CMCOM Stock Analysis – Risky Growth Bet

CM.com is a recent SPAC (special purpose acquisition company) that acquired a mobile services company based in the Netherlands. CM.com formed in 1999, and provides software for direct messaging, VoIP messaging, ecommerce payments and digital identification. The growth strategy has been to acquire a number of messaging and media startups over the recent years.

This CMCOM stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As. Here are the Bs already.

CMCOM stock price overview

CM.com stock has done really well since the IPO. The stock is traded on the Amsterdam stock exchange under the ticker AMS:CMCOM.

The company is still largely owned by the founders.

The market capitalization is 1.22 billion EUR. Let’s see about the business, fundamentals and conclude with an investment thesis.

CM.com business overview

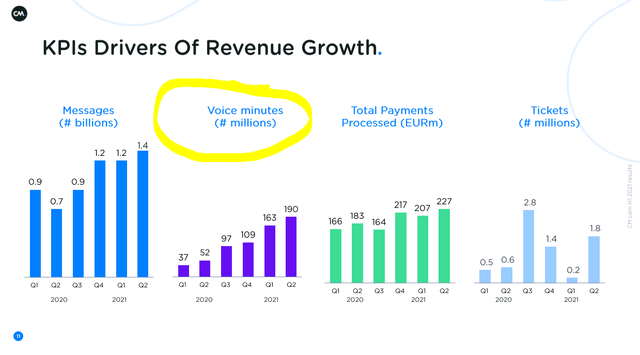

The current environment has been beneficial for the company as the technological shift has been fastened due to COVID. Therefore, all the businesses of the company have been experiencing growth, especially voice messaging.

The main revenue contribution comes from CPaaS (Communication Platform as a Service) while other businesses are likely interesting as the grow fast, but still not that significant in the revenue matrix.

The company is expecting slower growth ahead, but still at extreme levels of around 55% per year.

The strategy is to keep doing what they are doing and expand through acquisition and global scaling.

As with any other growth business, the investment levels are high and the profitability is uncertain, which is the key when it comes to investing.

Let’s see how the above fits a financial perspective.

CM.com stock analysis – financials

The company is clearly a growth company and if they reach their 30% yearly growth target, the current revenue of 196 million EUR should be at 727 million over 5 years.

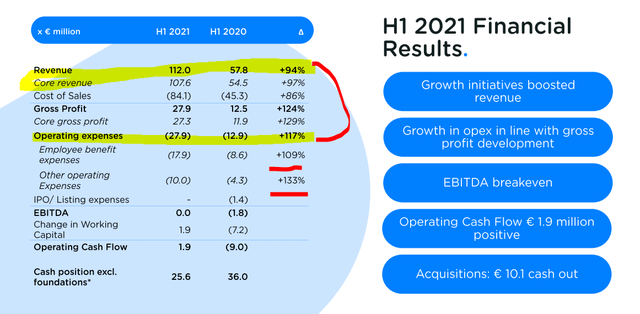

The next step for the company would be to reach profitability which is something they plan or better to say, hope to reach in the future with EBITDA levels above 20% in the long-term. For now, expenses have been growing faster than revenues which is not a good sign and makes the investment a risky growth stock investment.

CMCOM stock analysis – investment thesis

When it comes to investing in CM.com stock, it is all about what will happen in the future; will the company meet its 30% growth target, will it ever reach profitability, will it always have to reinvest every cent to stay ahead of the competition?

These are the questions that we cannot know the answers now. What we can do however is estimate on the possible scenarios.

If all goes well, in 2026 we might have around 700 million EUR of revenue with EBITDA of 140 million (20%). With fast depreciation of mostly intangible assets, taxes of 20% and 5% of revenues to be reinvested, I would expect 70 million of free cash flows. This would lead to a 5% FCF yield in the best-case scenario by 2026. From my perspective, this is too expensive for such a growth bet.

Plus, when the company starts growing significantly, other bigger competitors might become interested in the sector and eat the future profits away. I just read Peter Thiel’s book Zero To One and one of his key criterions for investing in growth stocks is that the product is 10 times better than what the competition has. Given the current negative profit margins, I don’t think CMCOM has a product 10 times better and therefore the business model is simply too risky for me to consider.

In the worst case scenario, the company doesn’t reach profitability, the growth subdues as the return on invested capital is negative, the acquisitions and the intangible assets have to be impaired and the situation becomes extremely bad. It reminds me of many other tech stocks that have fallen 99% after the dot-com bubble or other tech stock crashes. Therefore, if you must invest in stocks like CMCOM, make sure to carefully weigh your portfolio exposure, diversify the bets and assess the risk and reward of each position to best structure your portfolio.

Of course, I am a value investor and this is just an overview that I am doing as I am looking into all shares traded on the Amsterdam stock exchange. So, if you are more inclined to value investing than to betting on growth stocks, you might want to check my YouTube channel and subscribe to my newsletter.