Green Brick Partners: A Compelling Value Investment in Homebuilding

Here is the full video discussing Green Brick Partners if you want a more in depth analysis:

The search for undervalued companies with strong growth potential often leads investors to overlooked sectors, and homebuilding is one such area where hidden gems can still be found. Green Brick Partners (NYSE: GRBK), a land developer and homebuilder operating primarily in high-growth Sun Belt markets, stands out as an intriguing opportunity. Founded by hedge fund manager David Einhorn and homebuilding veteran Jim Brickman in the aftermath of the 2008 financial crisis, the company has quietly built a profitable, low-debt business with a disciplined focus on land acquisition and residential construction.

Trading at a remarkably low price-to-earnings (P/E) ratio of 7 while delivering earnings growth of around 30% annually in recent years, Green Brick appears to be a rare combination of value and growth. Yet, as with any investment in a cyclical industry, there are risks to consider—particularly the potential for a housing market downturn. This in-depth analysis will explore Green Brick’s business model, financial strength, growth prospects, and the key factors that could influence its future performance.

Understanding Green Brick’s Business Model

At its core, Green Brick Partners is a land-centric homebuilder. Unlike many competitors that focus primarily on construction, the company places heavy emphasis on acquiring and developing land in strategic locations. This approach provides several advantages:

1. Land as a Strategic Asset

Green Brick owns approximately 40,000 lots across its key markets—Dallas, Atlanta, and Houston—which gives it a significant inventory to support future growth. Given that the company sells around 4,000 homes per year, this represents a 10-year supply, ensuring long-term visibility. Importantly, land is carried on the balance sheet at cost, meaning there may be substantial hidden value if property prices have appreciated since purchase.

2. Focus on High-Growth Markets

The company’s operations are concentrated in some of the fastest-growing metropolitan areas in the U.S. Dallas, Atlanta, and Houston have all seen strong population inflows, driven by job growth, affordability, and migration trends away from higher-cost coastal cities. This demographic tailwind supports sustained demand for new housing.

3. Conservative Financial Structure

One of Green Brick’s most appealing traits is its minimal use of debt. With no net debt and a strong equity base, the company is far less vulnerable to financial stress than many of its peers. This is particularly important in homebuilding, where downturns can quickly strain overleveraged firms.

Financial Performance and Valuation

Green Brick’s financial metrics paint a picture of a company that is both profitable and efficiently managed:

- Revenue and Earnings Growth: The company has consistently grown its top and bottom lines, with net income reaching nearly $400 million in 2023.

- High Return on Equity (ROE): By reinvesting profits into land acquisitions, Green Brick has achieved an ROE of around 15% or higher, a sign of effective capital allocation.

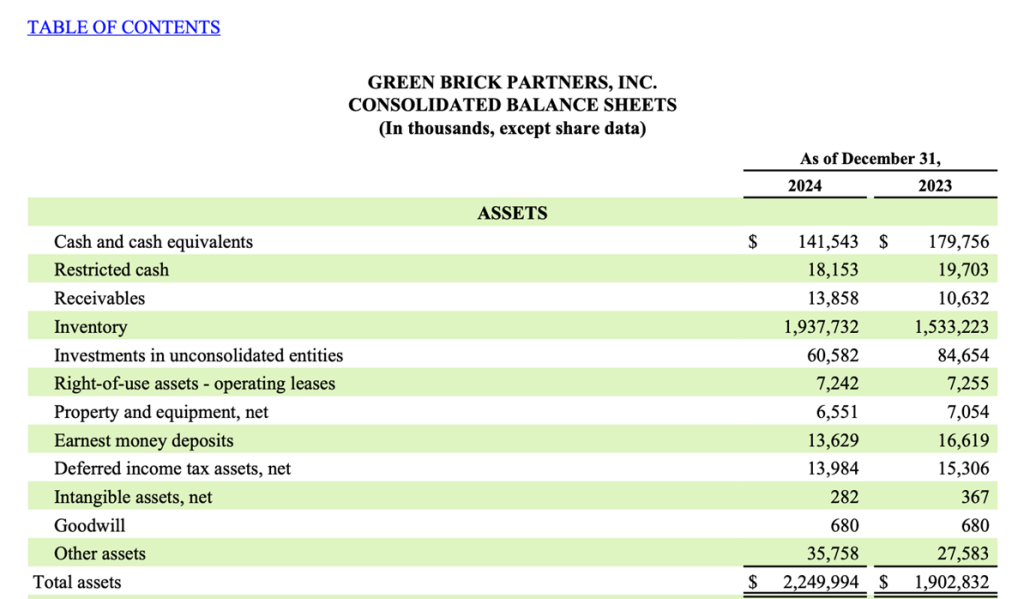

- Strong Balance Sheet: With $1.9 billion in inventory (primarily land) and $1.6 billion in equity, the company’s assets provide a solid margin of safety.

Despite these strengths, the stock trades at a P/E ratio of just 7—a significant discount to both its historical performance and the broader market. This suggests that investors are either underestimating its growth potential or pricing in substantial risks related to the housing cycle.

Potential Catalysts for Shareholder Returns

Given its financial flexibility, Green Brick has multiple avenues to enhance shareholder value:

- Stock Buybacks: Management has indicated that share repurchases could resume in the second half of 2024, providing a potential boost to the stock price.

- Dividend Potential: If the company slows its land acquisitions, excess cash could be returned to shareholders via dividends.

- Hidden Land Appreciation: Since land is carried at cost on the balance sheet, any appreciation in property values could lead to upward revisions in book value.

Key Risks and Challenges

While Green Brick’s fundamentals are strong, no investment is without risks—especially in a sector as cyclical as homebuilding.

1. Housing Market Vulnerability

The U.S. housing market has enjoyed a prolonged period of strength, fueled by low interest rates and strong demand. However, with mortgage rates now hovering around 7%, affordability has become a growing concern. If home prices stagnate or decline, Green Brick’s earnings could come under pressure. Historical precedents—such as the 2008 crash and the early 1990s downturn—serve as reminders of how severe housing corrections can be.

2. Regional Market Concentration

While Dallas, Atlanta, and Houston are thriving today, real estate markets are inherently local. A downturn in any of these areas—whether due to economic weakness, oversupply, or shifting migration patterns—could disproportionately impact Green Brick’s performance.

3. Cyclical Nature of Homebuilding Stocks

Historically, the best time to invest in homebuilders has been during downturns (when earnings are depressed and P/E ratios appear high), while the riskiest time has been during peaks (when earnings are strong and P/E ratios look cheap). Green Brick’s current low P/E may reflect market skepticism about the sustainability of its earnings rather than a true undervaluation.

Investment Outlook: Patience May Yield the Best Opportunity

Green Brick Partners is a well-managed company with a disciplined approach to land acquisition, a strong balance sheet, and exposure to some of the most dynamic housing markets in the country. For long-term investors, it represents a compelling way to gain exposure to the Sun Belt’s growth story while maintaining a margin of safety through its asset-rich structure.

However, given the cyclical nature of the housing market, the most attractive entry point may still lie ahead. If rising mortgage rates or an economic slowdown lead to softer home prices, Green Brick’s stock could become even more appealing. Investors with a value mindset may want to initiate a small position now while keeping powder dry for potential future opportunities.

Value Investing Risk & Reward Quadrant (check all the stock analyses)

v