Beyond Meat Stock Price Forecast – Negative Outlook on Contracting Margins, Debt Issues and Increasing Competition (Food Test)

I don’t think Beyond Meat needs much introduction but for those that don’t know about it, it is a producer of plant-based food products that resemble originally meat made products like burgers and sausages. Let’s start with a business overview, then discuss the competitive advantages, the fundamentals, make a valuation and conclude with an investing thesis.

Here is the BYND stock video analysis, full BYND stock written analysis continues below.

Beyond Meat Business Overview

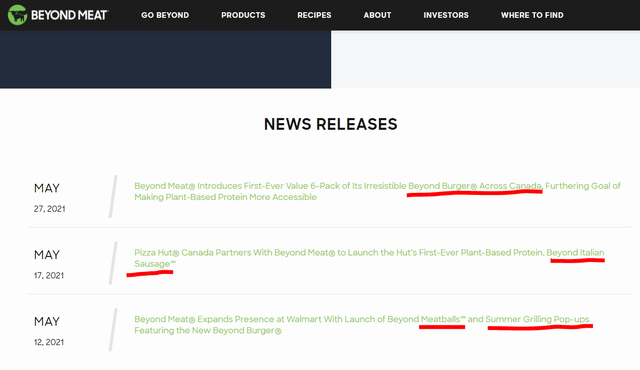

Beyond Meat has been growing fast in the past and is constantly expanding its products range and markets. Here below are just examples from the most recent news releases of a new Beyond Burger 6 pack for Canada, a Beyond Italian Sausage for Pizza Hut and more Beyond Meatballs for Walmart.

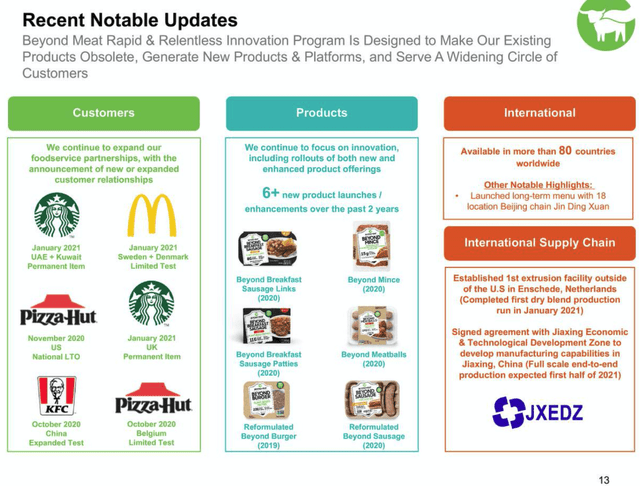

The company has been expanding fast through partnerships like McDonalds, Starbucks, KFC but that also means it will likely be accepting lower margins given that we all know companies like MCD are very tough to negotiate with.

Here is just an example of Beyond Meat’s meat substitute products.

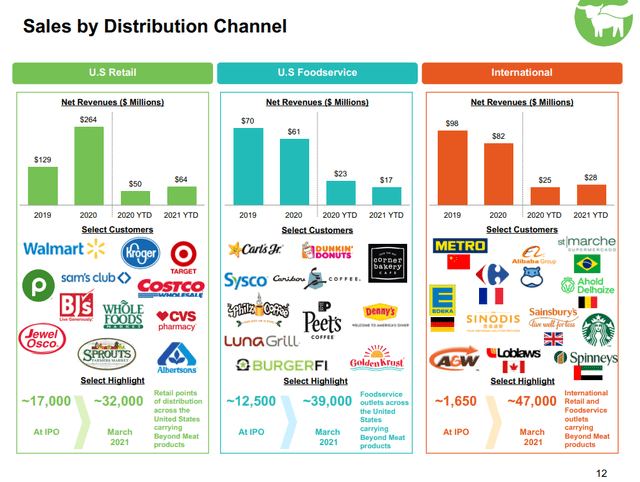

Beyond Meat has expanded extremely fast over the last years and is now well distributed internationally too.

Market Overview

The plant-based food market is growing fast and has grown 400% over the past two years in Europe where meat substitute products are already at 2.5% of the actual meat market. If the growth continues, things will be positive for Beyond Meat too.

There is plenty of room to grow as meat substitutes are highly sought in the environment. According to ProVeg’s research, plant-based substitute meat products come in second only after milk.

The trend for plant-based foods is very positive and growing fast. However, that is just one part of the story. We as investors have to also look at margins, competition and long-term trend sustainability because you want to invest in a strong trend while a fad is certainly something you don’t want to invest in. To do a deeper analysis on whether Beyond Meat is just a fad or might actually be a trend, we have even tested the product.

Beyond Meat Comparative Product Testing

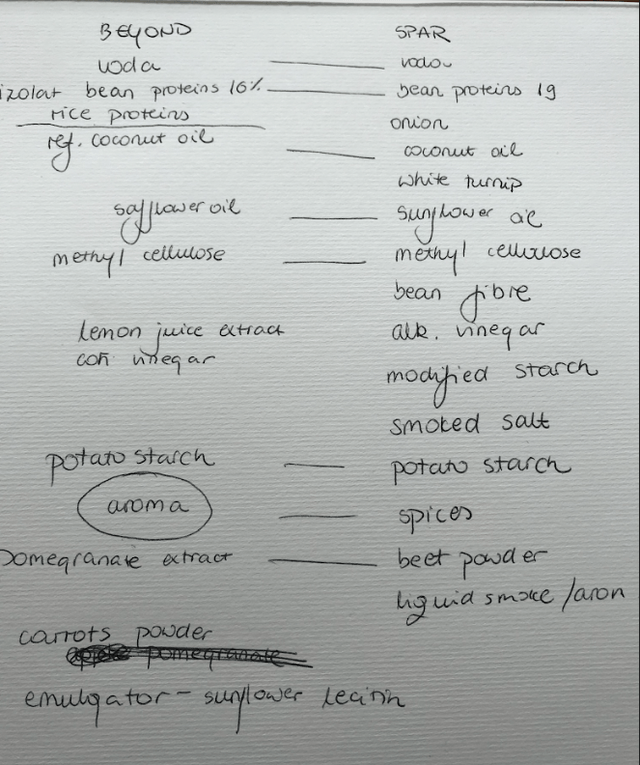

We went to the store that offers the product in my country (Slovenia) to do proper field research and found the following:

Beyond Meat’s package was squeezed on the top shelf and actually hidden. To make things worse, it was next to a few competitors and all the competitors have 50% lower prices on what seems the same product. My wife, who is a healthy food specialist (Naturally Ana channel) immediately analyzed Beyond’s ingredients and compared them with the private label from the supermarket’s own production. The comparative verdict on an ingredient basis is that there is practically no difference except in the price that is half of Beyond’s.

Apart from small differences where Beyond Meat uses aromas while Spar uses spices or a mix or rice and bean proteins versus just bean proteins, there isn’t actually a significant difference. Thus, the basis of Beyond’s value is the brand and the taste, which is the next step in our research.

Even if my wife says plant-based burgers are not food but just a food product and you would actually be healthier if you ate organic minced meat, we have tested and compared Beyond’s burger and Spar’s 50% cheaper counterpart.

It could be that market chains put Beyond’s products on the shelves so that people try them out, compare and then go for the private label for 50% of the price.

Now, about the taste, here is my comment:

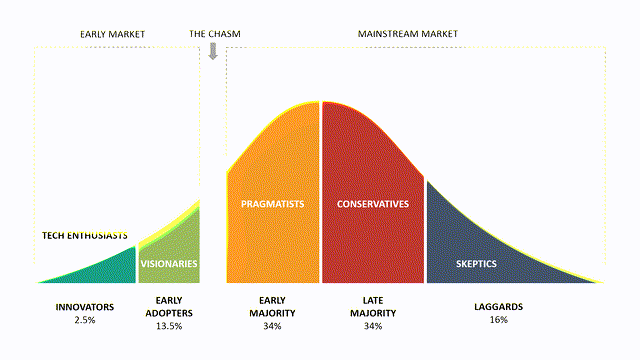

Personally, the taste difference is really subtle, and even as I will certainly not use the above as food, we just tested it, but no point in paying 50% more for practically the same. This is extremely important for our business analysis because it might have huge impacts on BYND’s future margins. As you use up the enthusiasts for such products, it is very likely your margins will need to be much lower to reach others in the mainstream market which is Beyond’s goal as a company.

The management is positive about Beyond becoming a mainstream food option and is investing accordingly. My worry is that if they do not become mainstream, then you are in a pickle if you are an investor.

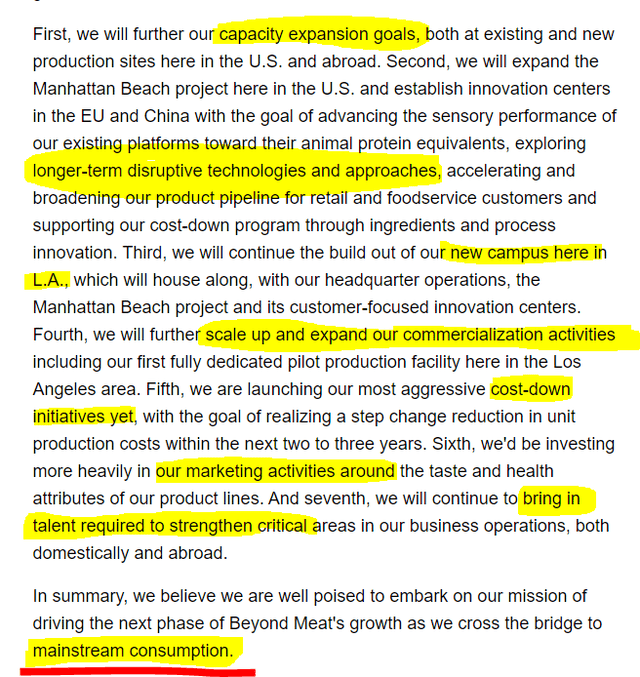

The management has a seven-factor strategy to achieve mainstream consumption and those are capacity expansions, new technologies (yes, that is exactly what I want to eat – haha), new campuses, stronger commercialization, lower costs, increase marketing and hire more people.

Let’s put the above business analysis into an investing perspective.

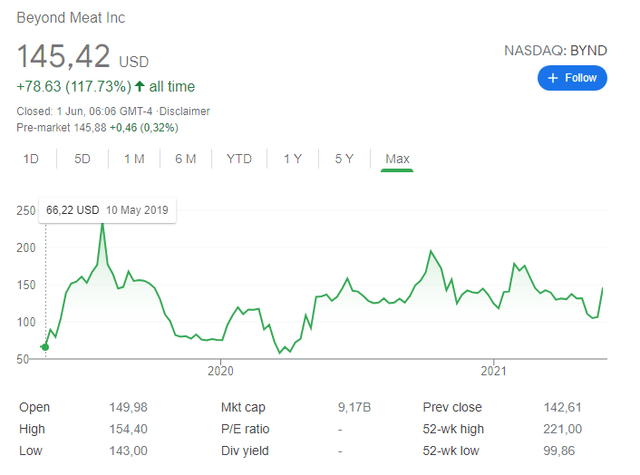

Beyond Mean Stock Price Overview

Since the IPO in 2019 BYND stock has been extremely volatile, one would call this ‘a traders paradise’. After the initial IPO craze the stock price returned to IPO levels, then spiked again and we have seen another super spike over the last few days.

The market capitalization is $9.17 billion which is the key number to compare our stock valuations with.

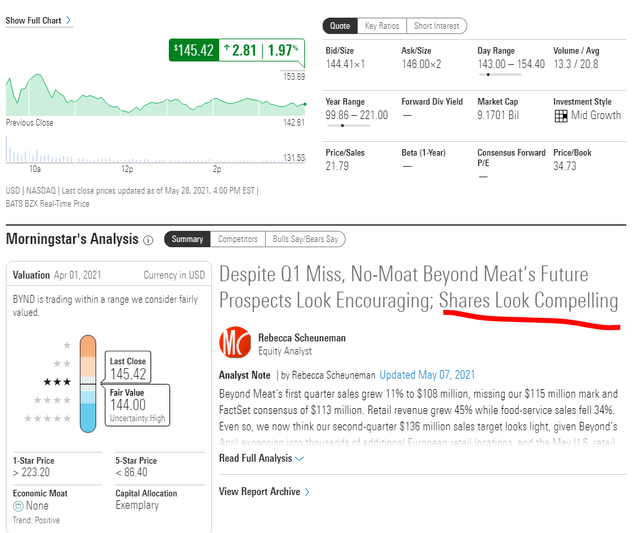

Morningstar is positive about BYND stock but as always you have to check their assumption where their fair value estimate implies a 2023 enterprise value/adjusted EBITDA of 35. EV/adjusted EBITDA of 35 is a very vague number to me, definitely looks smart when you use it but has absolutely no significance when it comes to real investing.

I prefer to look for actual profits that might turn into dividends and then see how far should Beyond Meat go and when it could reach such a stage.

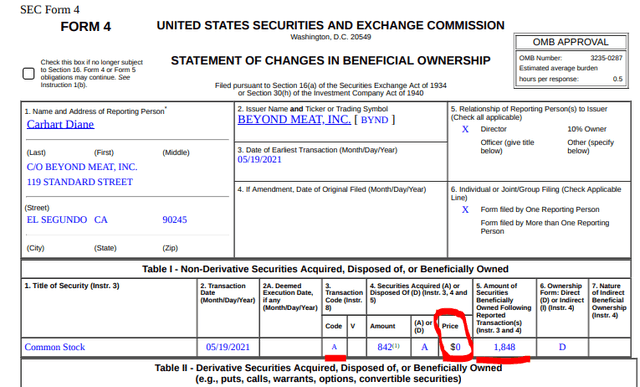

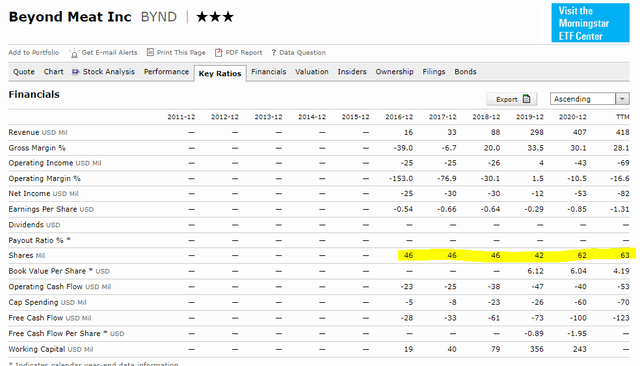

Just to touch on the number of BYND shares outstanding, there had been a big jump after the IPO and now we see a slow increase likely as options vest. A quick note here, if you look at BYND’s SEC filings, you will see that there are lots of insiders trading and on an aggregate basis it might look like there is no impact on the number of shares outstanding. I just want to notify that these insiders usually acquire the stock for $0 and then sell at market price which is something to keep in mind.

BYND’s number of shares outstanding looks stable.

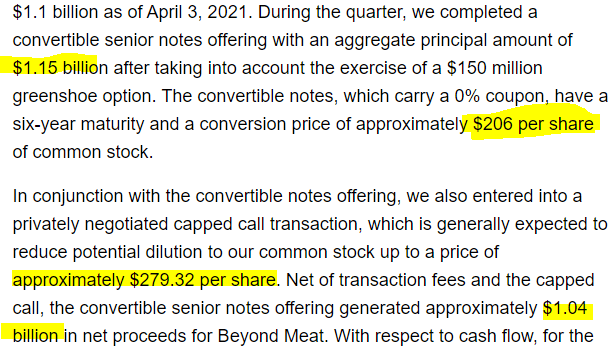

The company has recently issued a $1.15 billion convertible bond which is something to keep in mind because if things go well, then it isn’t a worry, but if things go bad, then the bond owners have a huge weight on the company and could actually become the owners of the company where you can’t do much about it anymore.

To note that net of fees, Beyond got $1.04 billion thus the upfront cost on the so called 0% financing is almost 10%, without mentioning future dilution costs and eventual cap maintenance. The conversion price is approximately $206 per share of common stock and the capped call transaction should prevent dilution up to a share price of $279.32 per share.

Let’s discuss how the above impacts the fundamentals.

Beyond Meat Stock Analysis – Fundamentals

Total 12-month trailing sales are $418 million so the price to sales ratio on a $9 billion market cap is 21.79. I will not say that is high or not, I will just show what has to happen with BYND in the future to justify the current price and then you can make your own conclusion and see how the risk and reward fit your portfolio.

Gross margin is 28%, and significantly down compared to previous quarters and a high of 38%, cash flows are negative and at $123 million which is logical given the high investment levels leading to fast growth.

Growth is expected to increase significantly in and beyond 2021 as the food-service business recovers from the pandemic and as the two new facilities in China and the Netherlands ramp up.

Of course, as things are still scaling, it is difficult to model future margins, but one can try doing that and then see what comes out.

Let’s see how fast should BYND grow ahead to justify the current market capitalization from an absolute investing perspective where what you care about are earnings and dividends.

Beyond Meat Stock Valuation

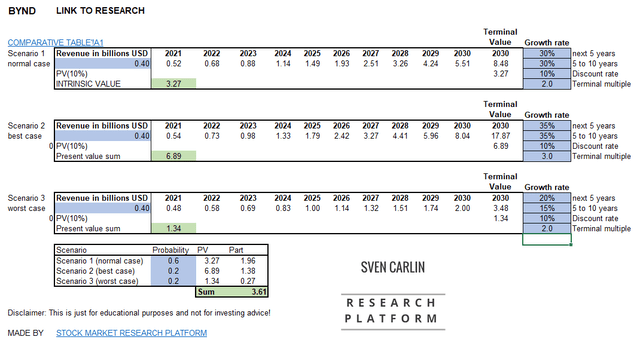

Let us assume 30% growth over the next 10 years, that would lead to more than $5 billion in sales. With a net profit margin of 5% where we can’t really know if it will be ever achieved, but still if it happens, we could expect $250 million of profits.

BYND stock valuation – Source: Sven Carlin Research Platform (free template download)

My intrinsic value in such a situation, where the price to sales ratio is 2 ten years from now, that would equal to a PE ratio of 30 with a 5% net profit margin, which I think would be a fair valuation in 2030, is $3.27 billion at a 10% discount rate that I usually use for comparing investment opportunities. This would see BYND stock as significantly overvalued.

In a best-case scenario shown below, with growth of 35% per year and a terminal multiple of 3 on sales, turning into a PE ratio of 45 down the road, the present value for BYND gets to $6.89 billion where it would still be slightly overvalued.

In the worst-case scenario, where the growth rate is ‘just’ 20% over the first 5 years and then 15%, with a price to sales ratio of 2, still implying a PE ratio of 30, my present value for BYND is $1.34 billion which would make BYND extremely overvalued now.

BYND stock valuation – Source: Sven Carlin Research Platform (free template download)

All the above calculations assume BYND will reach a stable net profit margin of 5% which is another doubtful factor. As Spar and other private labels have practically the same product as BYND offers being sold right next to it in the store at half the price, reaching profitability for BYND might be a long shot. The industry operates at such thin margins where BYND spends money on advertising, brings customers into the store and then those buy the private label too – that is a very difficult market to operate in.

Plus, it is really difficult to have a competitive advantage in the industry also because Beyond Meat is competing with much bigger players. Few know it, but it is actually Archer Daniel Midland (ADM stock analysis) that is the biggest producer of plant-based foods.

BYND Stock Investment Conclusion

There are two strategies when it comes to investing in BYND stock; the bigger fool strategy and the absolute investing perspective strategy.

For the bigger fool strategy to be successful you just need someone in the future that will be happy to pay more for BYND stock than what you paid for. Given it is likely that only few of BYND’s stock owners understand how to make a proper valuation as BYND is a hot meme stock on reddit, you might find your bigger fool if the company delivers good news.

However, to do well with such a strategy you should read Reddit posts and understand how will the short-term supply and demand for the stock work, I can’t help you there.

From an absolute investing perspective, you must try to understand the business and find an answer to the possibility for BYND to increase sales more than 10 times over the coming decade and do that profitably with a product that has little differentiation from competitors. If find that possibility to be very small.

Both of the above strategies are bets I certainly don’t want to take. However, the trend for plant-based foods is very positive, so one might find interesting investments by looking for the old and boring food stocks that deliver the ‘picks and shovels’ or better to say ingredients to these hot plant-based stocks like BYND. That is what I am looking for and the reason why I analysed BYND too.

Of course, miracles can always happen but I certainly don’t want to bet my financial future on those.

Additionally, this reminds me so much about the exuberance related to Whole Foods and the extreme growth assumptions that subsequently faded and the story ended with Amazon acquiring them at a normal 10.4 EBITDA ratio.

I wrote this analysis to see a bit what is going on in the sector as I am curious about it. I will write more analyses so if you are interested consider subscribing. If you are not interested in plant-based food stocks, you might consider subscribing fore my absolute return investment approach shown above.

bout the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.