Core Laboratories CLB Stock Analysis – Bet On Oil

This Core Laboratories Stock Analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As. Here are the Cs already.

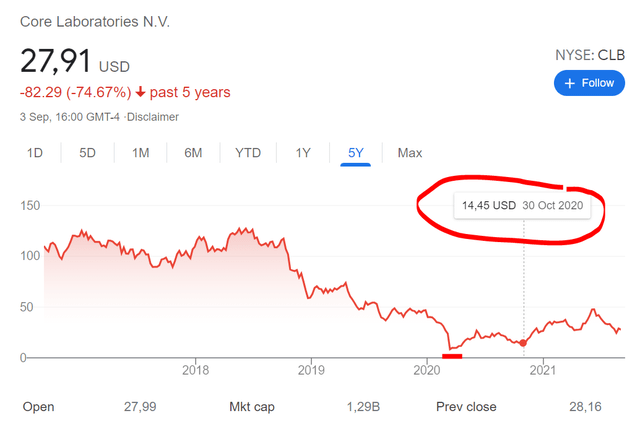

Core Laboratories Stock Price Overview

Core Laboratories stock is trading both on NYSE:CLB and on Euronext Amsterdam: CLB. CLB stock did really well up to 2014 since when the stock has tumbled 90%. To see such a stock price drop these days is rare but let’s take a look as when it comes to turning stones, sorry stocks, you never know under which stone you’ll find the gem that is going to keep giving forever.

I’ll first share a business overview alongside a discussion on how the oil sector outlook might impact CLB stock, cover the fundamental risks and conclude with what would be a low risk/high reward level for investing into the stock.

Core Laboratories Business Overview

Core Laboratories N.V. is an American service provider of core and fluid analysis in the petroleum industry headquartered in Amsterdam. Core Laboratories core business is reservoir rock description where the company analyzes all the kinds of rocks and fluids in an oil reservoir to enhance extraction and profitability for the operating company.

CLB Stock Analysis – Business Overview – Source: CLB 2020 Annual Report

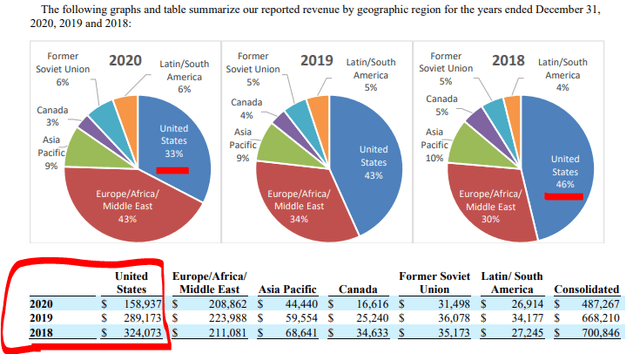

The business perfectly explains the above CLB stock chart as the stock boomed following oil prices and the shale boom, just to consequently crash as oil prices fell below $100 and as most big oil companies turned towards investing more into renewables by lowering their investments in new reservoirs. Less oil capex also means less business for Core Laboratories. Also, a mostly US focus pushed its revenues down given shale oil investments have been declining.

Total second quarter 2021 revenue was $118,700,000, of which $40,500,000 for production enhancements and $78,300,000 for reservoir description (this doesn’t add up but that might be due to rounding – source: Core Laboratories Q2 2021 results). Given that 100% of revenues are derived from such a specific field, the whole business thus depends on new oil fields being developed. For now, it looks like there is underinvestment in the oil field but one must also keep in mind it is very cyclical and likely to slowly and steadily decline over long-term. Something strongly reflected in CLB’s stock price chart over the last 7 years.

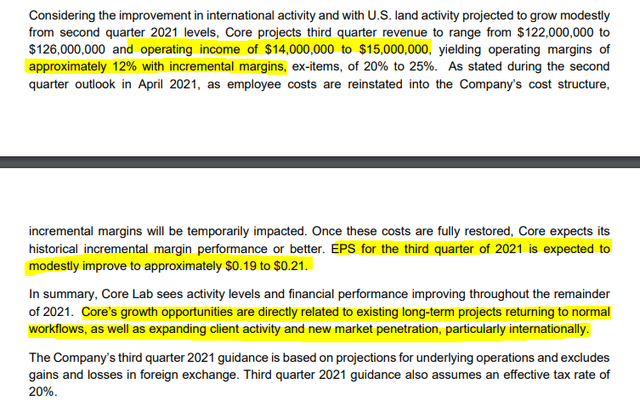

On guidance, there is not much to expect except stagnation. Maybe if oil markets recover, Core will do well, but that is a long shot even if it is unlikely we will see declining demand for oil in the coming years.

My outlook for oil is a bit more positive than consensus because I see electric vehicles adoption being slower than expected, especially in emerging markets where those could actually increase demand for oil. On the other hand, oil investments in western markets are lower and will likely remain lower given the sentiment, and that doesn’t bode well for Core Laboratories. For those interested in my oil outlook, here is my latest update:

Let’s look at the finances to see if there might be any value left that would give a margin of safety while waiting for a possible oil return to glory.

Core Laboratories Stock Analysis – Fundamentals

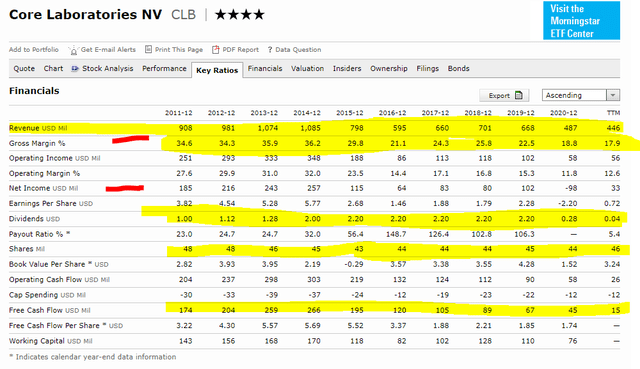

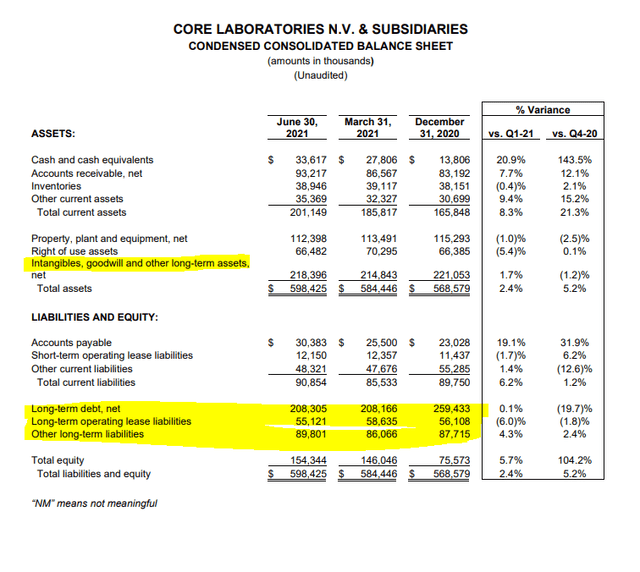

Revenues have declined more than 50% from the high oil price peak of 2014, margins have contracted, and the company went from making more than $200 million per year to making around $50.

$50 million per year in a bad environment is not even that bad, however we must check debt levels too. The balance sheet doesn’t look great.

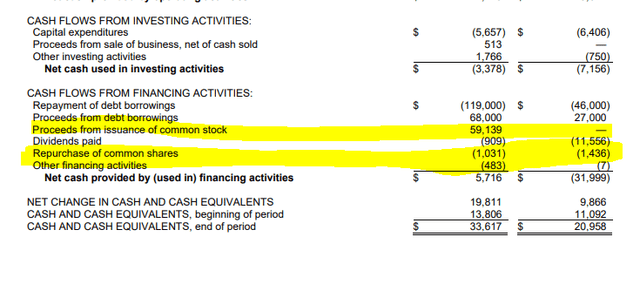

A company making approximately $50 million per year having more than $300 million in debt is a risky business. I see they have been lowering debt by issuing equity which means if there are new oil market issues, it will be again difficult to finance operations.

To survive the 2020 crisis the company had to issue shares to survive and now they are already doing buybacks to try to push. Given the money spend on buybacks, it seems those are just of cosmetical nature.

Core Laboratories Stock Analysis – Investment Thesis

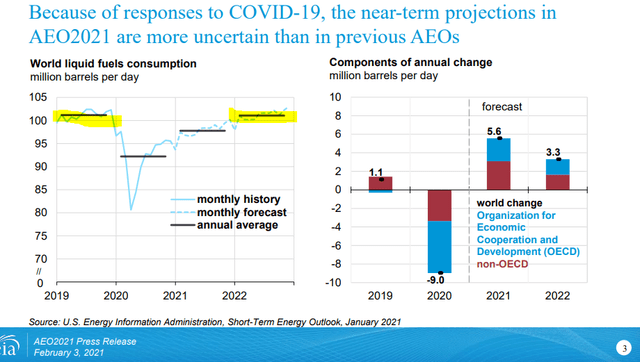

I feel CLB stock could do really well on a slower than expected decline in demand for oil compared to what the market is currently pricing in. By 2022 we should see oil demand in line with 2019 according to EIA.

The outlook beyond 2022 will mostly depend on how fast the world switches to alternative fuel sources and how fast emerging markets demand for oil grows. However, that is a global oil market we are talking about, and Core is mostly focused on the US which means it has to compete globally now.

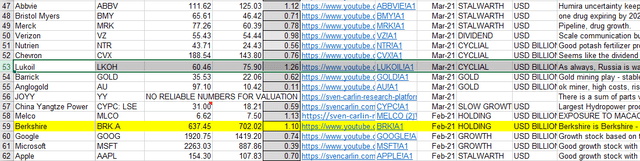

In a positive scenario, Core could improve margins and grow revenues for a while, but given the debt, this can also turn ugly, as we have seen in 2020 with the share issue. Therefore, this is not something I am interested in as I am a low risk investor. For those who look for higher risk bets, one might consider CLB stock. But then again, even if they make $100 or $150 million in a year, that would still be a FCF yield of around 10% which is relatively low from a global oil perspective. If I compare CLB stock with Lukoil, where the core investment driver is the price of oil too, Lukoil is simply much cheaper and has a better outlook.

Core Laboratories stock comparison – Source: Sven Carlin Intrinsic Value Template (free download)

To conclude, at a $1.3 billion market capitalization, Core Laboratories is already priced for good things happening down the road and increasing cash flows. Given the negative long-term outlook, I feel one could require a bigger margin of safety when it comes to investing in CLB stock. With the approximate $50 million in FCF the company is making, a price half the current would provide much less risk and better upside from a conservative value investing perspective.

You might call me crazy for saying CLB stock could be interesting only if it crashes 50%, but that is exactly where the stock was trading 11 months ago and given the inherent volatility in the oil segment with swift changes of sentiment – it might happen again.

Anyway, see how the risk and reward fits your investment requirements, I am onto the next stock analysis. If you wish to see my portfolios and stocks that I cover, check my research platform.