ARE THE STOCK MARKET AND ECONOMY IN A BUBBLE? 7 FACTOR EXPLANATION

I recently summarized Dalio’s last book, Big DEBT CRISES and there he shares his questions, check list, to see whether the stock market or economy is in a bubble or not. In today’s article, in light of the FED’s tightening, we are going to go through his questions, to see whether we are in a bubble or not.

Source: Big Debt Crises

Good day fellow investors,

my name is Sven Carlin and I am an independent investor, independent thinker who doesn’t really like to follow the crowd, that has served me well in my life and, I have the feeling it will serve me well in the future too. Let’s go through Dalio’s questions one by one and then conclude with what to do, where Dalio’s option is to have an all-weather portfolio.

We are going to look at whether the US economy and stock market are in a bubble. As for Europe, I’ll make a special article about it due to the many economies.

- PRICES ARE HIGH RELATIVE TO TRADITIONAL MEASURES

The US stock market is expensive and prices are much higher than traditional measures.

Source: Multpl

A look at the cyclically adjusted price to earnings ratio for the S&P 500 that takes into account 10 years of earnings, shows how stock prices were higher only during the dot-com bubble. But, let’s not focus only on stocks, let’s look at housing.

Source: Longtermtrends

The home price to income ratio is not higher than it was in 2007 but is getting close to it and it is much higher than it was in the past 50 years. Incomes were low in the 1950s so that isn’t really comparable.

To answer question one: yes, prices are high relative to historical measures.

2. PRICES ARE DISCOUNTING FUTURE RAPID PRICE APPRECIATION FROM THESE HIGH LEVELS

If we take a look at the S&P 500 and at S&P 500 forward expected earnings, all we can see is fast growth.

Source: FACTSET

So, huge growth is expected, S&P 500 actual earnings are at 116 points while the market expects them to be at 175 points in the next 12 months.

Source: Multpl

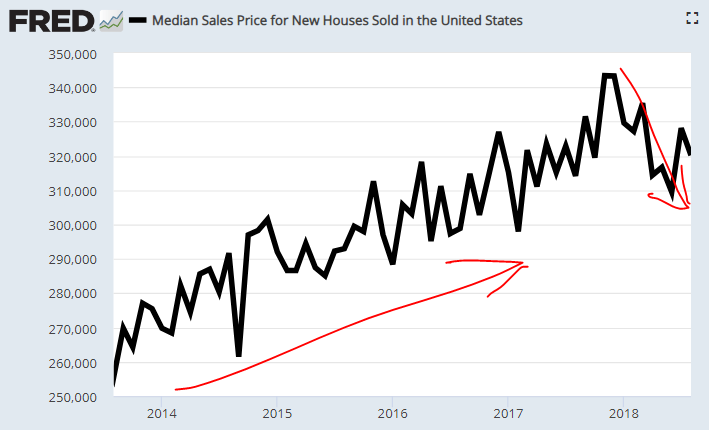

As for home prices, the huge run up in prices up to 2018 showed bubble characteristics but it has been cooling of as interest rates go up.

Source: FRED

So, perhaps what we have seen up to December of 2017 will again be called a bubble as higher interest rates inevitably put pressure on asset prices. Not yet on stocks as the sentiment is still strong but you can’t escape when it comes to housing.

ANSWER: YES, prices are discounting fast future price appreciation, certainly in stocks, whereas it might be over for housing.

3. THERE IS BROAD BULLISH SENTIMENT

Let’s see, Kudlow states the US economy is crushing it.

Source: CNBC

While consumer confidence is close to record highs.

Source: FRED

Answer: YES, sentiment is bullish! Even with stocks, the sentiment has been extremely greedy in 2018.

Source: CNN

4. PURCHASES ARE BEING FINANCED BY HIGH LEVERAGE

This is not in a bubble, consumer credit is just 50% higher than where it was in 2008 and is just 10 times higher than where it was in 1980. (allow for some irony here)

Source: FRED

As for the stock market, margin debt is at historical highs. Just to mention as a comparative note, margin debt was $263 billion in February of 2010 and $314 billion in July of 2008.

Source: FINRA

Answer: YES, purchases are increasingly being financed by debt.

5. BUYERS HAVE MADE EXTENDED FORWARD PURCHASES

If we look at the level of business inventories, those are 33% higher than in 2008 and I don’t think the economy grew 33% since 2008.

Source: FRED

Answer: a mild yes in this case.

6. NEW BUYERS HAVE ENTERED THE MARKET

Now, the percentage of Americans owning stocks didn’t really go up that much lately as millennials don’t invest that much in stocks.

Source: Gallup

The middle class left after 2008, typical behaviour, buying high and selling low. If we see another bump like in 2007 where the participation jumped from 61% to 65%, we will know it’s a bubble. Those aged 35 and above are investing a bit but not yet like it had been the case.

Source: Gallup

However, not investing in stocks but definitely saving for a house. New buyers are rushing into the home market.

Source: Bloomberg

Answer: with stocks it is a no but with houses it is a yes. Also, it is important to note the widening wealth gap where those that have invest more and push stocks higher while those that don’t have, simply don’t have to invest.

7. STIMULATIVE MONETARY POLICY THREATENS TO INFLATE THE BUBBLE EVEN MORE (and tight policy to cause its popping)

Interest rates have been already tightening and we can expect more in December.

Source: FRED

However, just take a look at historical interest rates.

Source: FRED

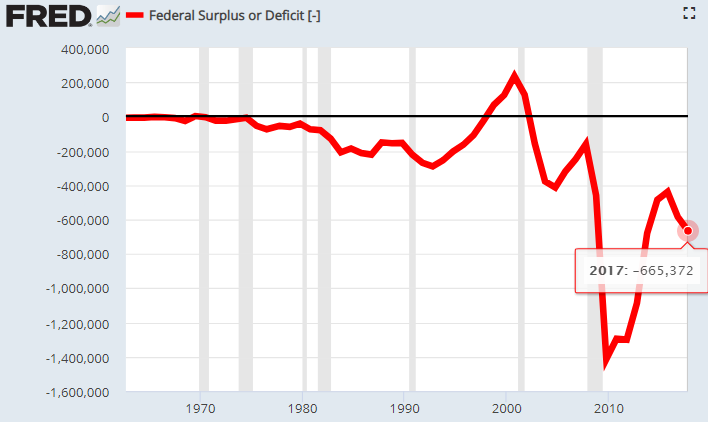

On top of monetary stimulus, there is huge fiscal stimulus.

Source: FRED

On top of the already huge deficit, the deficit is expected to breach $1 trillion in 2019.

So, to summarize on the questions:

WHAT TO DO:

Now, that depends on where you are in your life, about to retire or just starting, but in any case, an all-weather portfolio is the key as we are in the late part of the cycle.

Source: Big Debt Crises

We are at bubble top – so a lot of opportunities to diversify by selling what is in a bubble and buying what is in depression. In a global world you can do that today.

If you wish to check how am I building my portfolio as I cashed out of most my long investments during 2015-to 2018, the last being Nevsun – you might want to check my Stock market research platform where I am slowly building my model portfolio that should do very well in this environment.