Devro Stock Analysis – Pension Deficits Might Make This An Ugly Investment

Devro Stock Analysis

Devro plc is a multinational company with registered office in Moodiesburn, Chryston, United Kingdom which manufactures and distributes goods derived from collagen, principally sausage casings, a product in which it is the world leader.

In my FTSE 250 small cap research I discussed how the company had big pension deficits that present a big investing risk. However, as we came across Devro stock twice already, it is worth a deeper look.

Devro Stock Analysis – Financials

If we take a look at Devro’s financials, revenue has been stable over the past 10 years, operating margins have been volatile but quickly recovered from 2014. Dividends have been stable and doubled but the pay-out ratio went from very low to very high. The number of shares remained stable and the free cash flow is where it was. Also, book value per share didn’t change much. With such a boring stock, it boils down to valuation and outlook, will there be something that will make the situation different over the next 10 years? For that, we need to check their story and Devro’s investor presentation.

The last interim earnings report shows how the company is still stable but we have to see about the new strategic plans. When it comes to such small companies, they have the know-how so you never know when can it do some good. (the company did grow 19% in China lately)

And, China is a key growth market for Devro.

There is market weakness and high competition in Europe, but the company is growing fast in the US (10%) and in China (19%). They expect to grow in H2 2019 and what is also important is the dividend of 5.3%.

The stock probably didn’t deliver on expectations since 2013, there has also been the whole Brexit mumbo-jumbo, so it is cheap value now. The forward price to earnings ratio is 9.91 which makes it a value stock.

Devro stock analysis – pension deficits

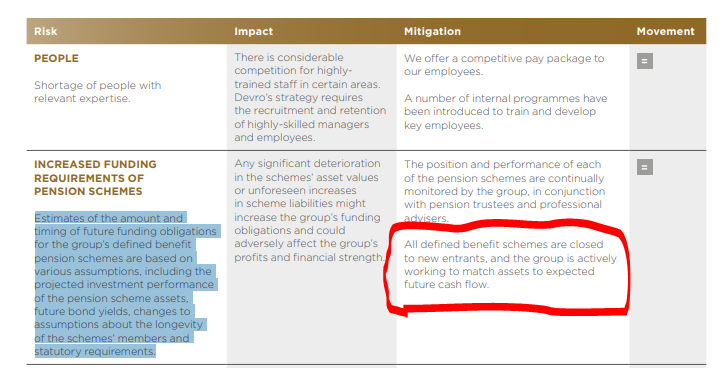

The pension deficit is 60 million pounds and growing. Given the current situation in the markets, it could easily grow even more very fast.

The pension obligations are on the balance sheet (those were also 82 million in 2017) but are not included in the earnings calculation (only in the comprehensive earnings calculation). So, the earnings are not so high as the company is showing them to be after we account for the possible pension risks. In 2017 there was a 32 million pension gain due to updated assumptions. I must say I don’t like actuarial assumptions because if those are completely wrong, the company could be in big trouble.

Fortunately, defined pension benefit schemes are now closed to new entrants as companies have learned that they cannot guarantee future payments. If we dig deeper, we can se that the decline in pension liabiltities was just thanks to a change in the assumptions, probably the discount rate.

This can be better understood by looking at what assumptions go into such a calculation. The company is monitoring the situation but is it like monitoring the weather now to see what will be the weather in 6 months.

They simply increased discount rates significantly and lowered pension obligations. If the actuary doing the calculations in 2020 wants to get hired again, he’ll better increase the discount rate again.

Now, if interest rates go up, the fair value of bonds should go down. If not, interest rates have actually gone down! With Devro, the discount rate they use on their obligations went up so the obligations went down but the value of their bonds went up, which means their interest rates went down.

That is a heck of an actuary doing those calculations, practically a magician.

The key risk here are interest rates, if those go up, bond values will go down, diversified growth funds values will go down and stocks too. So, you can find yourself within a 100 million hole very quickly. A risk I really don’t like.

I’ll try to ask the manager of the fund what is his opinion on this holding. However, Devro is not even close to top 10, so perhaps they bought it during the 2009 bottom when it was real value.

Definitely not something for me, plus the company has no moat and the whole food sector, thanks to the internet, private labels etc. is a sector where competition is increasing.

If you wish to learn more about how to analyze stocks, check my FREE Stock Market Investing Course.