Allison Transmission Stock Analysis – A good business with a 12 FCF yield

Alisson Transmission stock analysis summary:

- Free cash flow yield is 12.9%. Likely to change short term but attractive longer term.

- Apart from the coming recession, the other cloud over the business is the EV threat.

- The buybacks are likely to be cut, the debt is relatively high but the business will not go away that fast.

Allison Transmission stock analysis

Allison Transmission stock (ALSN) is the world’s largest manufacturer of fully automatic transmissions for medium- and heavy-duty commercial vehicles and is a leader in hybrid-propulsion systems for city buses. The company was owned by GM for a long time and The Carlyle acquired it in 2007 for $5.6 billion. It went public in 2012.

Source : ALST history

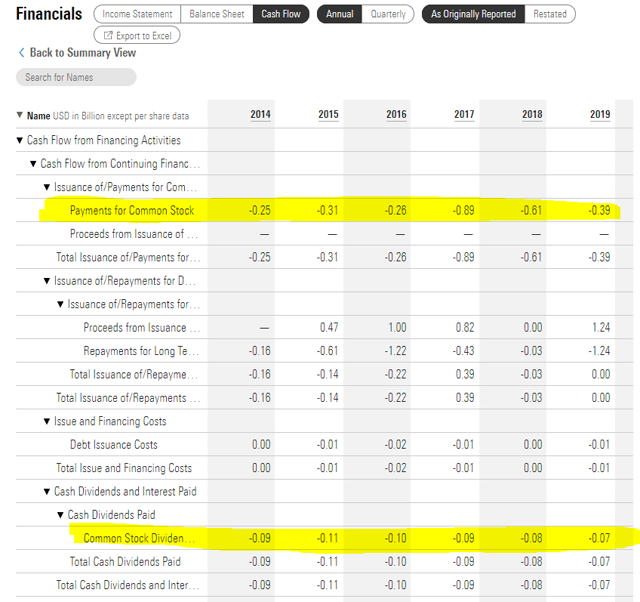

The Free Lunch Portfolio defines it as an uber cannibal stock. A look at ALSN’s cash flow shows it spent $2.71 billion on buybacks over the last 6 years. It spent on average about $90 million for dividends per year. The number of shares outstanding has declined from 188 million in 2013 to the last reported, 123 million.

ALSN Stock Analysis – Cash Flow – Source: Morningstar

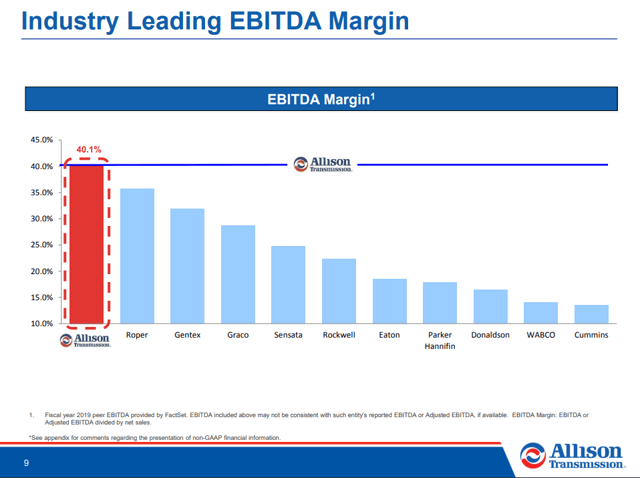

Such heavy spending is possible because the company has pretty good margins on its products.

ALSN Stock Analysis – EBITDA Margin – Source: Allison Transmission IR

Having good margins also means you have an advantage over other producers which indicates business quality – always a good thing to invest in. Good margins lead to high free cash flows and a high return on capital.

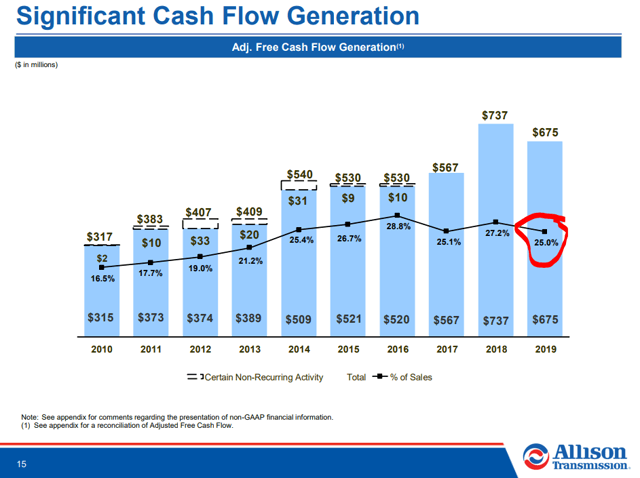

Allison Stock Analysis – Free cash flow – Source: Allison Transmission IR

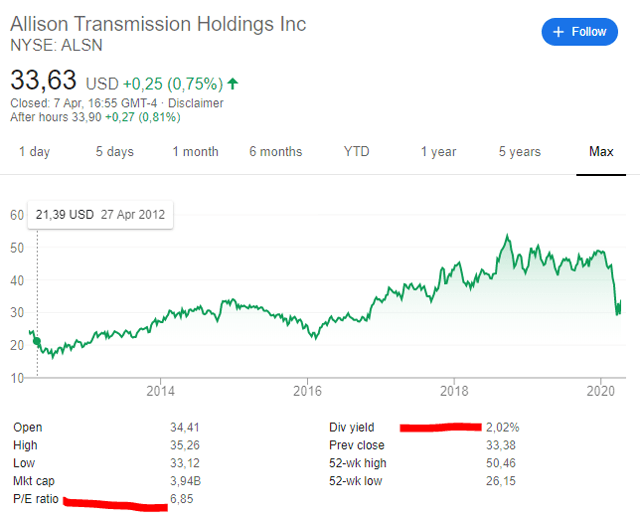

On the current market capitalization of $3.94 billion, average free cash flows of $509 million per year over the last 10 years indicate to a free cash return of 12.9%.

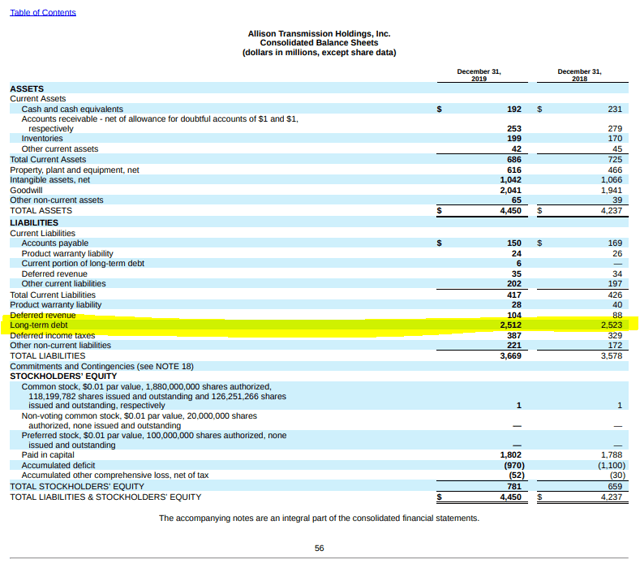

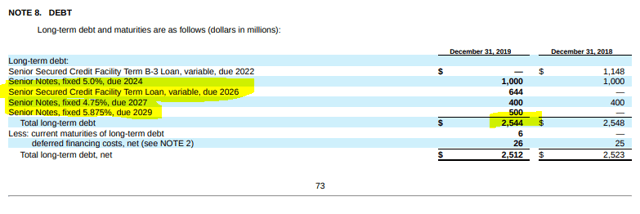

I always like to look at the debt structure of a company and they have a significant amount of it, $2.5 billion. In case of deteriorating cash flows, the debt will become a bigger and bigger issue.

Allison Transmission Stock Analysis – Balance Sheet – Source:10K

They still have two years to refinance the $1 billion loan, but the cost of it will depend on the business environment for the company.

We have now discussed the past for ALSN, and it looks really good. However, it is time to discuss the future because investing is about the future, unfortunately not about the past – that would make things too easy.

Allison Transmission stock analysis – outlook

For me, categorizing a stock into the 6 categories discussed in Peter Lynch’s book One Up On Wall Street makes it much easier to know what to expect from a potential investment.

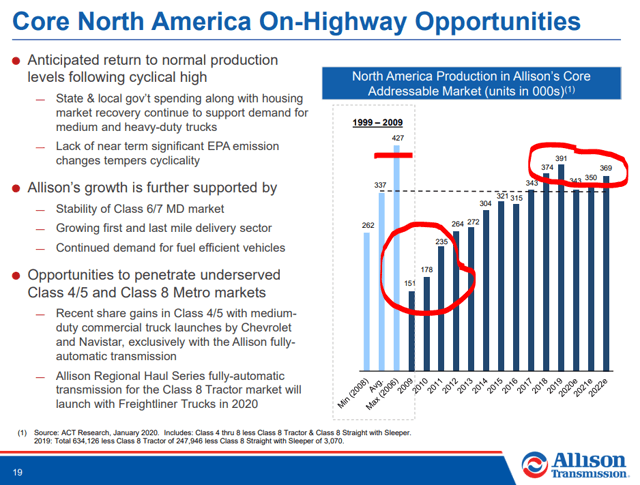

I would categorize ALSN’s business as cyclical. Demand for its products depends on economic activity, interest rates and the general sentiment. ALSN’s market might be less cyclical than the Linehaul Class 8 market but it is still cyclical.

In 2009, the market fell 65% compared to the average of the previous 3 years and it took 6 years to recover to the previous long-term average as it never reached the previous cyclical highs.

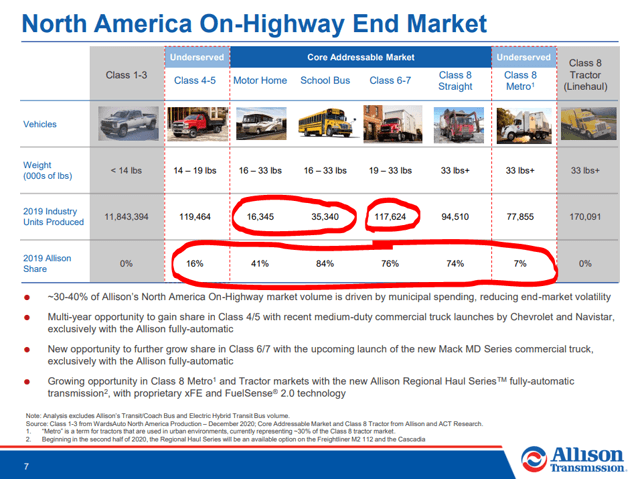

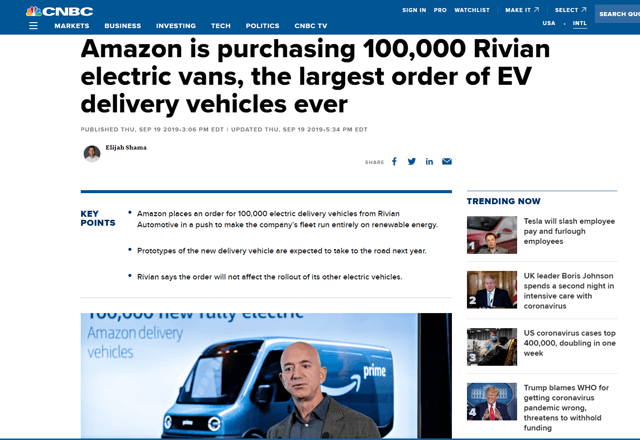

The question is, will there be more market growth or is it a market destined for a slow, but long structural decline due to the EV danger?

ALSN’s market threat – Source: CNBC

However, they have two growth opportunities out there. One is to expand globally as they are doing by opening factories in Hungary and India.

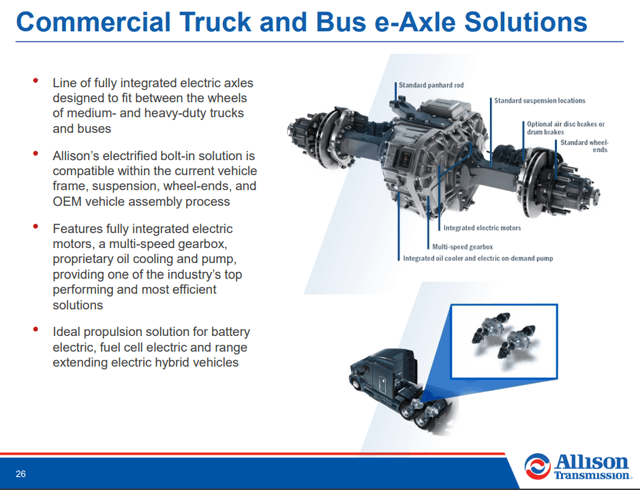

The second growth opportunity comes from the hybrid business and new potential EV business. However, that is an area with high competition and they will likely not have the advantages they have in the traditional business thanks to their GM heritage.

ALSN STOCK – Investment conclusion

The conclusion is simple. ALSN is a cyclical stock and the best time, the lower risk and higher reward investment opportunity with such businesses, is when the fundamentals start to improve, not heading into a recession.

Secondly, one must carefully watch the EV threat as it is really becoming fancy to buy an EV garbage truck. Maybe it is not feasible now, but going into the second part of this decade, there will be much more supply at lower prices where we don’t know how will ALSN fare in that environment.

On a cash flow basis, the company is also still a bit expensive because we can expect it to see slow or even negative growth over the coming decade. On top of that the company has $2.5 billion in debt that will become a burden at some point in time (it always does in a cyclical industry).

Despite my cloudy outlook, I would say that if someone follows the company over the next decade, carefully assesses the technology, he or she might buy just before ALSN gets to a breakthrough. The positive situation might never materialize, but it might be worth to follow.

If you enjoyed this analysis, please subscribe to the newsletter to get all the Free Lunch Portfolio Analyses in your inbox.