Daimler’s stock crash analysis and investment thesis

Daimler’s stock is down 25% from its 2018 peak.

It is crucial to take a long term cyclic perspective on the company.

Daimler can be a good investment but you have to apply the right strategy.

Daimler’s stock (Xetra: DAI, OTCPK: DDAIF) is 25% below its 2018 peak. The last blow came from their guidance cut based on import tariffs for US vehicles into the Chinese market.

This is an excellent opportunity for me to discuss how I approach investing in a company like Daimler. We all know it is a cyclical, it can also be affected by internal shocks, like recalls and external shocks, like tariffs. In that light, one must have a long-term orientation when analyzing a company like Daimler.

To quote Seth Klarman:

“The single greatest edge an investor can have is a long-term orientation”.

The long-term orientation analysis method

In this article and video, I describe the long-term perspective I use when analyzing a company like Daimler.

Here is the video, written article follows below:

The key is to focus on long-term earnings trends, where by long term I consider at least a 10-year period. A long-term focus allows us to take advantage of short-term fluctuations.

Here is Daimler’s stock chart from 1996 till the end of 2017.

Figure 1 Daimler’s stock can be described as very volatile

Source: Modern Value Investing

What is clear from the above is that Daimler’s stock has been hit hard during every recession, where peak to bottom declines are in the range of 70% (2002 & 2009). Smaller shocks also negatively affect the stock; there was a 40% peak to bottom decline in 2015 due to the Chinese recession scare and a similar decline in 2012 due to the European crisis.

The above, leads me to believe that one has to take into account possible known and unknown shocks when looking for Daimler’s intrinsic value. Given the price target ranges for Daimler, from €55 to €90, I assume few analysts do that. Let me explain what I mean by showing you a few earnings models for the company. Before that, just a funny anecdote which shows exactly how important is to take a long term, cyclic perspective, on modeling earnings estimates and consequently, calculating intrinsic value.

In December of 2017 I picked Daimler as the company to analyze and apply the 25 tools discussed in the book I was writing, Modern Value Investing. I chose Daimler because of its largeness and long history, that gave me enough material to apply all the tools. However, I took a big risk as the price at the time of writing was €77.5 while my intrinsic value estimations were closer to €50. Fortunately for me, and unfortunately for Daimler shareholders, the stock price quickly declined closer to my estimated fair values.

Going from a linear towards a cyclic earnings model

A net present value calculation of future cash flows is essential for valuing a stock. That is what I did with Daimler. I started by taking a linear perspective and continued by adding shocks in the form of recessions.

Note on the earnings model: I usually estimate 10-year earnings and apply a 10% discount rate which is my minimal required rate of return. I don’t add a final value to keep things simple, but feel free to play around with that.

Figure 2 Daimler’s NPV without a recession and without a final value to avoid complexity

The 1.5% growth rate is derived from McKinsey’s expectations for global automotive industry growth.

Linearity is a trap many fall into when analyzing a company. To show how shocks can affect Daimler, then next table offers an earnings model with a recession in 2020 where earnings turn negative and are halved in the years prior and post the recession. The earnings loss in the recession year is my estimation based on Daimler’s losses during the last recession (2009) in relation to their previous profits (2007 & 2008).

Figure 3 Daimler’s NPV with one recession in 2020 and consequent stable growth

Just one recession lowers Daimler’s value by 25%.

By adding a second recession to my earnings model, Daimler’s stock value falls another 20%.

Figure 4 Daimler’s earnings model with two recessions, one in 2020 and one in 2026

As the most likely scenario is that we will have at least one recession in the next 10 years, I have calculated an intrinsic value for Daimler of €50 for those who want a long term of 10% return on their investments.

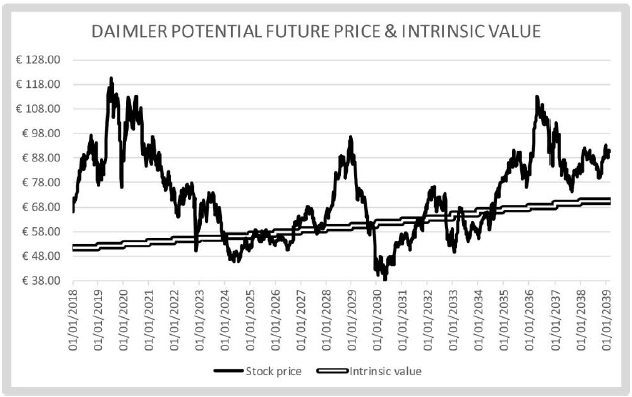

Taking advantage of the market’s long-term volatility

The €50 intrinsic value seemed very conservative back in December of 2017. Now, it looks like a prescient prediction. Nevertheless, to show how one should always wait for better entry points when it comes to cyclical stocks like Daimler, I have plotted the past 20-year stock price movements onto my intrinsic value estimation with a 1.5% book value future growth rate. The start of the past price line is at €77.5 which was the price back in December of 2017. If things resemble what has happened in the last 20 year, one should have the opportunity to buy Daimler with a significant discount to intrinsic value and sell the stock when it is clearly overvalued in euphoric economic times.

Figure 5 Plotting Daimler’s historic price volatility to an estimated future intrinsic value

Source: Modern Value Investing

With the latest trade war news and Daimler lowering its guidance, the first opportunities to buy the stock at intrinsic value might be around the corner.

Waiting for a margin of safety

Intrinsic values are not all there is. Value investing, where you apply a margin of safety, goes beyond investing in a stock when it is only fairly valued. You want to invest in something at a discount to fair value. Fortunately, as the above figure shows, there probably will be opportunities to invest in Daimler at a discount, because the stock price is never still.

How big of a margin of safety should you wish for depends on you, your risk reward appetite and other investment opportunities. As I do a lot of research, my minimum margin of safety is 40%. Thus, my entry point with Daimler would be €30. This seems low, but at peak pessimism, during the next recession, we might see such a price. Especially if the stock remains at levels around €55.

The following table summarizes my conservative estimations about Daimler’s intrinsic value from December 2017.

Figure 6 Summary of the 25 tools described in the Modern Value Investing book

Source: Modern Value Investing

Conclusion

I believe Daimler is a company that will be there in the next few decades. It has always been at the forefront of new technological developments, it has a strong brand, and is exposed to a global growth trend – the automotive industry.

Therefore, one could easily invest in Daimler when the price satisfies one’s long term expected return from stocks. But keep in mind, this is a cyclical and better investing opportunities might be around the corner in the form of lower entry points. Therefore, adjust your exposure accordingly.

My message is to be patient and take advantage of the volatility that is and will always there. If you find good companies to follow, a dozen of them. You will get to know them well over time and you will know when one of those is a buy. You don’t need to do anything else when it comes to investing.