great, the stock has outperformed all benchmarks but, the dividend has not even doubled over the past two years while the stock is a 5x since 2011.

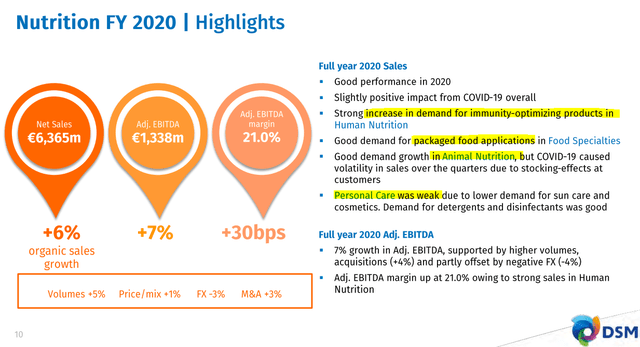

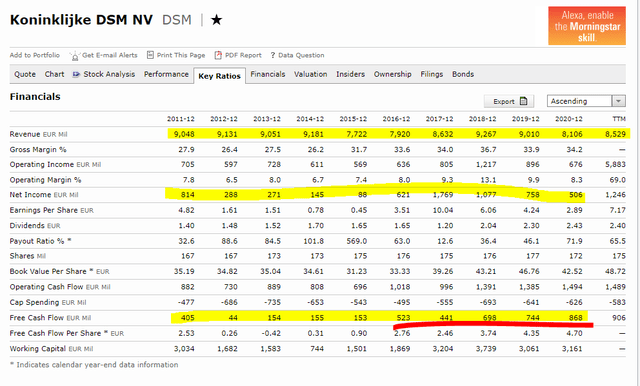

As they divest and acquire, revenues have been pretty stable over the last decade. However what has changed are margins and especially cash flows. The FCF went from an average of around 200 million in the early 2010s to the current average of around 900 million EUR.

From a fundamental perspective it all looks good, but let’s see from an investment perspective.

DSM Stock Valuation

They have doubled FCF over the years, but still, at a market capitalization of 30 billion, FCF of less than 1 billion, even at planned growth of 10%, it will take 15 years to get to 4 billion and a 15% business return from the current business. That is not bad, and the stock will likely follow the growth, but too much risk for me on a high valuation.

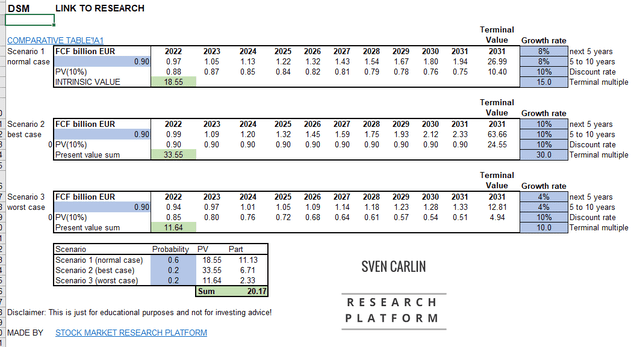

I have taken the 0.9 billion EUR if FCF as a valuation start. If we assume 8% FCF growth which is what the management projects, a discount rate of 10% which is my comparative rate of return and a terminal multiple of 15 ten years from now, I get to a fair value of 18.55 billion EUR which is much lower than the current 30 billion.

If I am more exuberant, put 10% growth in each year over the next 10 years and a terminal multiple that doesn’t contract over the next 10 years and remains as is now, I get to a similar valuation to the current market cap.

DSM Stock Valuation – Source: Sven Carlin Research Platform (free valuation template download)

So, for me DSM stock is a good business for sure, just valuation is what makes the investment risky. Even if the management succeeds and delivers on targets, without hiccups over the next 10 years, just a change in market sentiment where the valuation falls to normal historical levels of 15, would see DSM as overvalued now but a margin of 66%.

DSM stock might be fairly valued in the current environment but not for me – too expensive thus too risky – I’ll keep looking for a business that looks like DSM looked in 2010, ugly and cheap, that is where the best investments are found.