Aalberts NV Stock Analysis – Interesting Business Compounder

This Aalberts stock analysis is part of my full, stock by stock, analysis of the Amsterdam stock exchange. There you have the list of analyzed stocks and if you wish to receive email updates on stock analyses, please subscribe to my newsletter:

Aalberts stock analysis summary:

- Just EUR 5 billion market capitalization on interesting niche business growth.

- Exposed to water, flow measurements, piping etc.

- Growth strategy organic and M&A, usually a good thing with niche businesses.

- Maybe high now, but is often volatile due to business cycles, then is the time to watch it.

- Can it be a 10 bagger? Yes, but more likely from the 20 EUR starting point we had in March 2020. To watch.

AALBERTS NV Stock Price Analysis – AMS: AALB

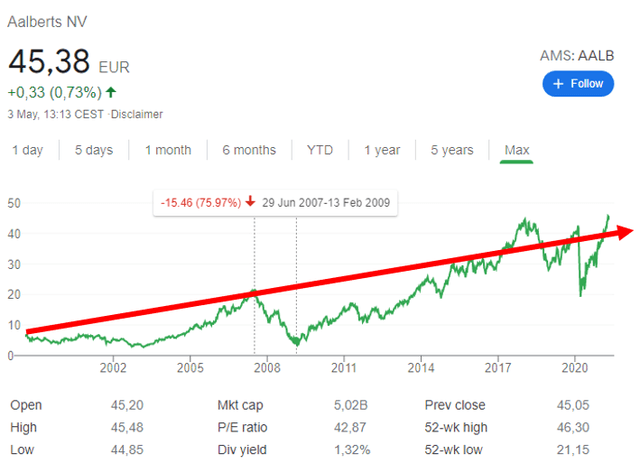

Aalberts stock price (AMS: AALB) looks promising because when you see a long-term stock price chart that goes up, it is the first sign of a good business. The market cap is still just 5 billion EUR which means there is plenty of room for growth.

However, the above chart also indicates the high volatility of the stock price. From 2007 to 2009 the stock crashed 75%, 30% in 2018 and more than 50% in the COVID flash crash of 2020.

The key to deal with such volatile stocks is to know the business well and understand it in depth. That is what will allow to strike when the market gives an amazing opportunity.

It is funny how the stock price actually follows the business development over the long-term, revenues have stagnated since 2015 and so did the stock since 2017. Let’s see if the business can continue to grow as it did in the past through smart acquisitions as it is normal that all business growth comes in cycles. Also, acquisition often take time to create value but in niche businesses it is often smart to do them.

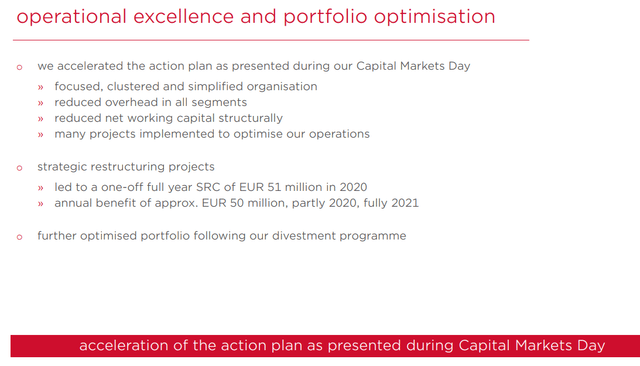

To address the stagnation the company has started a restructuring plan that should lead to net income benefits in 2021.

Let’s take a deeper look into the business.

Aalberts NV Business Overview

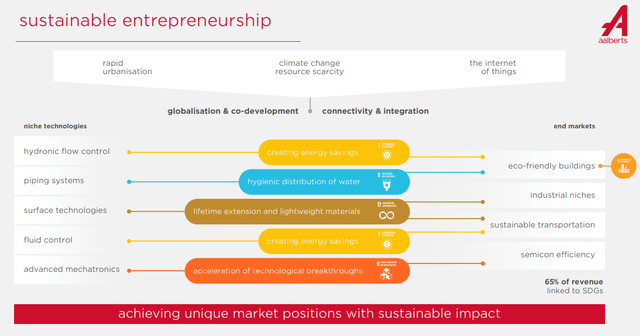

Aalberts is in business of piping systems, surface technologies, hydronic flow control, fluid control and advanced mechatronics.

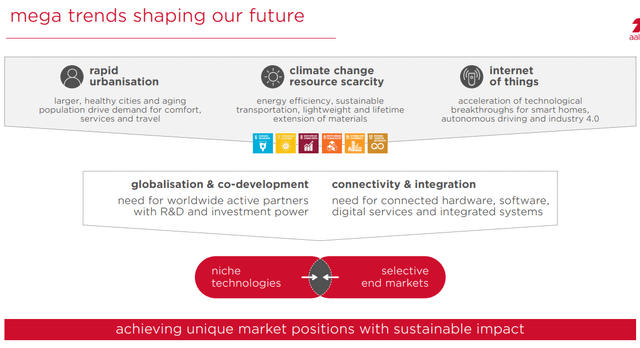

All these sectors are closely related to current megatrends like sustainability, water, ecology, urbanization and low CO2 emissions.

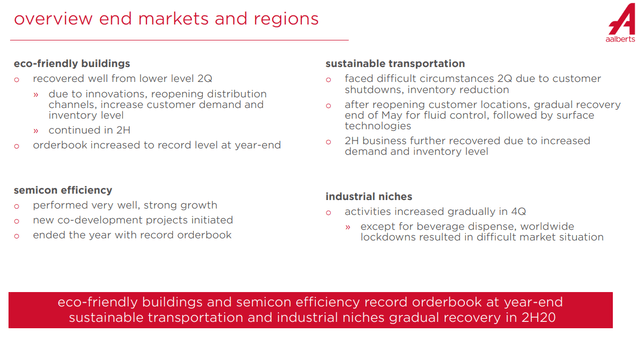

The current business situation seems stable and improving after the COVID-19 pause.

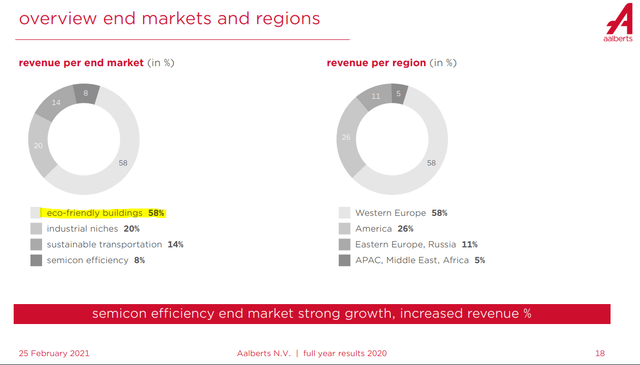

The revenue split is still largely from western Europe with 58% but there is also opportunity abroad as emerging market urbanization is big.

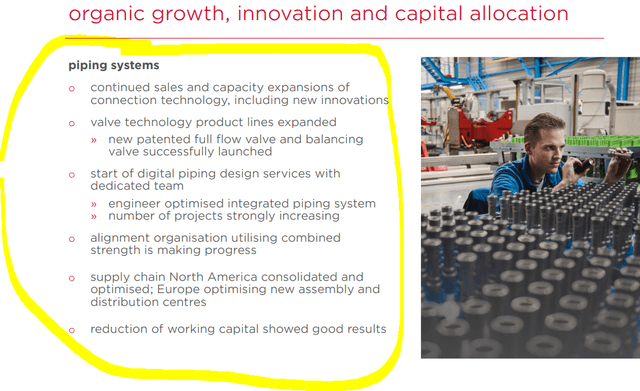

The piping segment looks positive.

Measuring flow, there is a new facility coming.

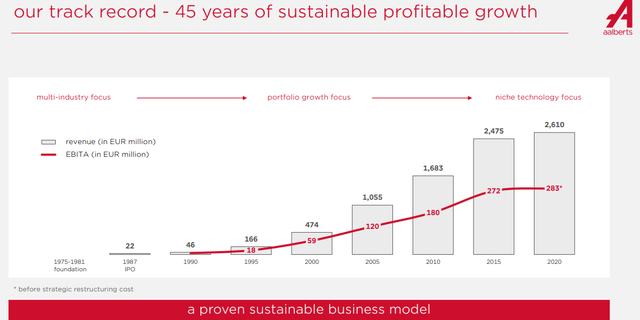

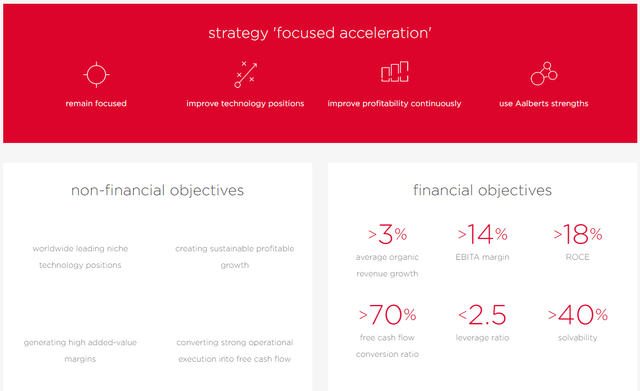

The strategy of the business is in line with the past strategy that did relatively well for investors. They will continue focusing on organic revenue growth but also on acquisitions.

Aalberts stock analysis – business outlook – Source: Aalberts IR 2020 Presentation

All in all, an interesting business is a somewhat boring industry. I don’t think there are many Harward graduates that can’t wait to go into the piping business. But boring industries and boring businesses are where Peter Lynch says we should look for our 10-baggers. Let’s look at the fundamentals and make a valuation.

Aalberts NV Stock Analysis – Fundamentals

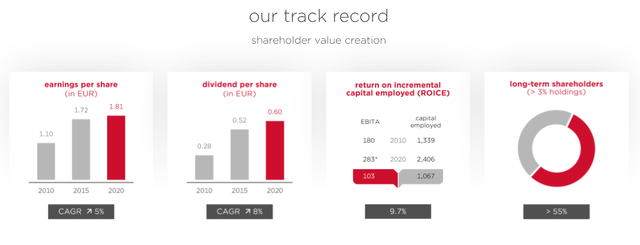

The company did really well over the past, they doubled the dividend over 10 years and if they do it again, that is already good.

Their objective is to have a return on invested capital of above 18%. If they can achieve that over the long-term, then 18% will likely be also the investment return from investing in Aalberts stock, that is how investing works. Of course, it is not easy to achieve ROIC of above 18%, but it makes it interesting to follow.

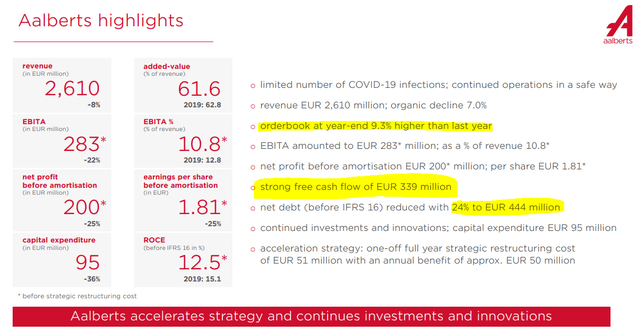

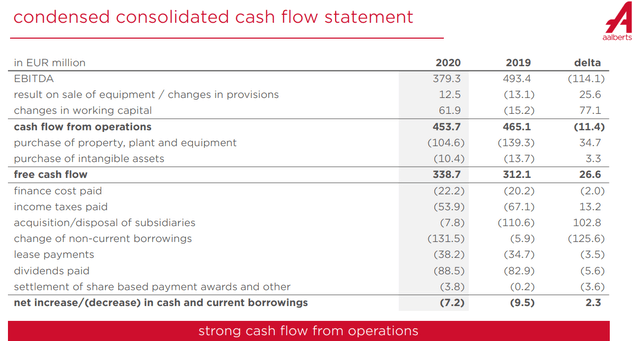

In 2020 revenues have declined as the world was blocked, but the company still made good profits and what is key; free cash flows of 339 million EUR. That leads to a 6.7% free cash flow yield which is not bad for the economic circumstances in 2020. (me and the company have a different way of looking at cash flows – discussed below)

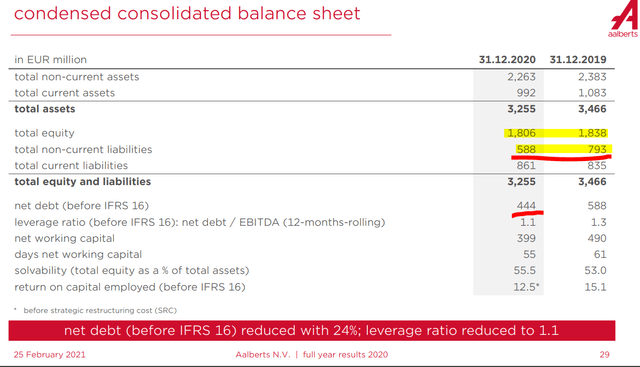

They used that cash flow to lower long-term debt by 200 million and paying a dividend, that is something remarkable and the balance sheet doesn’t looked stretched at all.

If I look at the actual cash flows, they managed to create 222 million EUR for shareholders when we adjust for interest costs, taxes and lease payments. That is a 4.4% yield, but still good considering the 2020 environment.

I feel that in good years these guys can make 300 million EUR in FCF which is something interesting and certainly gives room for dividend payments, especially as they are lowering the debt. When the debt is low, such M&A niche companies usually focus on making a new acquisition, that leads to higher revenue growth and higher dividends down the road.

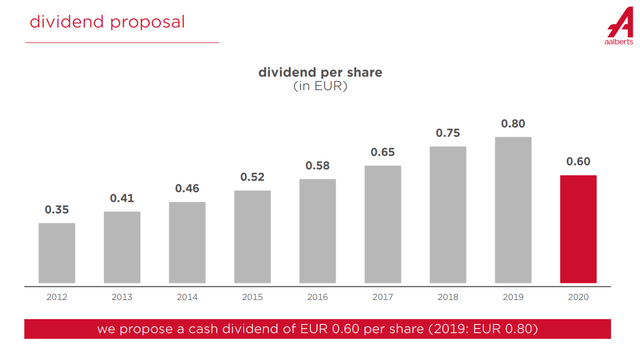

Aalberts Dividend

Aalberts dividend has been steadily growing up till 2020. But when the cash flows return, I would not be surprised in higher dividends in 2021.

I will use the 0.8 EUR dividend as starting basis for my valuation as I think the company will be able to find the approximately 100 million necessary for that. Anyway, from a cash flow perspective, the dividend seems relatively stable, with declines in bad times when the management it seems does things conservatively.

Aalberts NV Stock Valuation – Dividend and cash flow

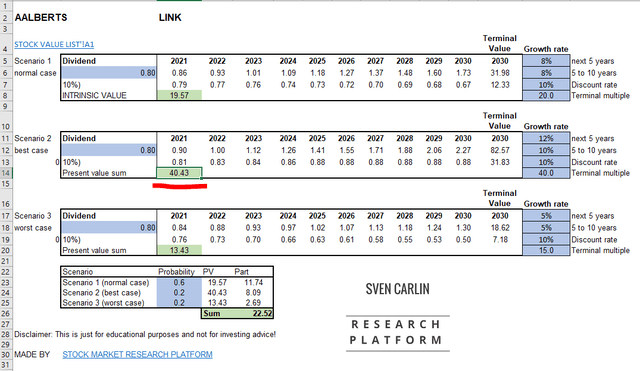

As the dividend is what they give me, I’ll make first a valuation based on that, it keeps things simple and easy but of course isn’t perfect.

The dividend valuation tells me the stock should crash 50% to give me a 10% return and some margin of safety. It might actually happen but the valuation is distorted because of the current low yield. If I apply the current low yield also to the future for AALB, the stock is fairly priced as we can see below in scenario 2.

AALB stock valuation – dividend – Source: Sven Carlin Research Platform

For me it is risky to base my investment on the assumption that the market will still be happy with a dividend yield below 2% by 2030.

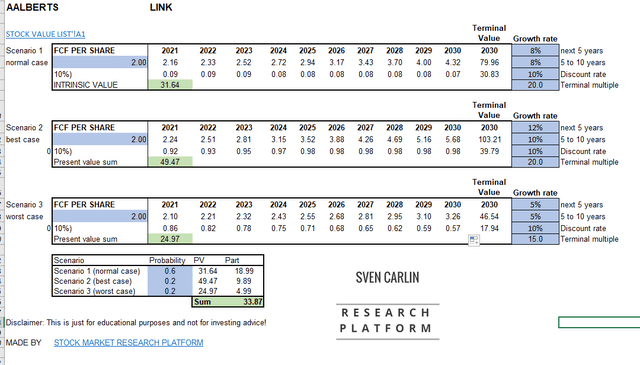

If I apply a free cash flow analysis, the 220 million in FCF amount to approximately 2 EUR per share of FCF. I add up the present value of the dividends by assuming a 45% pay-out ratio.

If FCF growth 8% per year and the terminal multiple on the FCF remains as the current is around 20, the intrinsic value comes to 31.64 EUR.

In the best-case scenario, we get close to 50 EUR, but the growth ahead has to be constantly in the lower teens, year in and year out, which is very hard and, in my view, the current price doesn’t justify the risks.

AALB stock valuation – dividend – Source: Sven Carlin Research Platform

But, if the stock crashes 50%, and we have seen that it is possible for it to happen, this could be an interesting opportunity. It goes on my watch list and then if it ever does reach my conservatively measured intrinsic value, I will take a deeper look.

Aalberts NV Stock Investing Risk & Reward

For now, AALB is a bit exuberantly priced as the stock price reflects my intrinsic value calculation that I get in an exuberant scenario. This means that the upside is limited while the risks are high. It is not a situation I like to be in.

Also, from a business perspective, I am aiming at higher returns than a 1.7% dividend yield. Even if the dividend growth 8% every year, by 2030 my yield on cost would just be 10% which is again risky.

If you enjoyed this analysis, please consider subscribing to my newsletter where I update on stock analyses. If you wish to immediately see the core of my work, check out my Stock Market Research Platform.