Apple Stock: A Comprehensive Look at Its Valuation and Future Prospects

If you want a deep dive into Apple stock, watch the full video about the Magnificent 7 Stocks:

Apple stands as the most valuable company in the world, with a staggering $3.3 trillion market capitalization, surpassing the GDP of nearly every country except the United States and China. Its stock has been a phenomenal wealth creator over the past decade, multiplying in value sixfold since 2019. However, recent performance has raised concerns among investors, with shares down roughly 10% year-to-date amid slowing growth, macroeconomic uncertainty, and questions about the sustainability of its valuation.

This in-depth analysis explores whether Apple remains a worthwhile investment by examining its financial health, growth prospects, valuation, and the risks that could disrupt its trajectory.

Apple’s Financial Health: Strong but Showing Cracks

At first glance, Apple’s financials appear robust. The company generates over $100 billion in annual free cash flow, maintains gross margins above 40%, and has a fortress-like balance sheet with $166 billion in cash and marketable securities. However, a closer look reveals concerning trends.

Slowing Growth in Key Areas

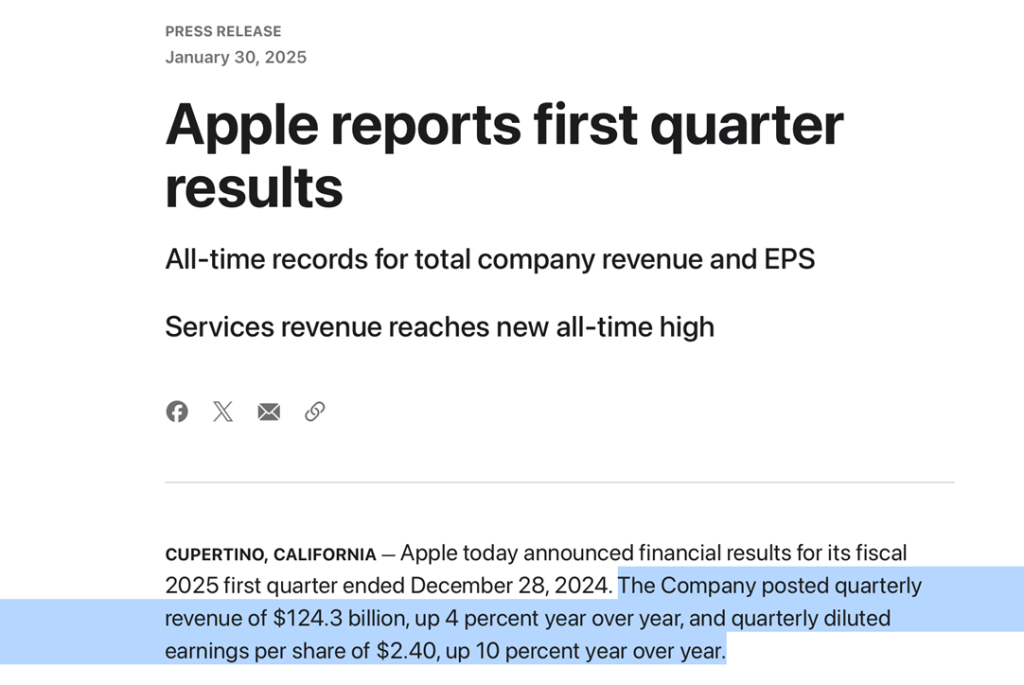

Apple’s revenue growth has decelerated to just 4% year-over-year, a far cry from the double-digit increases seen in previous years. While net income has grown at a healthier 10% clip, much of this improvement stems from aggressive stock buybacks rather than true operational expansion.

The company remains heavily dependent on the iPhone, which still accounts for 55% of total sales. iPhone revenue has been declining, particularly in critical markets like China, where competition from Huawei and domestic brands is intensifying. Services—often touted as Apple’s next growth engine—now make up 22% of revenue, but this segment is intrinsically linked to the iPhone ecosystem. If iPhone sales continue to weaken, Services growth could stall as well.

Capital Allocation: Prioritizing Buybacks Over Innovation

Apple’s management has chosen to return nearly all of its excess cash to shareholders through $104 billion in stock buybacks and $15 billion in dividends over the past year. While buybacks have helped prop up earnings per share (EPS), they do little to address the company’s long-term growth challenges.

Critically, Apple is investing only about $10 billion annually in capital expenditures, far less than what tech peers like Microsoft, Google, and Amazon spend on cloud infrastructure and AI development. This raises questions about whether Apple is adequately preparing for the next wave of technological disruption.

Valuation: Is Apple Overpriced?

Apple’s stock currently trades at a price-to-earnings (P/E) ratio of 34, well above its five-year average of around 20. This premium valuation suggests investors are pricing in significant future growth, but the company’s fundamentals don’t fully support that optimism.

Discounted Cash Flow Analysis: A Reality Check

To assess whether Apple’s stock is fairly valued, we can use a 10-year discounted cash flow (DCF) model, which estimates the company’s intrinsic value based on projected earnings and cash flows.

Base Case Scenario (Most Likely)

- Earnings growth of 7% annually (in line with recent trends)

- Terminal P/E of 20 (a reasonable long-term multiple)

- Resulting intrinsic value: ~$97 per share

This suggests the stock is overvalued by more than 50% at its current price near $200.

Optimistic Scenario (Aggressive Growth)

- Earnings growth of 12% annually (requiring a major new product or service)

- Terminal P/E of 30 (assuming sustained market enthusiasm)

- Resulting intrinsic value: ~$570 per share

While this scenario offers upside, it depends on Apple successfully reigniting growth—something it hasn’t done in years.

Pessimistic Scenario (Stagnation or Decline)

- No earnings growth (iPhone sales continue to weaken)

- Terminal P/E of 12 (typical for stagnant tech companies)

- Resulting intrinsic value: ~$35 per share

This worst-case scenario highlights the substantial downside risk if Apple fails to adapt.

Probability-Weighted Fair Value Estimate

Assigning a 70% probability to the base case, 15% to the optimistic case, and 15% to the pessimistic case, we arrive at a fair value estimate between $90 and $100 per share—far below today’s price.

Key Risks That Could Derail Apple’s Stock

1. iPhone Dependency and Market Saturation

The smartphone market is mature, with global shipments declining in recent years. Apple’s ability to raise prices has helped mask unit sales weakness, but this strategy may have limits. If iPhone revenue continues to shrink, the company’s overall growth will suffer.

2. Economic Downturn and Consumer Weakness

The U.S. has avoided a major recession for over 15 years, an unusually long expansion. If consumer spending weakens, Apple’s premium-priced products could see disproportionate demand destruction.

3. Regulatory and Antitrust Pressures

Apple faces increasing scrutiny from regulators worldwide, particularly over its App Store policies. The EU’s Digital Markets Act (DMA) is already forcing Apple to open its ecosystem to third-party app stores, potentially eroding its lucrative services revenue.

4. Lagging in AI and Innovation

While rivals like Microsoft, Google, and Meta are investing heavily in AI, Apple has been slow to articulate a clear strategy. Its recently announced “Apple Intelligence” features are a step forward, but the company risks falling behind in what may be the most transformative tech trend of the decade.

5. Geopolitical Risks in China

China accounts for nearly 20% of Apple’s revenue, and the company relies heavily on Chinese manufacturing. Rising tensions between the U.S. and China—along with increasing competition from Huawei—pose a serious threat to Apple’s business in the region.

Historical Perspective: Apple as a Value Play vs. Today

Back in 2016, Apple traded at a P/E ratio of just 9, with a free cash flow yield approaching 8%. At that time, the stock was a clear bargain, offering both growth potential and a margin of safety.

Today, the situation is reversed. Apple’s valuation is stretched, its growth is slowing, and its dependence on buybacks to sustain EPS increases is unsustainable in the long run.

Investment Outlook: Proceed with Caution

Given Apple’s high valuation, slowing growth, and mounting risks, the stock appears overpriced at current levels. While the company’s brand strength and ecosystem loyalty provide some downside protection, the risk/reward balance is unfavorable.

Potential Strategies for Investors

- Wait for a Better Entry Point: A pullback to $120 or below (P/E of ~20) would offer a more attractive risk/reward setup.

- Consider Alternatives: With 10-year Treasury yields near 4.2%, risk-free bonds now offer better income than Apple’s <0.5% dividend yield.

- Monitor Innovation Efforts: If Apple demonstrates meaningful progress in AI, wearables, or augmented reality, the growth narrative could improve.

Final Verdict

Apple remains a high-quality company, but at today’s prices, it’s a high-risk, low-reward investment. Prudent investors should avoid chasing the stock here and wait for either a significant price correction or evidence of renewed growth.

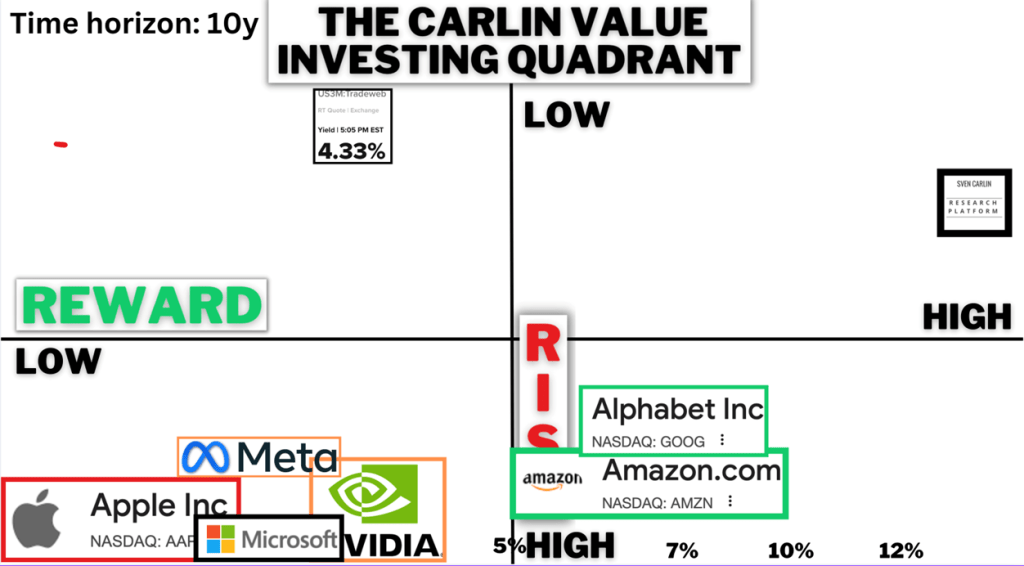

Value Investing Risk & Reward Quadrant (check all the stock analyses)