ASML Earnings Analysis: Navigating Short-Term Uncertainty for Long-Term Value

If you want an in depth video explaining ASML, you can watch it here:

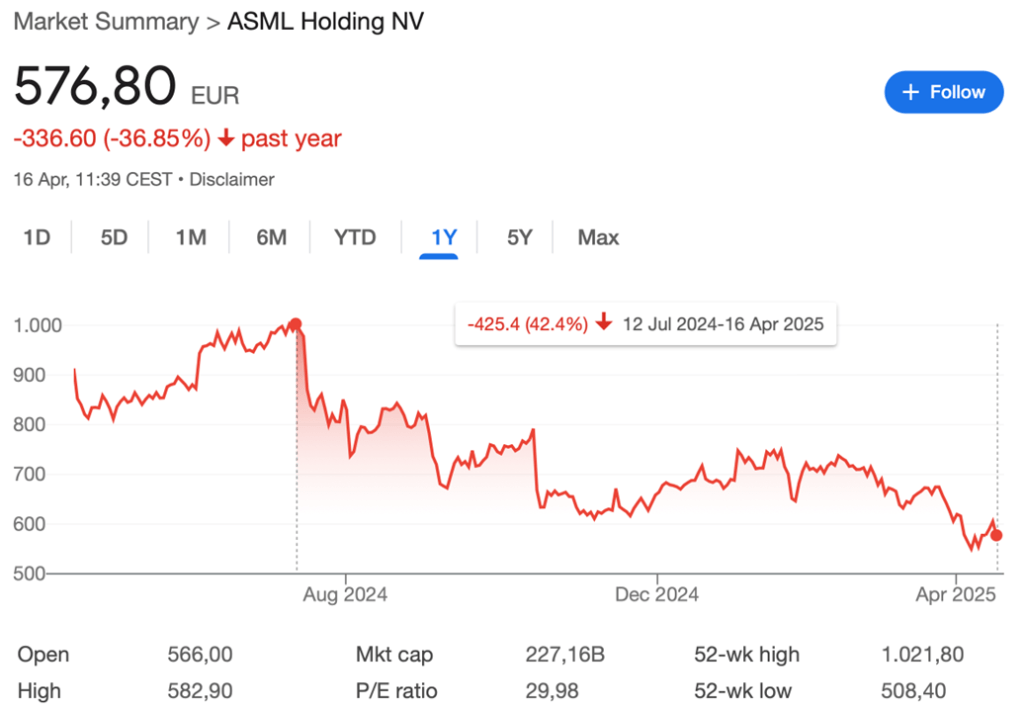

The recent earnings report from ASML has once again placed the semiconductor giant in the spotlight, particularly within the context of its risk-reward profile. While the stock has faced significant headwinds—down 42% over the past 10 months and dipping further on tariff concerns—the core question for value investors remains: How do we differentiate between short-term market noise and the enduring strengths of ASML’s business model?

Short-Term Volatility vs. Long-Term Durability

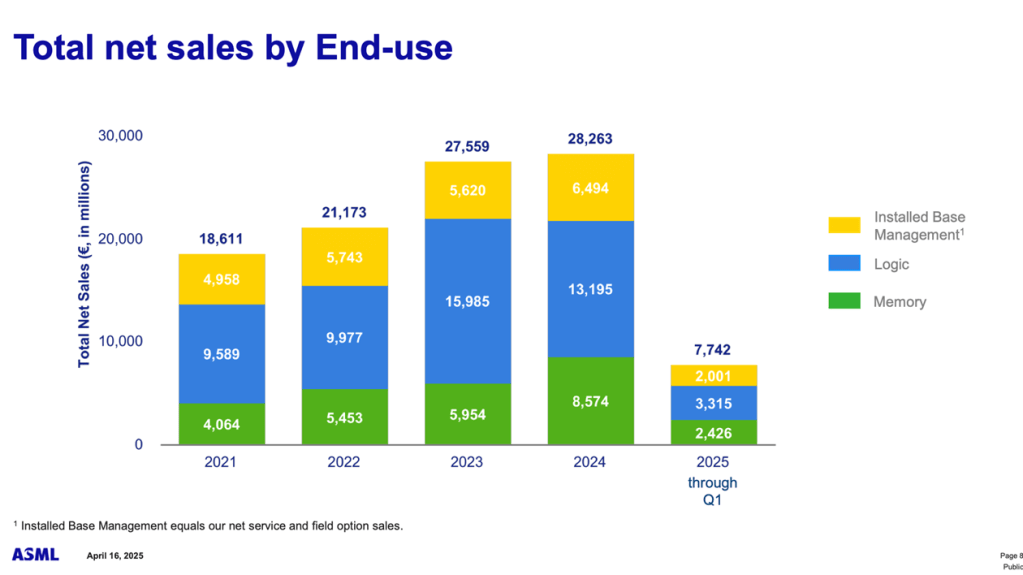

Market reactions often hinge on transient uncertainties—tariffs, geopolitical tensions, or near-term guidance adjustments. In ASML’s case, Wall Street expressed disappointment over net bookings, which fell short of expectations. However, these fluctuations obscure the underlying resilience of the company. ASML’s CEO acknowledged the current “highly uncertain” environment but reaffirmed expectations for growth in 2025 and 2026, driven by the relentless expansion of artificial intelligence (AI) and semiconductor demand. The industry’s revenue is projected to surpass $1 trillion by 2030, with ASML positioned as a critical enabler of this growth.

Financially, ASML’s fundamentals remain robust. The company reported stable earnings of €7.7 billion, with gross margins expected to climb to 56-60% in the coming years. While sales growth may appear muted in the near term—with 2025 revenue guidance ranging between €30 billion and €45 billion—the long-term trajectory remains compelling. The key for investors is to look beyond quarterly volatility and focus on ASML’s technological moat, competitive advantages, and profitability.

Intrinsic Value Assessment

To gauge ASML’s true investment potential, we turn to an intrinsic value analysis. Using conservative estimates, we model three scenarios based on management’s guidance:

- Base Case (75% Revenue Growth Over 5 Years): Assuming earnings per share (EPS) of €20 this year, growing at 10% annually (plus a 4% boost from buybacks), and a terminal price-to-earnings (P/E) multiple of 15, the intrinsic value lands at €395 per share. This suggests a solid margin of safety at current prices.

- Bull Case (Doubling Revenue): With EPS reaching €48 over the same period and a terminal P/E of 20, the intrinsic value approaches €1,000 per share, reflecting the potential for significant upside during periods of market exuberance.

- Bear Case (50% Revenue Growth): Even under this subdued scenario, with EPS growth slowing to 5% and a terminal P/E of 12, the intrinsic value stabilizes around €275, indicating downside protection.

The Buyback and Dividend Advantage

ASML’s capital allocation strategy further bolsters its appeal. The company returns substantial cash to shareholders through a 30% dividend payout ratio (€6.40 per share) and €10 billion in annual buybacks (a 4.4% yield). These buybacks systematically enhance per-share metrics, providing an additional tailwind to earnings growth.

Cyclicality and Sentiment: A Value Investor’s Opportunity

Semiconductor stocks are inherently cyclical, oscillating between periods of panic and euphoria. While ASML may face further volatility—potentially testing €400 in a worst-case scenario—its long-term growth drivers remain intact. The AI revolution, coupled with expanding semiconductor applications, ensures sustained demand for ASML’s cutting-edge lithography systems.

Conclusion

ASML represents a classic case of short-term uncertainty creating long-term opportunity. For investors willing to endure cyclical swings, the stock offers an attractive entry point with a projected 12% annual return under conservative assumptions. The lower the price falls, the more compelling the valuation becomes—embodying the essence of value investing.

As always, the key is patience. Market sentiment will eventually align with ASML’s fundamental strengths, and those who capitalize on today’s dislocation may reap substantial rewards.

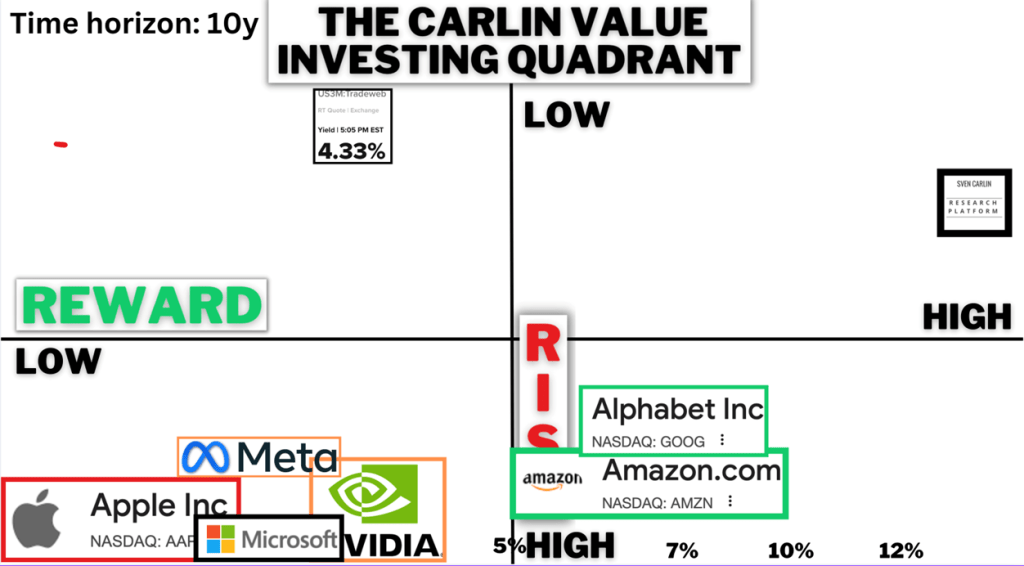

Value Investing Risk & Reward Quadrant (check all the stock analyses)

v