Aker BP: A Compelling Case for Income Investors Seeking Stability in the Volatile Oil Sector

You can watch the full video discussing Aker BP here:

The global energy landscape remains as unpredictable as ever, with oil prices fluctuating amid geopolitical tensions, demand uncertainties, and the ongoing energy transition. In such an environment, investors seeking exposure to the oil sector while prioritizing stable income would do well to examine Aker BP (OTCMKTS: AKRBF), the Norwegian oil producer that combines an exceptionally robust business model with one of the most attractive dividend profiles in the industry.

Unrivaled Cost Efficiency: The Foundation of Aker BP’s Strength

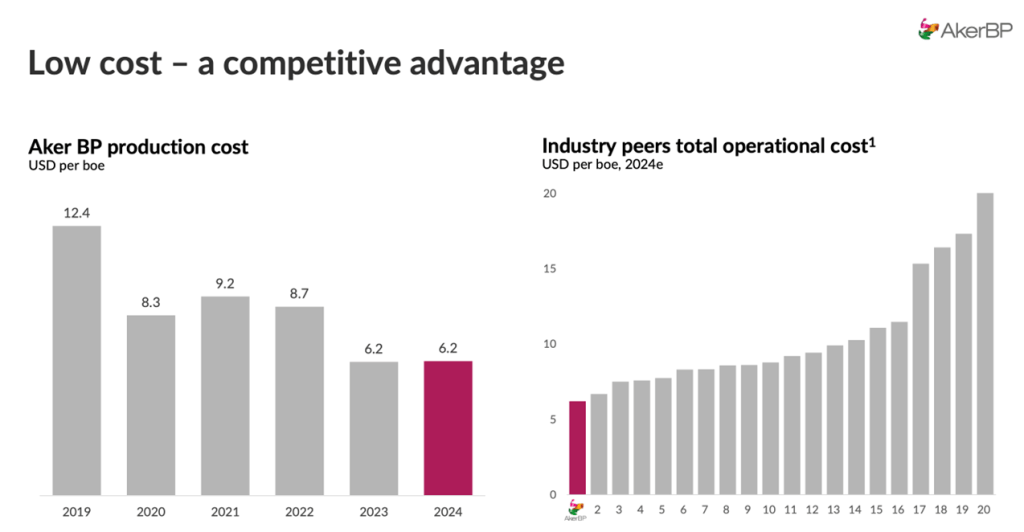

At the heart of Aker BP’s investment proposition lies its industry-leading cost structure. With production costs averaging just $6 per barrel, the company operates at a significant advantage compared to both shale producers and international oil majors. This remarkably low cost base provides Aker BP with unparalleled resilience against oil price downturns. Even in a scenario where Brent crude were to fall to $40 per barrel, the company would remain comfortably profitable—a stark contrast to many U.S. shale operators that require prices above $50-$60 just to break even.

This cost advantage stems from several factors:

- High-quality Norwegian offshore assets with long reserve lives and stable production profiles

- Operational efficiencies gained through consolidation (notably the merger with Lundin Energy’s E&P business)

- Favorable fiscal terms from operating in Norway’s stable regulatory environment

Dividend Sustainability: A Rare Combination of High Yield and Growth

What truly sets Aker BP apart is its exceptional dividend policy. The company currently offers investors a 10.7% dividend yield—among the highest in the European energy sector—with a commitment to growing this payout by at least 5% annually as long as oil prices remain above $40 per barrel.

This dividend is underpinned by:

- Strong cash flow visibility: Even at conservative oil price assumptions ($65/bbl), Aker BP is positioned to generate $8 billion in cumulative free cash flow over the next five years—more than 50% of its current market capitalization.

- Conservative balance sheet: With net debt of just $4 billion (after accounting for $3 billion in cash) and leverage ratios that remain below 0.5x at $65 oil, the company has ample financial flexibility.

- Built-in downside protection: Stress tests show the dividend remains secure even if oil prices were to decline to $50, with leverage staying below 1.5x in such scenarios.

The Norwegian Context: High Taxes But Predictable Returns

While Norway’s 78% tax rate on oil profits might initially appear prohibitive, this needs to be understood in context:

- Tax incentives for reinvestment allow deferral of tax payments when funds are plowed back into production growth

- The high-tax regime ensures political stability, reducing risk of arbitrary fiscal changes that plague other oil jurisdictions

- The 25% dividend withholding tax (which may be reduced for international investors depending on tax treaties) is already factored into the attractive yield

Importantly, these fiscal terms haven’t prevented Aker BP from delivering consistent returns to shareholders, with the dividend having grown steadily since its inception.

Valuation Perspective: Margin of Safety Present

At current levels around NOK 220 per share, Aker BP appears undervalued on several metrics:

- Conservative DCF analysis (assuming just 5% dividend growth and a 10% required return) suggests fair value around NOK 300—36% upside from current levels

- In more bullish oil price scenarios ($90/bbl), the valuation could approach NOK 400

- Even in a no-growth scenario where the dividend remains flat indefinitely, the stock would still be fairly valued at current prices

This valuation disconnect likely reflects:

- General aversion to European energy stocks amid the energy transition narrative

- Overestimation of political risk (despite Norway’s stability)

- Lack of analyst coverage compared to larger international peers

Strategic Advantages Over Other Oil Investments

When compared to other oil investment options, Aker BP’s advantages become clear:

Versus U.S. Shale Producers

- Lower breakevens ($40 vs $50+)

- More predictable decline curves (offshore vs shale’s steep declines)

- Superior dividend yields (10%+ vs minimal or no dividends from most shale players)

Versus International Majors

- Pure-play upstream exposure without downstream/transition business drag

- Higher yield than most majors (BP, Shell, etc. typically yield 4-5%)

- More disciplined capital allocation focused on shareholder returns

Versus Other High-Yield Oil Plays

- Lower geopolitical risk than Petrobras (Brazil) or Rosneft (Russia)

- Stronger balance sheet than many high-yield E&Ps

- Transparent dividend policy unlike many variable dividend schemes

Why Dividends Trump Buybacks in the Current Environment

Aker BP’s dividend-focused approach contrasts favorably with many peers prioritizing buybacks. In today’s uncertain energy markets, dividends offer several advantages:

- Guaranteed returns regardless of oil price volatility

- Protection against value-destructive buybacks at cyclical peaks

- Flexibility to reinvest dividends elsewhere as market conditions change

This is particularly important given the wide range of potential energy futures, from scenarios where oil demand remains robust for decades to more aggressive energy transition outcomes.

Potential Risks to Monitor

While Aker BP presents a compelling case, investors should remain aware of:

- Long-term oil demand uncertainty from electrification and substitution

- Norwegian fiscal policy changes, though historically stable

- Operational risks inherent in offshore production

- Currency exposure to NOK fluctuations

However, these risks appear more than priced in at current valuations.

Conclusion: A Rare Combination of Yield and Quality

Aker BP represents that rare find in today’s markets—a high-yield investment that doesn’t require compromising on business quality or sustainability. With its:

- Best-in-class cost structure

- Secure and growing dividend

- Strong balance sheet

- Conservative valuation

The stock offers both income and potential capital appreciation, making it particularly attractive for:

- Income-focused investors seeking stable high yields

- Value investors looking for misunderstood opportunities

- Energy investors wanting low-risk oil exposure

In an investment landscape where safe yields remain scarce, Aker BP stands out as a well-kept secret in the North Sea—one that deserves closer attention from discerning investors.