Berkshire Hathaway: A Fortress Built for Long-Term Compounding

The full video analysis of Berkshire is on my channel if you want a more in depth analysis:

Berkshire Hathaway, under the leadership of Warren Buffett, has long been regarded as a financial fortress and a beacon for value investors. With a track record of delivering 20% annual returns over six decades—compared to the S&P 500’s 10%—Berkshire stands as a testament to the power of disciplined, long-term investing. As the company prepares for a potential recession, now is an opportune moment to analyze its current position, valuation, and future prospects.

Berkshire’s Enduring Strength

Berkshire Hathaway is more than just a conglomerate; it’s a financial lighthouse that guides investors toward sound decision-making. Its business model is built to last, combining a diversified portfolio of wholly owned businesses, strategic equity investments, and a massive insurance operation that generates costless float. This unique structure allows Berkshire to compound value over time while minimizing risk.

One of Berkshire’s key strengths is its ability to avoid value-destructive practices common in the corporate world. Unlike many S&P 500 companies that engage in excessive buybacks or issue stock options to management, Berkshire focuses on reinvesting profits into high-quality businesses. This approach ensures that the company continues to grow its intrinsic value over the long term.

Analyzing Berkshire’s Earnings and Valuation

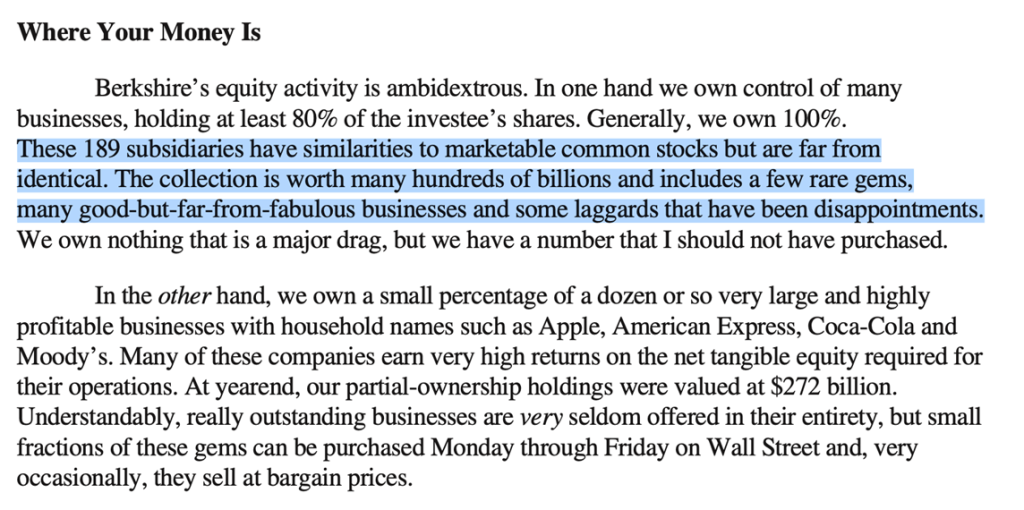

Berkshire’s recent earnings highlight the cyclical nature of its insurance business. In 2023, insurance underwriting generated $9 billion in profits, driven by favorable tailwinds such as subdued inflation and higher pricing after natural disasters. However, these results are exceptional and not indicative of long-term performance. Over the past two decades, Berkshire’s insurance underwriting has averaged $1.5 billion annually, with occasional losses during catastrophic events.

On the investment side, Berkshire’s $320 billion cash pile, primarily invested in U.S. Treasury bills, has been a significant source of income. However, with yields declining from 5.38% to 4.3%, investment income is expected to decrease in 2024. Despite this, Berkshire’s diversified portfolio of businesses—including railroads, energy, and other stable operations—continues to generate consistent earnings.

Using an intrinsic value template, Berkshire’s current market capitalization of $1.08 trillion suggests a long-term return of approximately 5-7% annually, assuming a 6% earnings growth rate and a terminal price-to-earnings (P/E) multiple of 15. While this may seem modest, it reflects Berkshire’s size and the conservative nature of its valuation. In a best-case scenario, with an 8% growth rate and a higher terminal multiple, Berkshire could deliver returns of 7-8% annually.

Warren Buffett’s Recession Playbook

A key takeaway from Warren Buffett’s latest shareholder letter is his preparation for a potential recession. With $300 billion in cash and short-term Treasuries, Berkshire is poised to capitalize on market dislocations. Buffett has historically bet heavily during periods of economic uncertainty, acquiring high-quality businesses at bargain prices. This strategy has been a cornerstone of Berkshire’s success, and it appears that Buffett’s successor, Greg Abel, will continue this approach.

Buffett’s caution is evident in his recent actions. Despite the market’s exuberance, Berkshire has scaled back its share buybacks, signaling that the current valuation does not offer a significant margin of safety. However, for long-term investors, Berkshire remains a low-risk investment with the potential for steady returns. Even in a worst-case scenario—such as a severe recession—Berkshire’s liquidation value of $700-800 billion provides a substantial margin of safety.

Is Berkshire a Buy?

While Berkshire’s current valuation may not offer the same upside as in previous years, it remains a compelling investment for those seeking stability and long-term compounding. For investors with a value-oriented mindset, allocating a portion of their portfolio to Berkshire—perhaps 10%—is a prudent strategy. If the stock price declines further, increasing the allocation could enhance returns.

Berkshire also serves as a hedge against market volatility. While it may not be immune to a recession, its strong balance sheet and diversified operations make it more resilient than the broader market. In a downturn, Berkshire’s ability to deploy capital at attractive prices could further enhance its long-term value.

Key Takeaways from Buffett’s Letter

Buffett’s letter underscores several important themes:

- Patience and Preparedness: Berkshire’s success is built on waiting for the right opportunities and acting decisively when they arise.

- Focus on Quality: Buffett emphasizes the importance of investing in outstanding businesses, even if only small fractions are available.

- Cash as a Strategic Tool: While cash is not ideal in an inflationary environment, it provides Berkshire with the flexibility to capitalize on market inefficiencies.

Conclusion

Berkshire Hathaway remains a cornerstone of value investing, offering investors a unique combination of stability, growth, and resilience. While its current valuation may not present a compelling buy opportunity, its long-term prospects remain strong. For investors, Berkshire serves as both a financial fortress and a model for disciplined, long-term investing. As Warren Buffett prepares for the next recession, so too should investors position themselves to take advantage of the opportunities that lie ahead.

If you want to learn more about value investing and the risk and reward of stocks, check out my Value Investing Risk & Reward Quadrant.