BHP Group: A High-Quality Cyclical Play in the Commodities Sector

If you want an in-depth video about BHP, you can watch it here:

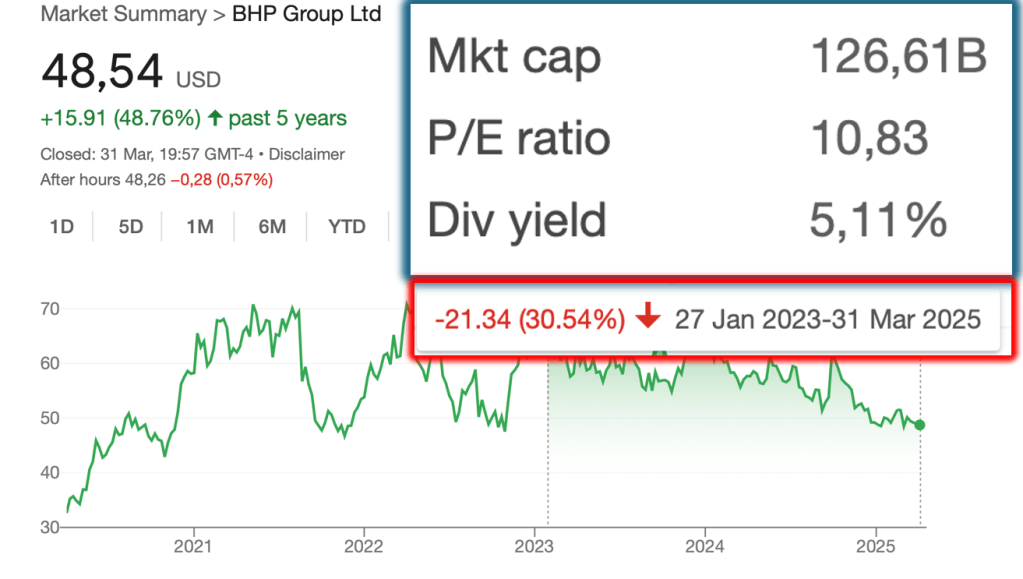

BHP Group (ASX: BHP, NYSE: BHP), one of the world’s largest and most diversified mining companies, has experienced a 30% decline in its stock price over the past two years. Despite this downturn, the company remains a powerhouse in the global commodities market, boasting a market capitalization of $126 billion, strong cash flow generation, and a resilient dividend policy. While short-term headwinds—such as fluctuating commodity prices and macroeconomic uncertainty—have weighed on the stock, a long-term perspective suggests that BHP is undergoing a cyclical correction rather than a structural decline.

For investors with a patient, value-oriented approach, BHP presents an attractive opportunity to gain exposure to high-quality mining assets at a reasonable valuation. The company’s diversified portfolio, low-cost production, and strategic investments in future-facing commodities like copper and potash position it well for sustained growth over the next decade.

BHP’s Resilience Through Market Cycles

Historically, BHP has demonstrated an ability to navigate downturns and emerge stronger. The company faced significant challenges in the past, including the 2015 Samarco dam disaster in Brazil and its ill-timed expansion into oil and gas, yet it managed to recover and continue delivering shareholder value. The current decline in share price is consistent with the cyclical nature of the commodities sector rather than a sign of fundamental weakness.

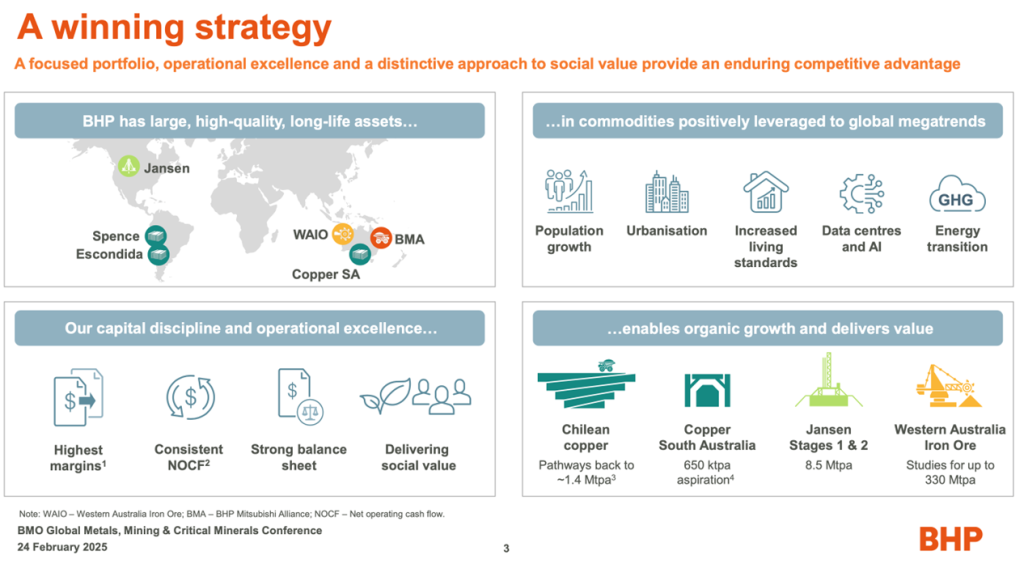

A Premier Asset Portfolio with Competitive Advantages

BHP’s strength lies in its tier-one mining assets, which are among the lowest-cost and most efficient in the world. These include:

- Iron Ore (Australia): BHP operates some of the most cost-efficient iron ore mines globally, with production costs averaging around $40 per ton. This provides a significant margin buffer even when iron ore prices decline.

- Copper (Chile & Peru): Copper is a critical metal for electrification, renewable energy, and electric vehicles. BHP is expanding its copper production through projects like the Escondida mine in Chile and potential acquisitions in copper-rich regions.

- Potash (Jansen Mine, Canada): The Jansen potash project is expected to eventually supply 10% of global potash demand and operate in the bottom quartile of production costs, making it a key long-term growth driver.

Financial Strength and Shareholder Returns

BHP has a long track record of generating substantial cash flows and returning capital to shareholders. Over the past decade, the company has distributed $83 billion in dividends and buybacks, translating to an average annual yield of around 8%. Even during weaker commodity price environments, BHP has maintained a disciplined approach to capital allocation, ensuring that dividends remain sustainable.

In its 2024 results, BHP reported 12 billion in EBITDA and declared 2.5 billion in dividends, implying an annualized yield of approximately 5%. This level of shareholder return is particularly appealing in an inflationary environment where commodities act as a natural hedge.

Commodity Market Outlook: Risks and Opportunities

Iron Ore – Stable but Facing Long-Term Headwinds

Iron ore remains BHP’s largest revenue contributor, but its outlook is mixed. While prices have been supported by steady demand from China, long-term growth is expected to moderate as China’s infrastructure boom slows. Analysts project iron ore prices to fluctuate between 60 per ton in downturns and 150 per ton during boom cycles, with consensus estimates settling around 80–80–90 per ton in the medium term.

BHP’s low-cost production ensures profitability even in weaker pricing environments, but investors should be prepared for volatility.

Copper – A Strategic Growth Driver

Copper is increasingly seen as a critical commodity for the global energy transition. Demand is expected to surge due to its use in electric vehicles, renewable energy infrastructure, and power grids. BHP is well-positioned to benefit from this trend through expansions in Chile and potential acquisitions.

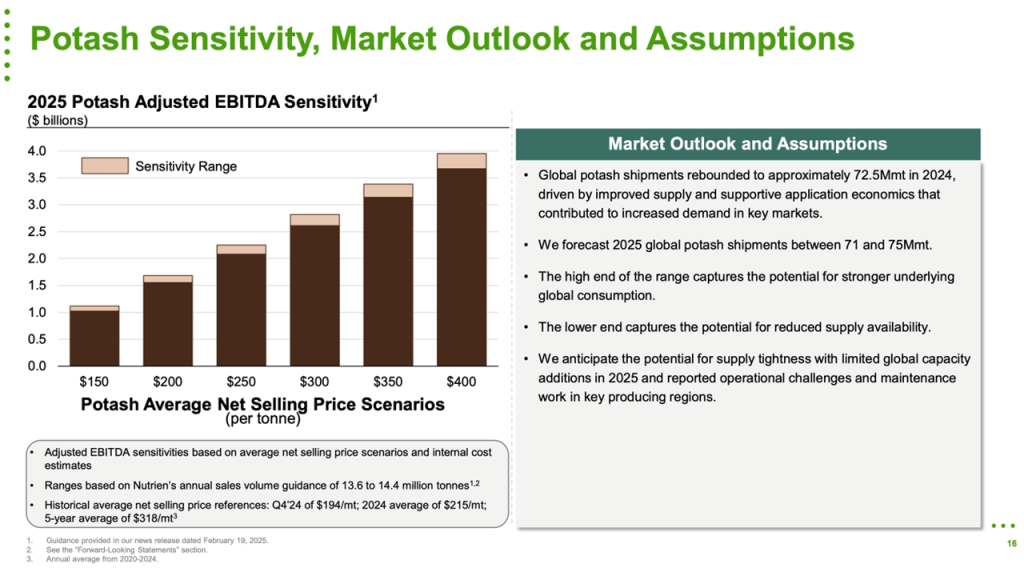

Potash – A Long-Term Bet with Upside Potential

The Jansen potash project represents a major long-term growth opportunity. Once fully operational, it is expected to generate over $1 billion in annual free cash flow by 2030. However, near-term profitability may be subdued due to oversupply in the potash market. Investors should view this as a long-term play rather than an immediate earnings catalyst.

Valuation and Investment Considerations

Intrinsic Value Estimate

Assuming a 4% long-term growth rate and a terminal multiple of 20x, BHP’s intrinsic value is estimated at $52 per share. At current prices, the stock offers a potential 10% annualized return, excluding deep-cycle buying opportunities.

Key Risks

- Commodity Price Volatility: BHP’s earnings are heavily influenced by iron ore, copper, and coal prices, which can swing dramatically.

- Macroeconomic Slowdown: A global recession could further pressure commodity demand.

- Execution Risks in Growth Projects: Delays or cost overruns in projects like Jansen could impact future cash flows.

Conclusion: A Compelling Long-Term Investment

BHP Group remains a high-quality, cyclical investment with strong fundamentals, a diversified asset base, and a commitment to shareholder returns. While short-term volatility is inevitable, patient investors can capitalize on the current price weakness to build a position in one of the world’s premier mining companies.

Investment Strategy

- Dollar-cost averaging may be prudent given commodity price uncertainty.

- Monitor macroeconomic trends, particularly Chinese demand and global energy transition policies.

- Consider BHP as both an income play (5–6% dividend yield) and an inflation hedge.

For investors willing to endure cyclical downturns, BHP offers a compelling mix of value, growth, and income potential.

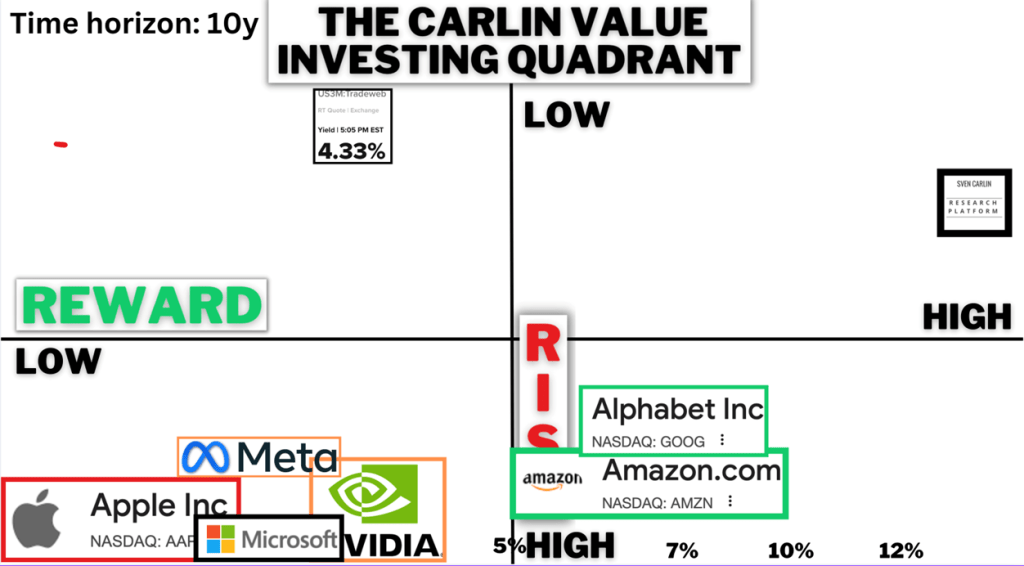

Value Investing Risk & Reward Quadrant (check all the stock analyses)