Amazon Stock: A Comprehensive Analysis of Growth Trajectory and Investment Considerations

If you want a deep dive into Amazon stock, watch the full video about the Magnificent 7 Stocks:

As one of the most influential companies in the global digital economy, Amazon (NASDAQ: AMZN) presents investors with a fascinating case study in balancing massive growth potential against substantial capital requirements. The e-commerce and cloud computing giant has seen its shares decline approximately 18% from recent highs, prompting important questions about its valuation and future growth prospects. This in-depth analysis examines Amazon’s financial health, strategic investments, competitive positioning, and valuation to help investors make informed decisions.

Financial Performance: Robust Growth Meets Heavy Reinvestment

Amazon’s recent financial results reveal a company in transition, with strong top-line growth accompanied by significant capital expenditures. Revenue continues to expand at a healthy pace, maintaining Amazon’s position as one of the world’s largest companies by sales. More impressively, the company has dramatically improved its profitability metrics in recent quarters. Operating income surged an extraordinary 86% over the past two years, while net income jumped an even more remarkable 95%. These improvements reflect both cost discipline in the core retail business and the ongoing margin expansion in Amazon Web Services (AWS), the company’s cloud computing division.

However, free cash flow tells a more nuanced story, growing just 4% to $38 billion as the company pours money into long-term growth initiatives. This divergence between earnings and cash flow highlights Amazon’s unique position as a company that consistently prioritizes future growth over short-term profitability. The scale of these investments is staggering – Amazon spent $77 billion on capital expenditures last year and is projected to invest over $100 billion in the current year. These figures represent one of the largest corporate investment programs in the world and underscore Amazon’s ambition to maintain its leadership position across multiple technology sectors.

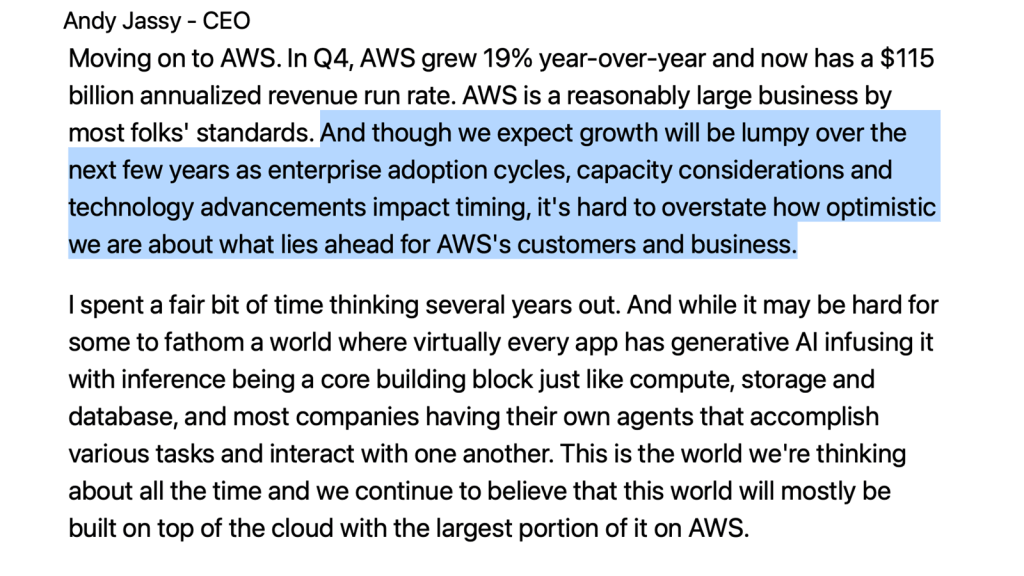

AWS: Cloud Dominance Facing New Challenges

Amazon Web Services remains the crown jewel of Amazon’s business portfolio, generating industry-leading margins and serving as the primary profit engine for the entire company. However, recent commentary from CEO Andy Jassy about “lumpy” growth suggests that even this powerhouse division faces challenges in the current environment. Several factors are contributing to this dynamic:

First, enterprise customers across various industries have become more cautious with their cloud spending amid economic uncertainty. Many organizations are optimizing their existing cloud usage rather than expanding their footprints, which temporarily slows growth for cloud providers. Second, competition in the cloud space has intensified significantly, with Microsoft Azure and Google Cloud both gaining traction, particularly in artificial intelligence workloads. Third, the rapid evolution of AI technology is causing some customers to pause decisions as they evaluate which platforms and partners will best serve their future needs.

Despite these near-term challenges, AWS maintains several structural advantages. Its first-mover position in cloud computing has created a vast installed base of enterprise customers with significant switching costs. The division’s operating margins, while down from their peak, remain exceptionally strong at around 30%. Furthermore, AWS continues to innovate, particularly in AI infrastructure and services, positioning itself for the next wave of cloud adoption.

The AI Imperative: Amazon’s Massive Bet on the Future

Amazon is making an enormous bet on artificial intelligence, committing unprecedented resources to ensure it remains at the forefront of this technological revolution. The company’s AI strategy is multifaceted, spanning hardware, software, and infrastructure:

On the hardware front, Amazon is developing its own AI chips (Trainium and Inferentia) to reduce reliance on NVIDIA’s expensive GPUs. This move could significantly lower costs for both Amazon and its cloud customers while giving the company more control over its technology stack. In software, Amazon Bedrock provides enterprises with access to multiple foundation models, including Amazon’s own Titan models as well as offerings from AI startups like Anthropic. This “model as a service” approach aims to make AWS the preferred platform for companies building AI applications.

The most visible aspect of Amazon’s AI investment is its data center expansion. The company is building massive AI-optimized data centers across the globe, with plans to spend over $100 billion annually on this infrastructure buildout. These facilities will house the computing power needed to train and run increasingly sophisticated AI models. While this investment is enormous, it reflects Amazon’s belief that AI will drive the next wave of cloud adoption and digital transformation across industries.

Valuation Analysis: Growth Priced to Perfection?

Amazon’s current valuation presents investors with a complex puzzle. At a $2 trillion market capitalization and a P/E ratio of 35, the stock prices in significant future growth. A detailed discounted cash flow analysis reveals several possible scenarios:

In a base case scenario assuming 8% annual growth and a terminal multiple of 20x, Amazon’s intrinsic value would be approximately $1.2 trillion – significantly below its current market cap. This scenario would imply substantial downside risk for current investors. A more optimistic bull case, incorporating 12% growth and a 25x terminal multiple, brings the valuation closer to today’s levels, suggesting the stock is fairly valued if Amazon can meet these ambitious growth targets. However, a bear case with just 5% growth and a 15x multiple yields an intrinsic value of $700-800 billion, highlighting the potential downside if growth disappoints.

Several factors complicate the valuation picture. Amazon’s free cash flow yield stands at just 1.8%, well below the risk-free rate offered by 10-year Treasury bonds. The company continues to dilute shareholders, adding about 100 million shares (worth approximately $20 billion) last year alone. Most importantly, much of Amazon’s valuation depends on the success of its AI investments, which remain unproven at scale.

Competitive Advantages and Moat Assessment

Despite these valuation concerns, Amazon possesses several enduring competitive advantages that support its long-term investment case:

In e-commerce, Amazon’s scale is unmatched. The company commands roughly 40% of the U.S. e-commerce market, a position reinforced by its Prime membership program and vast logistics network. This dominance creates a virtuous cycle where more sellers attract more buyers, which in turn attracts more sellers. Amazon’s advertising business, while smaller than competitors like Google and Meta, is growing rapidly at over 20% annually and benefits from the company’s unique access to shopping intent data.

AWS provides perhaps Amazon’s widest moat. As the first major cloud provider, AWS developed capabilities and customer relationships that competitors still struggle to match. The division’s profitability funds much of Amazon’s innovation while providing a platform for new services like AI tools and industry-specific cloud solutions.

Investment Outlook and Strategic Considerations

Given this comprehensive analysis, Amazon presents investors with both significant opportunities and notable risks:

For long-term investors, Amazon remains one of the most compelling growth stories in the market. The company operates in large, expanding markets and has demonstrated an unparalleled ability to innovate and dominate new sectors. Management’s willingness to invest aggressively in future opportunities, even at the expense of short-term profits, has historically created tremendous shareholder value.

However, at current valuations, much of this potential appears already priced into the stock. Investors are effectively paying for perfect execution of Amazon’s AI strategy and continued dominance across its business lines. Any stumbles in AI adoption, cloud growth, or retail profitability could lead to significant multiple compression.

Conclusion: A Cautious Approach to a High-Quality Business

Amazon stands as one of the most impressive business success stories of the digital age. Its transformation from online bookseller to global e-commerce and cloud computing leader demonstrates extraordinary vision and execution. The company’s current investments in AI position it well for the next phase of technological evolution.

However, even the strongest businesses can become overvalued. At current levels, Amazon’s stock appears to discount nearly perfect execution of its ambitious growth strategy. While the company may well deliver on these expectations, the risk/reward profile appears balanced at best.

Investors would be wise to maintain exposure to this exceptional company but remain disciplined about valuation. In the volatile world of growth investing, patience and selectivity often prove more valuable than enthusiasm. Amazon will likely remain a dominant force for years to come, but the optimal time to increase exposure may lie ahead rather than at current elevated levels.

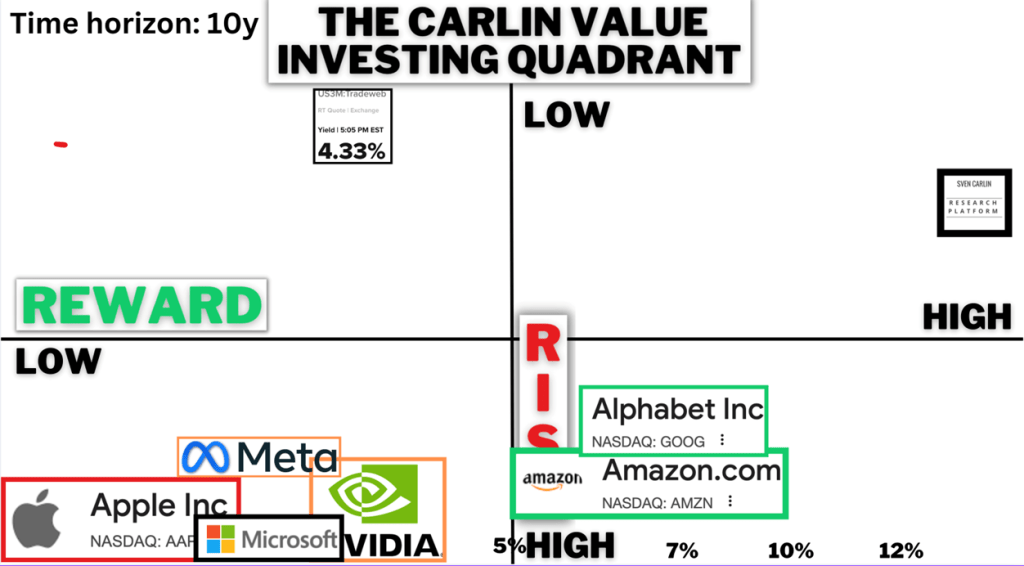

Value Investing Risk & Reward Quadrant (check all the stock analyses)