Analyzing the Growth Potential of Vital Farms: A Small-Cap, Organic Egg Producer

In recent months, egg prices have become a hot topic among investors and consumers alike. Amidst this discussion, one company has caught the attention of market participants: Vital Farms, a small-cap, high-growth organic egg producer. With a unique business model centered around pasture-raised, organic eggs, and sustainable farming practices, Vital Farms has positioned itself as a leader in the growing demand for ethically sourced food products. However, as with any investment, there are both opportunities and risks to consider.

If you want a more in depth analysis of Vital Farms, check out the full video I made here:

The Business Model: Sustainable and Scalable

Vital Farms operates on a conscious, sustainable, and community-oriented model, which aligns perfectly with current consumer trends favoring organic and ethically produced food. The company partners with local farmers to produce pasture-raised eggs, butter, and other dairy products, distributing them across the United States through major retailers like Whole Foods and Kroger.

The company’s growth trajectory has been impressive. Over the past seven years, Vital Farms has consistently expanded its product offerings and distribution network. Currently, the company produces approximately six million eggs per day, a significant figure that underscores its scale. Additionally, Vital Farms is investing in new equipment upgrades, such as MOBA egg processing technology, to further enhance efficiency and production capacity.

Financial Performance: Strong Growth and Positive Cash Flows

From a financial perspective, Vital Farms has delivered robust results. The company is guiding for 22% growth in EBITDA and expects to generate positive cash flows by 2027. With a revenue target of $1 billion and the potential to achieve $100 million in free cash flow, Vital Farms could offer a free cash flow yield of 10%, making it an attractive investment for growth-oriented investors.

The company’s balance sheet is also strong, with no debt and $359 million in assets. This financial stability allows Vital Farms to fund its expansion plans internally, reducing reliance on external financing. Gross margins have improved slightly due to higher egg prices, and operating income has grown as the company scales its operations.

Valuation and Market Potential

At a price-to-earnings (P/E) ratio of 26, Vital Farms is priced for growth, reflecting expectations of 20-30% annual growth in the coming years. Compared to its peers in the food industry, the stock appears relatively cheap, especially given its strong cash flows and scalable business model. If the company continues to execute its growth strategy, it could reach a $2 billion market cap within a few years, further justifying its premium valuation.

Risks and Challenges

Despite its promising outlook, Vital Farms is not without risks. The company relies heavily on a single packaging and washing facility, though it is expanding to a second location. Commodity price volatility, particularly in egg prices, poses another challenge. While Vital Farms has long-term contracts that mitigate some of this risk, fluctuations in input costs could impact profitability.

Competition is also a concern. As the demand for organic and sustainable food grows, new entrants could disrupt the market. Additionally, the company’s reliance on a network of small farms introduces operational complexities, such as land management and avian flu risks. While Vital Farms has reported zero outbreaks of avian flu to date, this remains a potential threat.

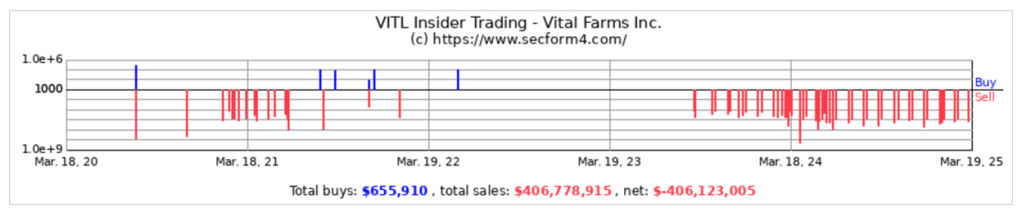

Insider Selling: A Red Flag?

One notable concern is the significant level of insider selling. Over the past year and a half, insiders have sold approximately $406 million worth of stock, representing about 30% of the company. This includes sales by the CEO, CFO, and other executives. While some of this activity can be attributed to stock-based compensation and vesting schedules, the scale of selling raises questions about management’s confidence in the company’s near-term prospects.

The timing of these sales coincides with a surge in egg prices and the company’s stock price, suggesting that insiders may view the current market conditions as cyclical rather than sustainable. This behavior could indicate that the recent boom in egg prices is temporary, and growth may slow in the future.

Conclusion: A Wait-and-See Approach

Vital Farms presents an intriguing investment opportunity, combining a strong business model, sustainable practices, and impressive financial performance. However, the significant insider selling and cyclical nature of egg prices suggest that the current valuation may already reflect much of the company’s near-term growth potential.

For investors, a wait-and-see approach may be prudent. If egg prices normalize and the stock experiences a pullback, it could offer a more attractive entry point. In the meantime, monitoring the company’s execution, competitive positioning, and management’s actions will be key to determining its long-term investment potential.

As always, thorough research and a disciplined investment strategy are essential when evaluating high-growth, small-cap stocks like Vital Farms. While the company’s future looks promising, patience and careful analysis will be critical to capitalizing on its growth story.

Value Investing Risk & Reward Quadrant (check all the stock analyses)