Latest Canada Pension Fund Investing Strategy

This pension fund investing strategy is for a Canadian customer that asked for my help when it comes to her pension fund investing and the unfortunately limited options she has in her pension plan. This is the list of options she has in her pension fund:

The options are really limited but you have to do what you can with what you have. In order to help with the extremely important pension investing strategy, I did some research, and the more I researched, the more pissed I became as I couldn’t believe what I found.

I became really mad, and this requires immediate government intervention in Canada – the pension fund investment environment has to be changed immediately.

So, call Justin, I hear he is he is a nice guy, so if he cares about his people he will intervene immediately and lower pension fund costs!

THE FEES CHARGED BY PENSION MUTUAL FUNDS ARE OUTRAGEOUS

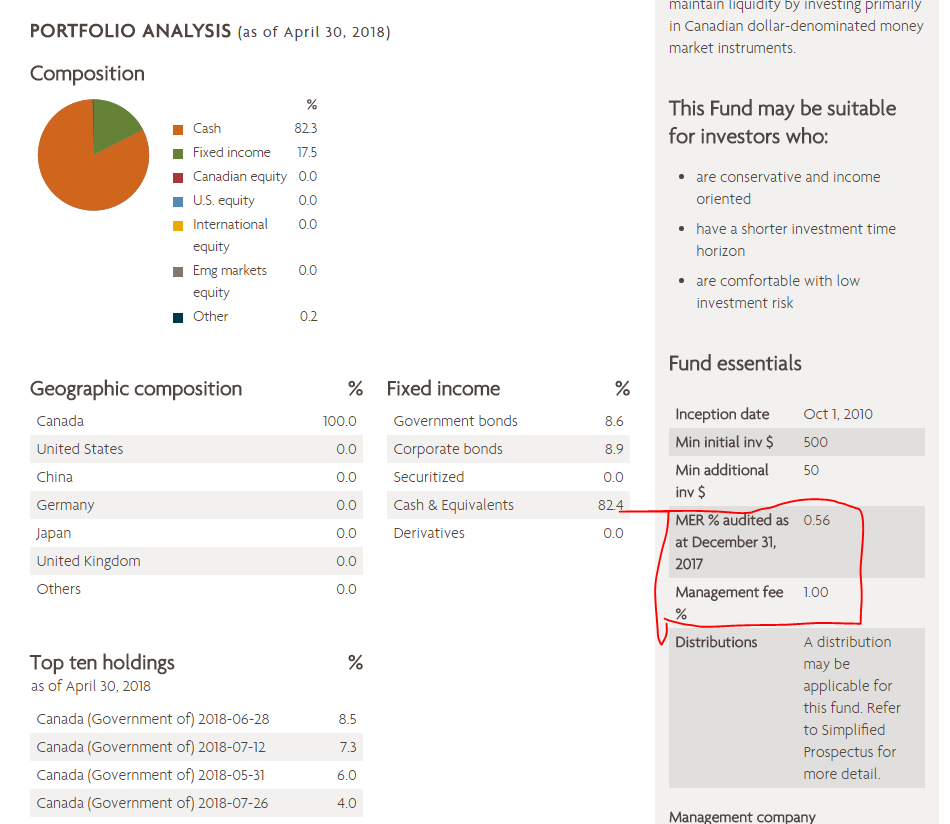

LET’s take a look at the funds and start with the money fund.

The bulk of a mutual fund is invested in cash and the management fee is 1%. The management expense ratio is at 0.56% but strange that it is below the fee.

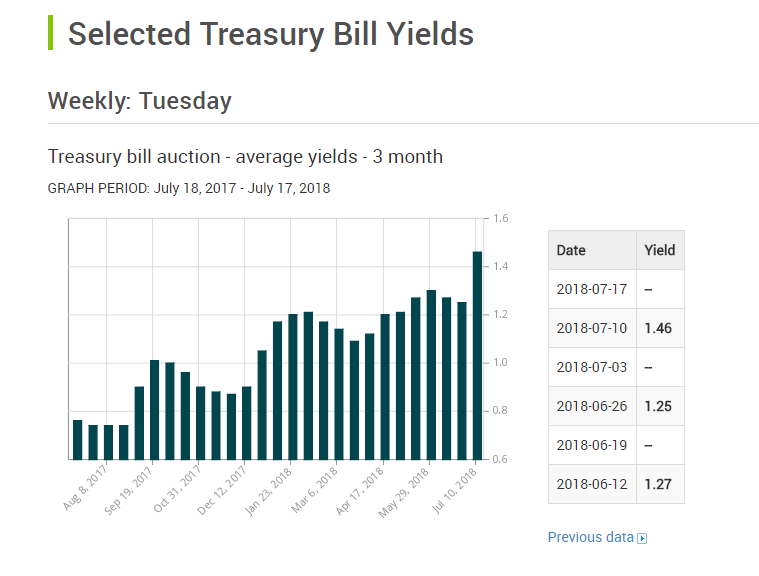

If I look at the yields, those are now a bit higher than the fee but still, the management fee of 1% and the management expense ratio of 0.56% on a money fund is outrageous! This means that the fund manager takes on average 50% of your gains!

Let’s take a look at a Fidelity fund that should have lower costs – Fidelity True North Fund!

The true north fund is charging 2.25% to its northern customers while its major selling point in the US are the low fees in the range of 0.04%. I think I missed profession, I need to become a fund manager in Canada and just live of the fat fees!

LET’s see a mixed fund like the SLF 2030 target date portfolio.

This fund that invests almost 80% of its money in fixed income, charges a fee that is 2.28% of the assets under management. With the low yield environment, the returns will probably be negative by 2030, better give you money to charity.

THESE MUTUAL PENSION FUND FEES ARE OUTRAGEOUS

If you don’t want to be a 70 year old waiter serving those rich money managers, it is time for Canadians to step up and do something, if not you will be working as a 70-year old bust boy or girl on Vancouver Island serving the fund managers and their kids that are living the rich life spending your pension!

Just an example!

THE AVERAGE EXPECTED RETURN ON STOCKS AND BONDS – a mix usually in pension funds will be 4%. If I invest $3,000 per year for 30 years the total investment is $90,000 and the final amount should be $174,000 without fees. With a 2% yearly fee deducted from my account, the final value is $123,000. This leads to a pension 30% lower than what it could be thanks to fees.

So, 30% of your pension will go to fees! 30% of your hard earned money! If we would put an average fee of 0.2% that you can get nice funds in the US for, on the same returns, it leads to a capital of $169,000.

That is just 3% of your pension. A difference of 30% on your pension is the difference between being miserable and sick and living the last quarter of your life with decency.

You, the voters in CANADA, solve this – your pension has to be 30% higher just from getting lower fees!

NOW, let’s dig into the PENSION INVESTMENT STRATEGY!

The first thing that comes to my mind is that I don’t want to pay such high fees. As those fees are fixed, whether they make money for you or not, you pay the fee, so the best way is to take just a little bit of advantage from such a situation, if we can call it an advantage.

CREATE ANOTHER PENSION FUND AND BALANCE

Here I go back to Benjamin Graham – a defensive investor, or even an aggressive investor should balance between bonds and stocks (I would say safety and growth) in relation to what are the risks of investing in stocks.

A look at the market’s PE ratio shows that stocks are historically expensive and that we can expect are extremely low returns.

Historically, at such high valuations 10-year returns have been close to zero, put a 2% yearly fee on that and you can expect your capital to be 20% smaller in 10 years.

I don’t expect much from such stocks in general – that is why I would not pay such high fees – so I would keep the cash position of my portfolio in the pension fund as I have to invest in that due to employee benefits, tax benefits etc. When stocks become cheaper again, or have a higher returns that doesn’t make the fee so outrageous, I would buy more stocks.

In the meantime, I would still make another portfolio where I would invest for the long term with better potential risk rewards, taking a bit more risk by investing in various stocks. If stocks fall, I have the money in the pension fund to buy more of those on the cheap.

So, the first pension fund strategy idea is to create your own counter balance portfolio!

If you are a bit more aggressive and still want to invest – again balance things out in the pension fund – just remember that Buffett has about 40% of his stock market portfolio in cash and he pays no fees on his stock holdings.

CREATE YOUR OWN DIVERSIFIED PENSION FUND – invest in businesses, stocks, real estate

There is no other option than to invest on the side, see what you own and how that will lead to your financial goals. It is extremely important to do so. Be hedged, because if you invest in the Canadian index you are really exposed to banks, that depend on the real estate market that consequently depends on your economy. However, you job too depends on the economy, so you are really only long the country and thus badly diversified.

As, said, think out of the box to create a better financial future for you! In this environment you have to take responsibility for your financial life and retirement because others it seems care only about fees.

Contact Justin and make him change the rules for your betterment!