Carnival Stock Analysis – Timing Is Key

Carnival stock (CCL) has been severely hit due to the coronavirus. The consequences will be felt for a long time and can’t be measured now. However, what we can do is to categorize the stock in order to know when is the best time to buy CCL.

I’ve recently discussed how Peter Lynch divided stocks into six categories which helped him a lot in reaching 28% yearly returns managing Fidelity Magellan.

The six categories are:

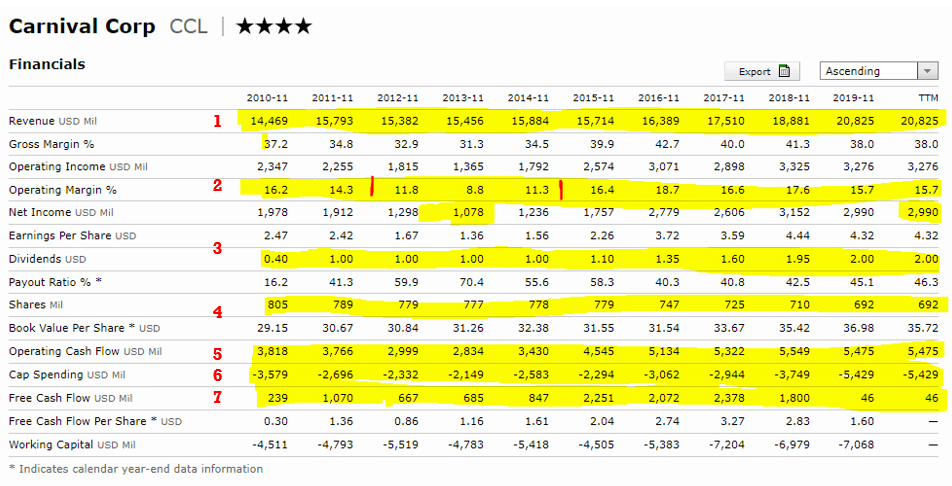

Carnival stock categorization

CCL stock has seen its revenue grow 33% over the past decade (line 1 in the below figure) which puts it into the slow growth category. However, from an investing perspective, perhaps the best categorization would be a cyclical one. Operating margins (line 2) are volatile considering the last recession period was around 2013, with the government shut down in the US and debt crisis in Europe. Net income in 2013 was just $1 billion while now it is $3 billion and dividends (line 3) doubled since. So, we could assume that earnings will suffer significantly in a recession and the current coronavirus situation certainly doesn’t help.

Source: Carnival Stock Morningstar

Now that we have categorized CCL, let’s see how to invest in it.

How and when to buy Carnival Stock

Sticking to Peter Lynch here is how he describes a cyclical stock:

- To flourish when the economy turns good again

- Suffer when there is no economic growth

- 50% drops are normal if you buy at the wrong part of the cycle

- You can wait for years before seeing another upswing (Ford down since 2013)

- Large and well-known companies that make the unwary stock picker most easily part with his money

- Timing is everything – watch for inventories and for new market entrants

- Stock usually declines when peak earnings is reached and investors expect next recession (look at Ford)

- Know your cyclical and figure out the cycles – In the car industry is 3 to 4 bad years followed by 3 to 4 good years. The worse the slump, the better the recovery.

- Easier to predict an upturn than a downturn in the industry.

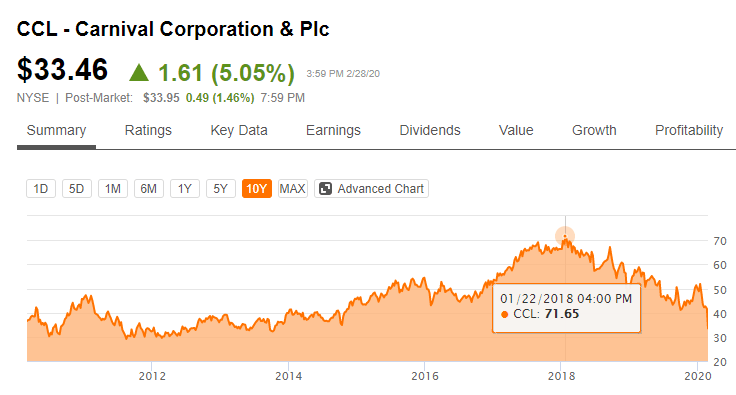

It is incredible how the above description perfectly summarizes CCL. The company increased net income from $1 billion to $3 billion as the economy turned good in the last 5 years (1). It will certainly suffer in the next recession (2). It is already down 50% from its peak in 2018 (3) and, given the circumstances, investors might have to wait a few years before the next upswing (4).

It is a very popular stock thanks to its current dividend growth and strong buybacks. This unfortunately attracts many unwary stock pickers that have been parting with their money for the last two years (5).

When it comes to investing in a stock like CCL, timing is everything and you have to check inventories and new entrants. The current situation is one where the company has 6 new ships entering service in 2020. The attractive margins have also attracted new competitors like Virgin Cruises. So we have a situation with increasing sector inventories (6) putting more pressure on short and medium term earnings.

The key with CCL, and the best time to invest is when things start to turn for the better withing a bad situation, like it has been the case between 2012 and 2015. Earnings have increased more than 200% and so did the stock. Now, it is unlikely that the company can again increase earnings 200% in the coming years, which at best makes it a slow growth company – a company to avoid according to Lynch. In the worst case and unfortunately most likely case, the coronavirus and possible recession will severely hit longer-term booking and earnings, and we might be looking at a few bad years ahead.

If you are interested in CCL, you should wait for things look really bad, that the current unwary dividend stock pickers capitulate and then, start accumulating before Wall Street gets it that things are turning for the best again as things usually do with a low debt cyclical stock.

For a deeper dive into the sector, capital expenditures, environmental issues and current coronavirus impact, please enjoy the video.

If you enjoyed this approach to stock analyses, please consider subscribing.