Aurelia Metals Stock Analysis – a Bet on Exploration Going Well For Now!

Summary:

- Australian miner producing gold but exploring zinc and lead

- Net cash position but with short mine live (4 years)

- However, great new exploration intersections counter the low reserves

- I conclude by putting Aurelia into a global mining investing perspective

Content

Aurelia Metals is an Australian miner that produces mostly gold for now but has exploration interest with zinc and lead. It has a net cash position. When it comes to whatever related to investing, the key differentiator between the bad and the good is always cash. However, let’s dig deeper. (Slides source: Aurelia)

They own and operate gold, zinc, copper and lead mines.

They expect 115 to 130 thousand gold ounces of production with costs of A$1,000 ($720) and what is very important, they expect to spend between $35 and $48 million on growth. Growth spending is always uncertain. This leaves about $35 million of operating cash flows. After taxes and other general expenses, there will not be much left.

The mine life is just 4 years.

The short mine life is forcing the company to invest heavily into exploration, which when it comes to Australia, usually means deeper and more expensive. Most of their targets are previously mined mines that are open at depth. As for the surface prospects, keep in mind that only 1 in 3000 surface prospects eventually becomes a mine.

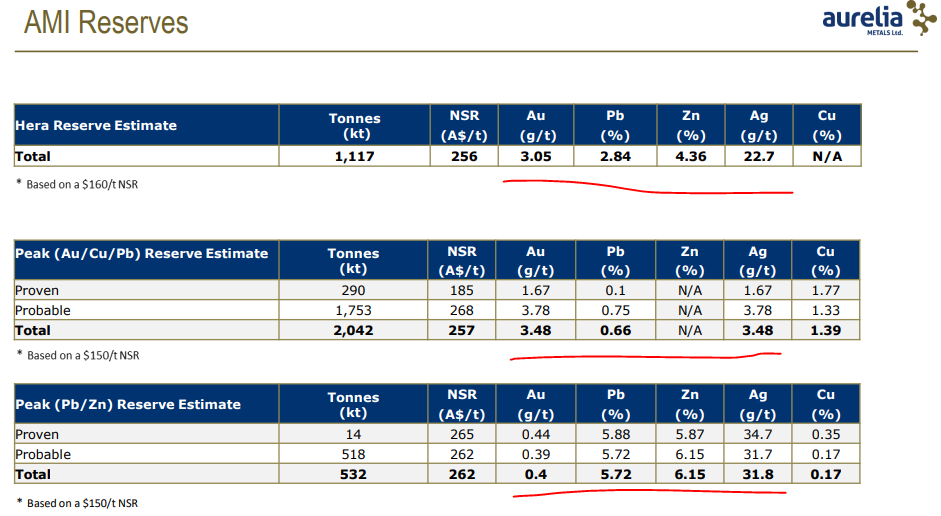

Plus, the ore grades of the current resources are significantly lower than those of the reserves. This means that to turn the resources into reserves, one should see much higher metal prices.

The short mine life and lower grade resources lead me to believe, it all depends on exploration with Aurelia. And when the exploration is deeper, it also means more expensive. Before looking at their exploration efforts more in depth, let’s look at the current operations.

The short mine life and lower grade resources lead me to believe, it all depends on exploration with Aurelia. And when the exploration is deeper, it also means more expensive. Before looking at their exploration efforts more in depth, let’s look at the current operations.

Current operations

Mining costs are going up as they go deeper. One should now look at the sequence of the ore they will mine in the future. The volatile costs increase the uncertainty as we don’t know what to expect next qua costs.

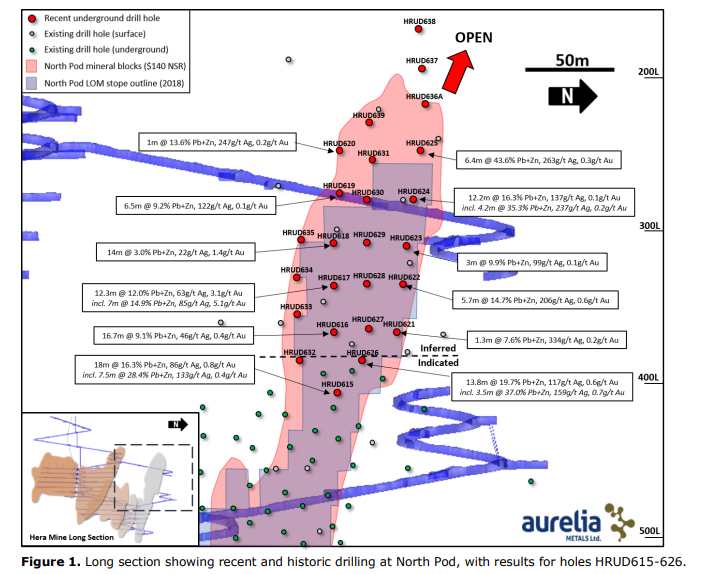

Further, the exploration results are mixed, 7 meters of copper at 1%? Nevsun at Timok had interceptions of 700 meters above 1% copper.

The following slide shows how complex is what they are doing. I would call it ‘deep and thin’.

However, their recent update shows nice and significant zinc and lead intersections. But, now the company depends on the price of zinc going forward and you can read my analysis of the zinc sector here.

The most recent exploration data shown above includes pretty good intersections but we are still talking about a few trucks of ore.

Plus, more drilling needs to be done to bring this to reserve level. The management will do that but then again, it will further depend on the price of zinc and lead and more future exploration.

Fundamentals

When it comes to fundamentals, they are showing a net cash position of A$105 million, but they have also raised equity for the same amount in the year and a half.

Book value is A$0.27 per share. Cash flows have been high in the last reported year but most of that went for the acquisition, growth and exploration.

Conclusion

Aurelia is a small, underground junior miner and you never know what can happen there. The intersections are not stellar, definitely not large, and not something that would make me say WOW. It is simply to risky for any kind of investment in my opinion, like most junior miners are.

When it comes to investing in miners, given the market’s volatility, you can often by what is there at a discount and get what might be there for free. With Aurelia, you are, at the current market capitalization, paying for what might be there, which is something I am not comfortable with. To each his own personal strategy.

However, given the low coverage junior miners have, one has to simply keep digging until you find the miner with great intersections, high potential and low risk. Sounds impossible, but that is what I am looking and I find it here and there. As for Aurelia, it simply doesn’t fit the description unfortunately.

For current Aurelia investors, the market cap is A$795 million and even if they continue to make $150 million in free cash flow over the next 4 years, what is included in the reserves, the reserves don’t cover for the price. So, as it is the case with many miners, it is a bet on exploration and prices. Good luck!

Sven Carlin is an independent stock market researcher running the Sven Carlin Stock Market Research Platform.